If it feels like more Singaporeans are packing up and building lives overseas, that’s because they are.

According to a report by the Department of Statistics in September 2025, the number of Singaporeans residing overseas has grown from about 213,00 in 2016 to over 221,000 by the end of last year.

There are now more Singaporeans living overseas compared to before the Covid-19 pandemic in 2019. In the report, the overseas Singaporean diaspora refers to citizens who have resided abroad for at least 20 years.

For many Singaporeans abroad, living overseas comes with a financial dilemma that’s easy to overlook: a tough choice between deciding whether to invest in a property overseas, or keep the cash in order to purchase a home in Singapore when they return for good.

From my conversations with other Singaporeans living overseas, the reality is that most of us can only save up enough cash and income to cover one mortgage. That means buying a home overseas often sacrifices the option of buying in Singapore—and vice versa.

So far, the most practical piece of advice I’ve come across is surprisingly simple: own property in the market that gives you the greatest leverage as a homeowner.

The challenge for many buyers today isn't access to information.

It's interpreting that information in a way that makes sense for their finances, goals, and stage of life.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

The Cost Of Waiting: Singapore’s Housing Market Is Evolving While You’re Away

There’s a perception that overseas Singaporeans are all living it large as well paid expatriates, and have a much greater chance returning as wealthy buyers and investors to pick up their choice of luxury condominiums or million-dollar HDB flats.

Frankly, this is far-fetched and rarely the case of the majority of Singaporeans working and living overseas. This is because Singapore’s property markets have recorded some of the largest price increases among most of the global gateway cities and developed economies.

For those of you that haven’t been paying much attention to the housing market in Singapore, HDB prices have been rising rapidly over the past few years. Islandwide resale prices jumped 9.5% in 2024 and resale prices still grew about 4% in 2025. Only recently did the market started showing signs of moderation.

While the spike in resale prices wasn’t as large in 2025, the HDB Resale Price Index has shown compounding gains across the last five years, and analysts from ERA and PropNex are projecting a further rise of 4 – 5% in 2026.

At the same time, the proportion of million-dollar flats, as a percentage of the total sales volume, has been gradually increasing. Last year, a record number of million-dollar HDB transactions were recorded, with 1,544 resale flats sold for over $1 million.

As more HDB estates record million-dollar resale transactions, it suggests that a new price ceiling is emerging, especially among estates in the central region.

What does this mean for Singaporeans living abroad who plan to return in the next five years? I think that some of you will find that the home which you had planned to purchase is now just out of your reach, and fetches a much higher price than what it is going for today.

My perspective is that staying liquid (or at least cash-rich) until your return might not be the most prudent choice at the moment.

The Homeownership Trap: Why A Sound Exit Strategy Is A Crucial Consideration

The way I look at it, the most logical thing to do might be to purchase a place of your own to stay in while you’re abroad, especially if you don’t plan to buy a property in Singapore. But depending where you are in the world, housing markets which have high barriers to entry, modest property yields, and slower market liquidity might turn you away from this option.

In Singapore, the residential market is one of the most liquid housing markets in the world due to its relatively large pool of well-financed buyers. On the other hand, most overseas housing markets are characterised for their relatively more volatile markets and a proportionately smaller catchment of so-called ‘safe’ buyers.

If your personal situation changes – let’s say, your employment situation, a family event, or a shift in government policies – exiting an overseas property can take much longer and cost quite a bit.

For example, in high cost-of-living cities like Melbourne or London, foreign buyer surcharges in both Australia and the UK are steep enough that unless you’re staying for the long haul, you’ll likely spend your first few years just breaking even on transaction costs. In these markets, liquidity and long-term property appreciation are meaningful, but there is a steep toll to pay for entry.

Meanwhile, in most European housing markets, like Sweden and Netherlands, it takes a long time to find a suitable buyer which can stretch out the amount of time that you’re holding on to that property.

Sweden is still working through a post-2022 hangover in its housing market which is characterised by high unsold inventory, while government regulation in the Netherlands seems geared towards pushing out foreign investors through strict rental regulation.

Overall, most European housing markets may look attractive on the surface with relatively high yields… until you remember the fact that you’re converting back to SGD a decade later and taking in the currency risk as well as forking out on taxes on your capital gains.

Even markets closer to home in Southeast Asia aren’t automatically good investment opportunities. Johor may seem like an obvious choice, but the resale market for foreign-priced condominiums is very thin. Batam is leasehold-only with a still-maturing resale market, Bangkok has foreign ownership quotas per building that can complicate your eventual exit, and Bali is more of a lifestyle bet than a proven investment market.

Wherever you are in the world, divesting a property is just as challenging, if not more challenging, compared to buying into the market. That’s the part most people forget to account for when they embark on a buying spree overseas.

Setting Yourself Up For Success: The Case Of Buying Overseas

To be clear, I’m not writing all of this to scare you off overseas property ownership, quite the contrary. But it’s worth recognising that overseas property markets don’t offer the same level of regulation and buyer protections that Singapore has. Many of the safeguards Singaporeans take for granted simply aren’t standard elsewhere.

Let’s address the prevailing misconception: buying overseas property automatically increases your net worth. It doesn’t, all you’re really doing is converting a liquid asset into an illiquid one.

Therefore it’s important to look at your overall finances and make decisions based on a sound analysis of price trends and property benchmarks, instead of relying on your gut.

For retirees, I reckon that a good rule of thumb would be to limit your overseas property to no more than 30% to 40% of your total net worth. Meanwhile, working professionals should be able to comfortably service the mortgage of an overseas property entirely on a median local income. This protects you from market shocks and unexpected events like being let go, while opening up the property to a more accessible buyer pool when you need to sell it.

