The HDB Resale Price Index (RPI) fell 0.1% q-o-q in 1Q2026, the first quarterly decline since 2Q2019, nearly seven years ago. This follows a flat reading in 4Q2025 of 0.0% in 4Q2025, and it is the end of a consecutive streak of quarterly price growth in the public housing market since the end of the Covid-19 pandemic.

The latest pricing statistics, released by HDB on April 24, suggests the HDB resale market is settling into a more measured pace after a prolonged period of market activity that drove up overall prices.

But a closer look at the latest figures suggests that the market is moving in very different directions depending on which estate, which flat type, and which price segment you are looking at.

News pieces like this explain what's happening in the market. Our consultations are designed to help you understand what it means for your own property decisions.

If you're considering buying, selling or upgrading, we'd be happy to help you work through your options.

Not a uniform decline in prices

The 0.1% dip is an aggregate of mixed outcomes across flat types. Based on resale transaction data compiled by Realion Group, average prices fell for one-room flats (-4.4% q-o-q), executive flats (-2.9%), and five-room flats (-0.7%). On the other hand, the average price of two-room flats grew 1.5% q-o-q, three-room flats recorded a price uptick of 1.0% q-o-q, and the price of four-room flats increased 0.8% q-o-q.

At the median level, Nicholas Mak, chief research officer of Mogul, states that four-room and executive flat prices fell 0.3% and 1.6%, respectively; meanwhile, two-room and five-room flat median prices rose 0.5% and 0.7%, respectively. The two datasets point in the same direction: the declines were most pronounced at the extremes of the size range, while the three-room and four-room segments, which collectively account for roughly two-thirds of all resale transactions in 1Q2026, stayed in positive territory.

Christine Sun, chief researcher and strategist at Realion Group, attributed the overall index dip to two concurrent trends. The price decline can be attributed to the slower buying sentiment, as more resale flats reached their MOP and were listed for resale, she says.

Resale volume up from last quarter but below transaction volume a year ago

A total of 6,285 resale applications were registered in 1Q2026, an increase of 19.6% from the 5,256 resale transactions lodged in 4Q2025. The rebound is consistent with a recurring seasonal pattern: sales volumes have moderated in every fourth quarter of the past several years before recovering at the start of the following year, as buyers tend to defer purchase decisions over the year-end festive period and the start of the school holidays, returning to the market in the new year.

However, on a yearly basis, the 6,285 sale applications in 1Q2026 were 4.6% below the 6,590 sales recorded in the same quarter a year earlier, and 13.0% below the 7,221 applications in 3Q2025, which emerged to be the strongest quarterly sales in 2025.

The breakdown of flat types from official HDB data shows four-room flats dominated resale activity, with 2,777 applications or 44.2% of the total resale volume. Three-room flats contributed 1,504 sales (23.9%), there were 1,431 five-room flats sold (22.8%), and 378 executive flats (6.0%) changed hands.

Comparing the HDB resale performance of 1Q2026 against 1Q2025, the three-room segment recorded the sharpest y-o-y decline, with transactions falling from 1,687 to 1,504, a drop of 10.8%. Executive flat volumes held almost flat at 378 in 1Q2026, compared to 375 in 1Q 2025, reflecting the limited supply of this flat type in the secondary market following its discontinuation in new HDB launches since 1995.

Number of Resale Applications by Flat Type

| QUARTER | 1-ROOM | 2-ROOM | 3-ROOM | 4-ROOM | 5-ROOM | EXECUTIVE* | TOTAL |

| 1Q2025 | 1 | 220 | 1,687 | 2,825 | 1,482 | 375 | 6,590 |

| 2Q2025 | 2 | 256 | 1,760 | 3,033 | 1,614 | 437 | 7,102 |

| 3Q2025 | 1 | 224 | 1,713 | 3,176 | 1,657 | 450 | 7,221 |

| 4Q2025 | 1 | 171 | 1,328 | 2,266 | 1,213 | 277 | 5,256 |

| 1Q2026 | 3 | 192 | 1,504 | 2,777 | 1,431 | 378 | 6,285 |

That said, the resale market remains the fallback option for buyers who cannot wait for BTO projects, says Eugene Lim, key executive officer of ERA Singapore. The February 2026 BTO sales exercise attracted around 15,000 applications, a subdued response compared to the 33,000 seen in October 2025, despite a concurrent Sale of Balance Flats (SBF) exercise alongside the BTO launches.

