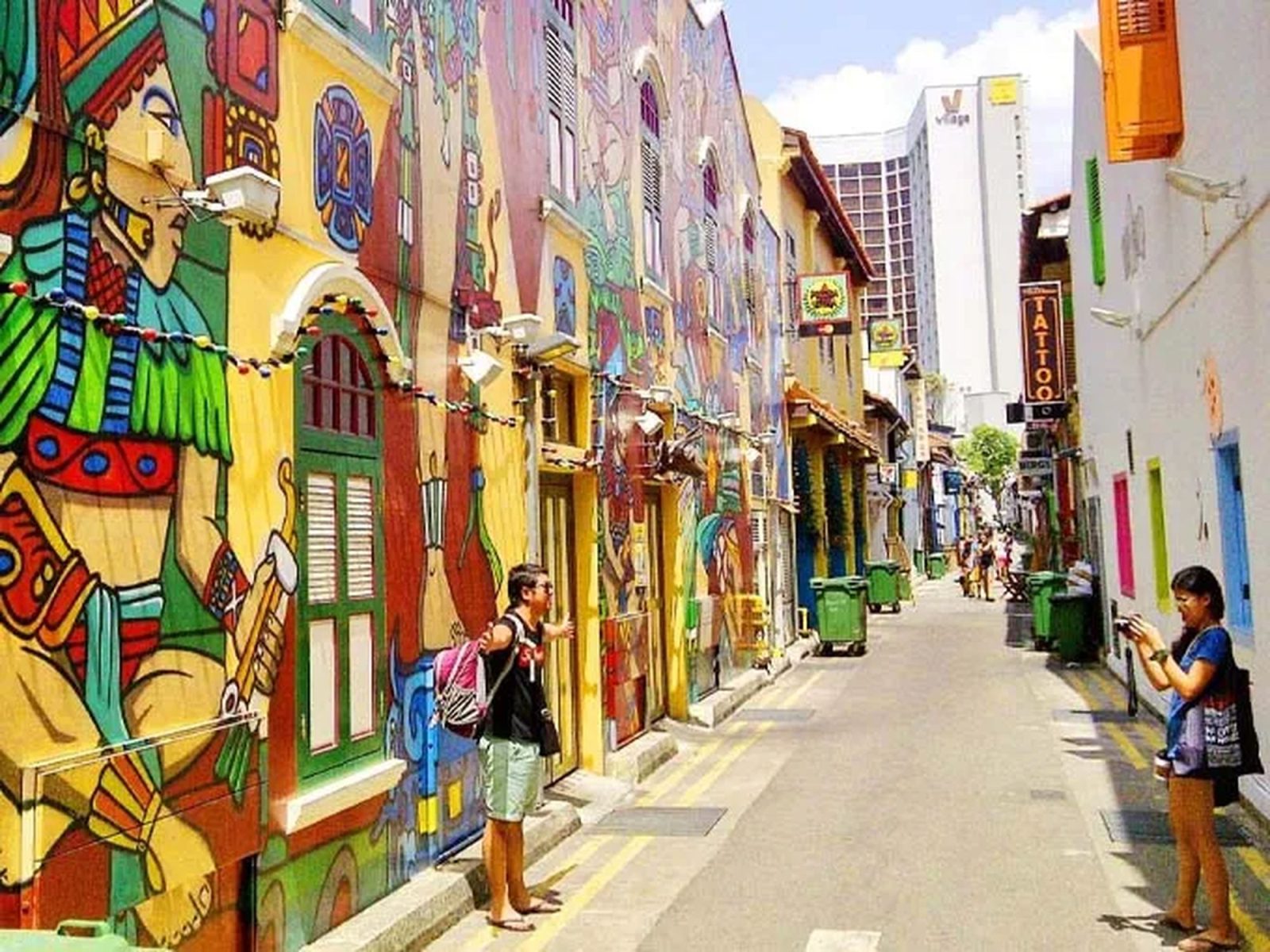

On any weekend evening, the contrast between the main historic districts in Singapore is hard to miss. Most of the crowd in Chinatown empties out by 10pm and Little India holds to its weekday rhythm. But Kampong Gelam, especially Haji Lane and Bali Lane, fill up with different crowds.