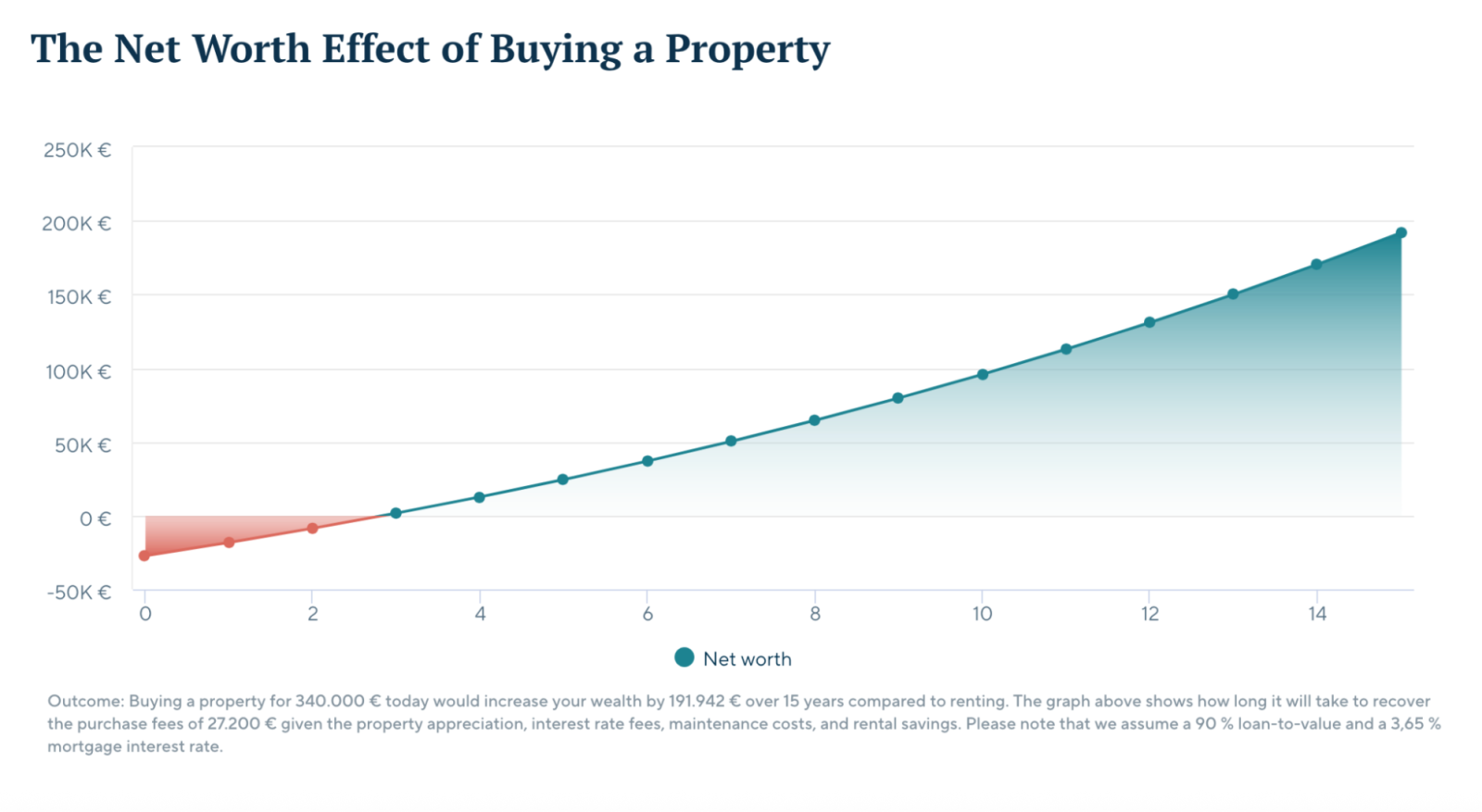

Next should be an examination of your cashflow. Does buying the property free up more cash, or does it make you less liquid on a month-on-month basis? Most aspiring buyers just compare mortgage payments with their current monthly rent and just stop there.

However, there are plenty of hidden costs that come with owning property. So the real number to calculate is the full costs (mortgage, property tax, maintenance fees, insurance) against a realistic rental projection that includes upward revisions.

Compare these considerations with your mortgage timeline before you decide. Buying overseas should ideally free up cashflow and put you on the path towards greater financial flexibility. There are plenty of rent vs. buy calculators online that you can tap on to do this comparison, but it’s also worth your while to crunch the numbers on a spreadsheet.

Finally, you should be buying property in areas that see a healthy volume of resale activity. This means owning property in populated towns and cities where the housing market regularly records a healthy turnover.

This is important not only from a profitability standpoint, but it also protects the value of the property you own and where your monthly mortgage payments go towards. In general, where there is demand, there is value.

If all three of these conditions are met, I believe that buying an own-stay property can genuinely build on your financial security while you’re abroad. You’re paying to live somewhere anyway, paying yourself instead of someone else usually makes more sense.

But if even one of the three conditions is shaky, I reckon that renting and keeping your capital flexible is usually the smarter call.

Conclusion

Overseas Singaporeans tend to enjoy a much wider range of options when it comes to property ownership and investment, compared to most locals that have to navigate our home market. But more options also means more ways to get it wrong.

Accumulating cash in order to finance a future property purchase in Singapore is a legitimate strategy, but so is putting your money to work where you’re abroad.

What isn’t a strategy is drifting through a ten-year posting without ever running the numbers, and then returning to a local housing market that’s moved further than you expected in terms of property prices.

Wherever you land on this, my opinion is that the worst decision is the one where you never decided at all – because not deciding is still a decision, and it’s usually the most expensive one.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

0 Comments