“The resale market continues to act as a crucial outlet for unmet housing demand, especially for buyers who value immediacy or are not keen on the locations announced for the upcoming BTO exercises,” says Lim.

Sun added that deals are taking longer to close as buyers gain more leverage given competitive market conditions. “We observed that deals are taking longer to close in recent months, as buyers had more housing options and sentiment has slowed in view of the uncertain macroeconomic conditions,” says Sun.

Median prices by town

The numbers from HDB’s 1Q2026 median resale price data by town and flat type revealed a sharp geographic divergence in the market.

For four-room flats, Queenstown recorded the highest median price at $1.04 million, followed by Toa Payoh at $1 million. Bukit Merah came in at $938,000 and Kallang/Whampoa at $929,000. At the other end, Jurong West ($535,500), Woodlands ($550,000), and Choa Chu Kang ($550,900) recorded the median price of four-room flats below $560,000, roughly half the quantum reflected in Queenstown.

The median price in Toa Payoh is worth examining directly. A median price of $1 million for four-room flats in that town indicates that approximately half of all four-room resale transactions in Toa Payoh during the first quarter of this year surpassed the million-dollar mark, reflecting a price premium that is no longer driven by a handful of standout units. It is now what a typical buyer pays in that estate for a 4-room flat. The same is true in Queenstown, where the median price of a four-room flat is $1.04 million, which likewise places the majority of transactions of these units in that town above $1 million.

In the five-room segment, the price gap is even wider. Toa Payoh’s five-room median stood at $1.1 million, Ang Mo Kio at $1.09 million, and Bukit Merah at $1.09 million. In the suburban areas, Jurong West ($635,000), Sembawang ($652,500), and Choa Chu Kang ($675,000) were well below $700,000 for the same flat type.

For buyers whose estate preference is flexible, the price gap between central and non-central locations is the clearest opportunity in the current market.