This heritage area, which stretches from Rochor Road to the Kallang River, sees a throng of crowds in the daytime that explore the various vintage, fashion, and the photo-booth concepts that have multiplied along Haji Lane.

But in the evening, the diners spill onto the street which turns into a vibrant pedestrian-only zone from 3pm to 1am on weekdays, and from 12pm to 1am on the weekends and public holidays.

The vibrancy of this popular destination has also ignited recent discourse about the retail and lifestyle experience there. Long-time tenants say that they are being priced out as rents increase, more shops seem shuttered, and the precinct’s homegrown character is giving way to tourist-targeted formats.

But do we see this reflected in the actual transaction figures and rents on these streets? What does it say about the direction that Kampong Gelam is heading, and are the recent complaints right?

News pieces like this explain what's happening in the market. Our consultations are designed to help you understand what it means for your own property decisions.

If you're considering buying, selling or upgrading, we'd be happy to help you work through your options.

Placemaking is what makes Kampong Gelam louder than its peers

Each of the conservation districts in Singapore have their own character that is bound to their histories, but their streetscapes sometimes don’t behave in the same way. And in the case of Kampong Gelam, its edge is the curation of its lifestyle, F&B, and retail offerings.

Stretches of Bali Lane and Haji Lane are pedestrianised at certain times throughout the week, which lets some F&B tenants extend their alfresco seating along the road. Kampong Gelam is also one of the precincts in the Urban Redevelopment Authority (URA)’s Business Improvement District (BID) programme.

This formally hands placemaking activity, festival calendars, and trail design to the business community there. The government supports this by providing dollar-for-dollar matching on member fees up to $500,000 a year for the first four years. The cluster’s identity, its day-and-night usage, and its event programming are curated outputs, not residual character.

This tells us a lot about the way rents there have been moving in recent years. Over time, when retail footfall is durable and broad, the tenant paying the highest rent is not the only viable tenant. Smaller operators can survive on a corner of the precinct’s traffic without having to dominate it.

Based on URA data, how each stretch of street in Kampong Gelam has performed gives us a better idea of the transformation of each area, rather than a general view of the retail situation in the precinct.

Only Haji Lane has held on to the rental spike since 2024

Examining the transaction data also suggests that the different market cycles and periods of time that recorded high, or low, rents inform us about the area’s market dynamics.

The median rent on Haji Lane was $7.29 psf in 2022 and it slipped to $6.43 psf in 2023. In 2024, it jumped to $12.39 psf, a whopping 93% increase in a single year.

But rents eased to $9.59 psf in 2025 before picking up again, and in the first five months of 2026, the median rent is about $12.94 psf based on 10 contracts that have been lodged year-to-date (YTD). The total value of each of the monthly rental transactions that have been signed so far this year amounts to more than $98,000 based on the 10 contracts signed since the start of this year.

Our examination of the rental data in 2024 suggests that the spike in rents was not confined to tenants along Haji Lane. In neighbouring Arab Street, the median rent rose from $6.24 psf in 2023 to $8.66 psf in 2024, a 39% increase. Retailers along Bali Lane saw a more modest increase, from $5.98 to $6.55 psf over the same period.

But the movement in rents from the start of 2025 to date varies by street. While average rents along all three of these streets in Kampong Gelam eased in 2025, the real divergence showed up since the start of this year.

In 2025, rents along Haji Lane dipped to $9.59 psf but rebounded significantly to $12.94 psf in the first five months of 2026, slightly above its 2024 peak. The level of rents in Arab Street held close to its peak in 2024 all through 2025, with median rents there coming in at $8.07 psf. But then this fell sharply to $6.21 psf in 2026 YTD, slightly below its 2023 level.

On the other hand, rents along Bali Lane softened to $6.06 psf in 2025 before rising to $7.08 psf in 2026 YTD, also a fresh high but still in a low band that most operators are used to in this area.