Median Resale Prices by Town and Flat Type in 1Q 2026

| TOWN/ESTATE | 1-ROOM | 2-ROOM | 3-ROOM | 4-ROOM | 5-ROOM | EXECUTIVE |

| ANG MO KIO | – | * | $441,800 | $630,000 | $1,090,000 | * |

| BEDOK | – | * | $425,500 | $588,000 | $809,000 | * |

| BISHAN | – | – | * | $805,000 | $970,000 | * |

| BUKIT BATOK | – | $382,000 | $410,000 | $649,000 | $830,000 | $884,400 |

| BUKIT MERAH | * | * | $445,400 | $938,000 | $1,085,000 | – |

| BUKIT PANJANG | – | * | $465,000 | $566,500 | $706,400 | * |

| BUKIT TIMAH | – | – | * | * | * | * |

| CENTRAL AREA | – | – | * | * | * | – |

| CHOA CHU KANG | – | * | $462,500 | $550,900 | $675,000 | $822,900 |

| CLEMENTI | – | * | $435,000 | $781,000 | * | * |

| GEYLANG | – | * | $388,000 | $808,400 | * | * |

| HOUGANG | – | * | $450,000 | $617,000 | $778,500 | $920,000 |

| JURONG EAST | – | * | $415,000 | $548,900 | $715,500 | * |

| JURONG WEST | – | * | $386,500 | $535,500 | $635,000 | $800,000 |

| KALLANG/WHAMPOA | – | * | $450,000 | $929,000 | $930,500 | * |

| MARINE PARADE | – | – | * | * | * | – |

| PASIR RIS | – | * | * | $640,000 | $735,000 | $927,500 |

| PUNGGOL | – | $395,400 | $545,000 | $685,000 | $805,000 | * |

| QUEENSTOWN | – | * | $500,000 | $1,038,000 | * | * |

| SEMBAWANG | – | $371,000 | $522,500 | $600,000 | $652,500 | * |

| SENGKANG | – | * | $540,000 | $640,000 | $710,000 | $854,000 |

| SERANGOON | – | – | $468,000 | $650,000 | * | * |

| TAMPINES | – | * | $491,400 | $668,000 | $820,000 | $970,000 |

| TOA PAYOH | – | * | $370,000 | $1,000,000 | $1,100,000 | * |

| WOODLANDS | – | * | $432,500 | $550,000 | $650,000 | $935,900 |

| YISHUN – | * | $435,000 | $555,000 | $700,000 | $880,000 |

Asterisks (” * “) refer to cases where there are less than 20 resale transactions in the quarter for the particular town and flat type. The median prices of these cases are not shown as they may not be representative.

Million-dollar flat transactions hit a new high

The consistent increase in the proportion of million-dollar flat transactions sits in sharp contrast to the overall decline in resale prices. A total of 412 resale flats changed hands at $1 million or above in 1Q2026, up 17.7% from 350 in 4Q2025. Based on data compiled by Mogul, the count also rose 23.4% compared to the figure in 1Q2025.

Overall, million-dollar flats represented 6.6% of all 1Q2026 resale transactions, below the 6.7% share recorded in 4Q2025 but well above the 5.1% recorded in 1Q2025 and more than five times the 1.2% proportion seen just four years ago in 1Q2022.

By flat type, four-room flats led with 190 million-dollar transactions, followed by five-room flats (143), executive flats (78), and one multi-generation flat.

The geographic concentration was consistent with the median price data. Toa Payoh recorded the most million-dollar deals at 72, followed by Bukit Merah (57), Queenstown (55), Ang Mo Kio (41), and Kallang/Whampoa (32).

These are the same estates where median four-room and five-room prices are already at or above $929,000, which means million-dollar transactions in these towns are not exceptional outliers but reflect the upper portion of a pricing distribution that has shifted upward.

About 15.3% of the 412 deals involved units fresh out of their Minimum Occupation Period (MOP) with remaining leases of 94 years or more. Alkaff Courtview accounted for 24 such transactions and Ang Mo Kio Court for 20, both illustrating how newer leases in accessible estates can support premium pricing after the lifting of resale restrictions.

“While a broader correction in HDB prices might be underway, growth could persist in specific segments of the resale market, such as million-dollar HDB flats,” says Lim.

With average mass-market three-bedroom condo prices holding above $2 million, Mak believes that large and centrally located HDB flats priced around $1 million continue to attract buyers who see its comparative value.