The trajectory of rents has spurred discourse online and in the media that Kampong Gelam losing its character is a reflection of the rental situation that tenants there faced since 2024 and 2025.

However, our view of the data is that, at least on Arab Street, the precinct generally seems to have priced itself back into accessible levels that most businesses would find manageable, from a rental perspective and notwithstanding the high cost of labour and goods.

If we take a step back and look at other conservation areas, the figures are similar but follow different timelines for each heritage precinct. Median rents in Pagoda Street in Chinatown nearly doubled from $4.50 to $8.91 psf in 2023, but subsequently slipped to $7.55 psf in 2024 and sit at around $8.24 psf today.

South Bridge Road, the arterial running through the same Chinatown conservation belt, has drifted higher across the full period of time we’re examining, from $5.40 psf in 2022 to $7.06 psf in 2026 YTD (+31%), without the spike year that defined the tourist-headline streets.

Buffalo Road in Little India has seen volatile years with rents falling from $13.52 to $9.88 psf in 2023, before recovering to $12.19 psf in 2024, but have dropped to $11.06 psf to date. Meanwhile, rents along Serangoon Road have fallen 31% over the nearly four-year period, from $7.06 psf in 2022 to $4.84 psf today.

Median rental $psf by year

| Street (Conservation Area) | 2022 | 2023 | 2024 | 2025 | 2026 (YTD) | 2022 vs. 2026 % difference |

| Haji Lane (Kampong Gelam) | $7.29 psf | $6.43 psf | $12.39 psf | $9.59 psf | $12.94 psf | +77.5% |

| Bali Lane (Kampong Gelam) | $4.77 psf | $5.98 psf | $6.55 psf | $6.06 psf | $7.08 psf | +48% |

| Arab Street (Kampong Gelam) | $6.13 psf | $6.24 psf | $8.66 psf | $8.07 psf | $6.21 psf | +1% |

| Buffalo Road (Little India) | $13.52 psf | $9.88 psf | $12.19 psf | $11.23 psf | $11.06 psf | -18% |

| Serangoon Road (Little India) | $7.06 psf | $7.47 psf | $7.15 psf | $5.65 psf | $4.84 psf | -31% |

| Pagoda Street (Kreta Ayer) | $4.50 psf | $8.91 psf | $7.55 psf | $7.44 psf | $8.24 psf | +83% |

| South Bridge Road (Kreta Ayer) | $5.40 psf | $6.62 psf | $6.56 psf | $7.29 psf | $7.06 psf | -31% |

There are two findings that stand out from this dataset. The Haji Lane to Arab Street rent ratio was 1.19x in 2022 and is 2.08x today. This means that within Kampong Gelam, the ability to tide through the recent rental growth largely depends on the occupiers and their own staying power.

The streets where the tenant mix could not absorb the new rent level have priced themselves back. The same shape holds across belts: South Bridge Road, the arterial in the Chinatown conservation belt, drifted steadily without ever spiking, while Pagoda Street in the same belt had its sharp 2023 run.

Overall, the rental movement seems to be concentrated on tourist-headline micro-streets and generally not along conservation streets.

Two factors plausibly explain the divergence in rents in this precinct. The first is a self-reinforcing tenant mix. Photo-booth concepts, souvenir retailers, and themed F&B can pay the higher rent because their revenue is tied directly to weekend foot-traffic of the kind Haji Lane reliably delivers.

As long as those retail formats are able to keep delivering on the asking rent, the rental ceiling that we see across the area will generally hold firm.

Next is the lingering effect of higher interest rates on individual landlords. Several of the shophouse landlords on Haji Lane bought those properties during the higher interest rate environment in 2022 and 2023. To service their mortgage, or to justify the high acquisition cost, most have turned to upward rental revisions.

The result is that landlords lean towards the bidder who can pay, not the local business or tenant mix that may be a better fit for the area.

Meanwhile, Arab Street tells a different story. The street sits one block off Haji Lane but draws its own daytime foot traffic. It has long been home to textile traders and rattan merchants, not the trendy mix Haji Lane is known for.

The spike in rents in 2024 pushed rents there to $8.66 psf and held near that level through 2025 at $8.07 psf, but did not carry into the rest of this year. The median rent has fallen to $6.21 psf in the first five months of 2026, back to what the long-standing tenants have historically operated at.

The rent ceiling on a street, the data suggests, is set as much by who walks down it as by what a tenant can pay.

According to Loyalle Chin, the broader Bugis area sits above central business district shophouse comparables on rental psf. He attributes this to URA’s Live-Work-Play implementation around the Ophir-Rochor corridor under the Master Plan 2025, leading to further intensification and rental growth in the precinct.

URA’s quarterly street-level data supports this: median asking retail rents along North Bridge Road have held above $9.30 psf through most of 2024 and 2025, ahead of comparable conservation stretches like Beach Road.

A property agent with PropNex Realty, Chin specialises in shophouses and commercial buildings and is one of the co-founders of Steward Asia, a team of agents under the property agency. He also has a portfolio of properties in this district.

On the ground, Chin says he has had tenants asking for rent rebates due to ongoing road works for the North-South Corridor (NSC), where barricades to sound-proof the construction have blocked pedestrian flow into shops fronting Bali Lane.

He also notes that retailers who rely on tourist footfall, such as souvenir shops, have been offering above-market rent for shophouse space, raising the cost ceiling for other tenants. “The profit-driven landlord will pick the higher-paying tenant, while the landlords with a longer-term vision will pick reasonably-paying tenants that will bring positive gentrification to the neighbourhood,” he says.

Shophouses with longer remaining leasehold tenures command a clear premium

Based on URA caveats lodged over the last 60 months, the median price for shophouses in the Kampong Gelam Conservation Area is about $6,026 psf (based on the land area) across 46 transactions that have been lodged during that period.

That headline figure compresses a wide spread. Along Haji Lane and Bali Lane, where there are mostly 999-year leasehold shophouses, those properties have typically traded in the range of $8,000 to $10,800 psf.

On the other hand, the 99-year leasehold shophouses along Jalan Sultan and parts of North Bridge Road have transacted closer to $2,800 to $5,000 psf. For context, the Kreta Ayer Conservation Area in Chinatown has a five-year median price of $11,627 psf, and Little India sits at $4,612 psf over the same period.

Recent transactions in Kampong Gelam indicate that most buyers have settled in this price range at the moment. A freehold shophouse at Sultan Gate fetched $19.1 million ($10,748 psf) in March 2025. A freehold unit on North Bridge Road traded at $9.9 million ($5,507 psf) in October 2025.

A leasehold shophouse on Arab Street changed hands at $5.32 million ($8,102 psf) in December 2025. The most recent Haji Lane sale lodged with URA dates to August 2022, at $3.8 million on just a 393 sq ft land plot.

According to Chin, 12 Haji Lane, an inter-terrace shophouse on a 650 sq ft land plot with a built-up area of about 1,150 sq ft, recently transacted in August 2025 for $6.98 million. A corner unit on the same stretch, he says, would fetch closer to $10 million today. The prominent corner pair at 26 and 28 Haji Lane is being held by investors who will only consider letting go at $20 million.

Corner shophouses command a premium because they can host alfresco F&B seating, one of the few uses that can match the rents on the precinct’s prime stretches.

Today’s shophouse buyer is no longer the owner-occupier or family business of years past. Chin recently closed a $22 million shophouse deal with a family-office buyer who purchased the asset for their own use, and is seeing more ultra-high-net-worth individuals (UHNWIs) and family-office capital enter the shophouse segment.

His take on their motivation to acquire these properties is straightforward: Core Central Region (CCR)-adjacent positioning at a lower entry psf than a comparable freehold residential purchase in the prime districts themselves.

Most of the return is in capital gains, not rent

He puts the upper bound for freehold and 999-year shophouse rental yields in this stretch at no more than a gross of 1.9%, with 99-year leasehold shophouses in the high 1% to 3% range.

Many leasehold buildings in Tanjong Pagar and elsewhere in the central area have approximately 60 to 70 years left on their lease, with capital values still rising in tandem with inflation. Chin opines that yields are unlikely to climb much further, given continued capital inflow into the shophouse asset class, as well as the current low interest rates.

This matters for tenants more than it does for owners. Most of the investment return on a Kampong Gelam shophouse today stems from its capital appreciation, not the rental yield. As long as transaction prices keep rising, the rent that supports the entry psf also has to rise, and the next tenant the landlord prefers is the one whose business model can pay that rent.

Recent ‘pop-up shops’ in the cluster dictate the retail experience

Some of the public discourse has framed master-tenant arrangements as a subletting workaround. This is when an operator leases space at full rent and then sublets to smaller pop-ups, including the photo-booth concepts that have multiplied along Haji Lane.

This does not technically cross any planning rule — URA regulates how premises are used, not how the tenant arranges the space. And whether the lease itself permits subletting is another contract question between the landlord and tenant.

This means that engaging an event operator to programme rotating pop-ups inside leased premises is generally an in-use activity, not a change of use.

That nuance matters because the model is, in practice, one of the few paths through which a small homegrown brand can show up on Haji Lane at all today. The headline rent on a full unit means that less than a handful of independent local brands can afford it.

This is the part of the story that is easy to miss when reading the rent figures alone. According to Chin, smaller-stall rates in these shophouse pop-ups can cost $20 psf and above, cheaper than a Bugis Street equivalent and without the opening-hour restrictions of a shopping mall.

They also gain access to Haji Lane’s trendy, up-and-coming crowd. For a young, brand-building business, that mix of price, footfall, and freedom often beats the alternatives. When the master operator picks a well-represented slate of small businesses, this adds variety and greater footfall to the precinct.

Where is the precinct heading?

Three structural shifts ahead are likely to widen the gap between rent-paying and character-anchoring tenants. The first is the broader live-work-play intensification of the Bugis precinct around Kampong Gelam.

As the area becomes more dense, through new developments like Guoco Midtown, the Shaw Towers redevelopment, and any future release of undeveloped plots in the stretch, the implied land value of nearby shophouses moves with it.

The second is URA’s car-lite ambition for Kampong Gelam, set out in the 2023–2028 Place Plan, which includes road dieting on Arab Street to widen walkway space and broader pedestrian-connection improvements across the precinct.

The third is the completion of the North-South Corridor (NSC) in 2029, which will remove the current street-front blockage along Bali Lane towards Ophir Road and bolster connectivity.

Each of those, on its own, will result in supporting the growth of rents in the area. Plans for Arab Street are the cleanest near-term test of the rental trajectory. Shophouse rents in Arab Street traded at $8.66 psf in 2024 and gave nearly all of that back by the end of this quarter.

The question is whether wider walkways and more foot traffic can re-energise the rent and let it stick this time, or whether the street’s heritage tenant mix continues to anchor it at the $6 psf level.

A reflection of emerging retail trends

Haji Lane has always mirrored Singapore’s retail landscape. The nightlife-heavy late-evening years gave way to a daytime trade in vintage and fashion, with F&B still anchoring the evening but quieter than a decade ago. There is more to do across the day than there was five years ago, and the footfall reflects it.

The harder question is who gets to be there to take the upside, and on which streets we are asking it. The maths on Haji Lane leans towards the operator who can pay, not one who necessarily fits, as rents increase to support the price.

What keeps the cluster from collapsing into a single type of tenant is likely only the curation: the BID’s placemaking work, the master-tenant pop-up model that lets small brands rotate in, and the streets next to Haji Lane that still lease at rents that businesses can afford.

Whether Haji Lane sustains its $12+ psf median or falls back the way Buffalo Road did remains to be seen, but the precinct still has the structural pieces to keep room for the heritage businesses that built its character.

A single headline is rarely enough to change your plans. The value comes from understanding how today’s news fits into the broader direction of the market.

If you’d like to talk through what a shift like this means for your own timing, purchase, or exit, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

0 Comments