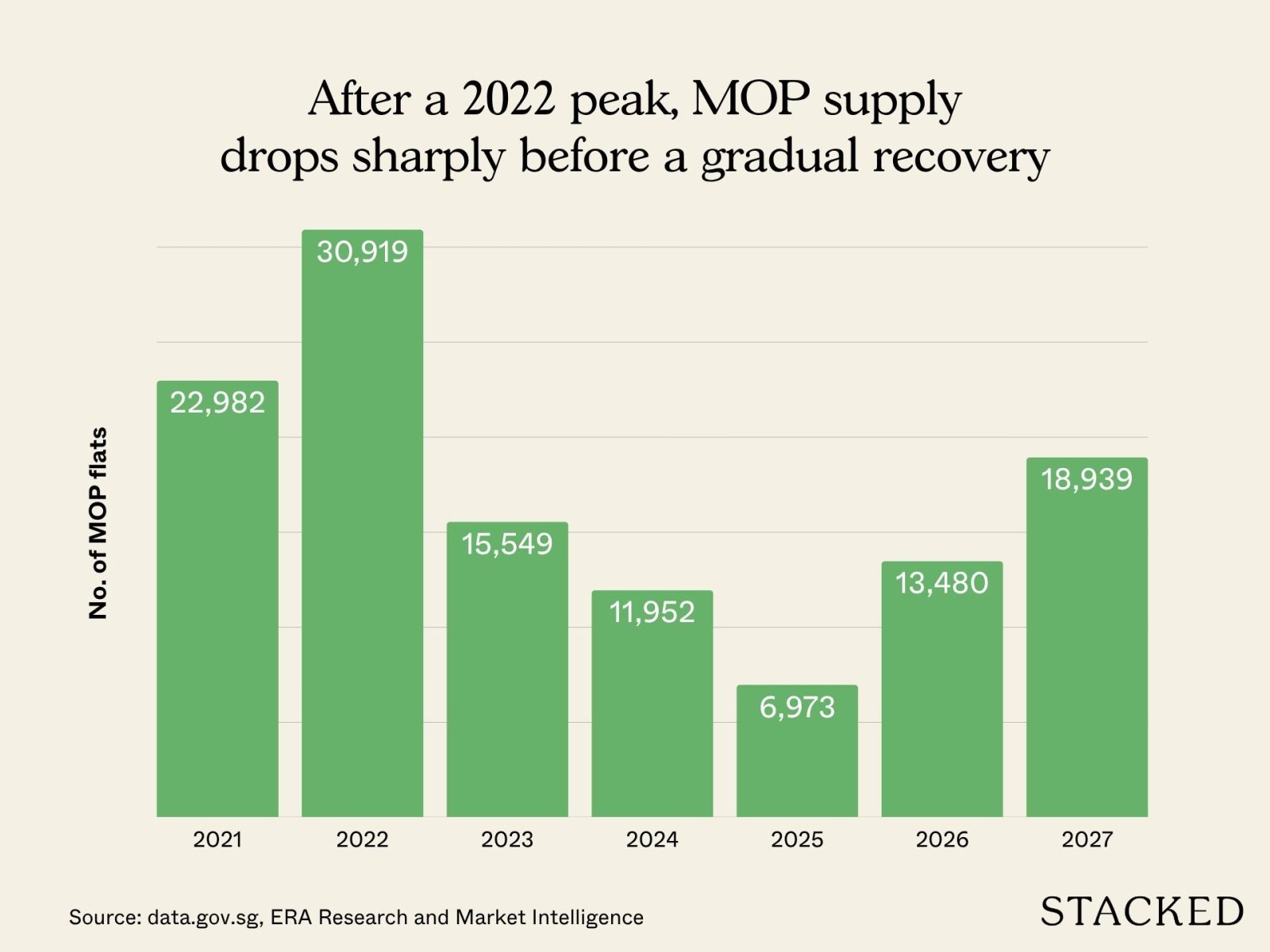

Near-doubling of MOP completions will reshape supply

A consequential structural shift in the resale market this year is the sharp increase in flats reaching their MOP. An estimated 13,480 HDB flats are expected to complete their five-year MOP in 2026, almost double the 6,973 in 2025, substantially increasing the pool of units available for resale.

Five towns account for about 80% of all 2026 MOP completions. Punggol leads with 3,222 units (23.9%), followed by Queenstown with 2,405 (17.8%), Tampines with 2,133 (15.8%), Toa Payoh with 1,594 (11.8%), and Bedok with 1,440 (10.7%).

Distribution of MOP Flats by Town in 2026

| Punggol | 3,222 | 23.9% |

| Queenstown | 2,405 | 17.8% |

| Tampines | 2,133 | 15.8% |

| Toa Payoh | 1,594 | 11.8% |

| Bedok | 1,440 | 10.7% |

| Yishun | 456 | 3.4% |

| Bukit Panjang | 350 | 2.6% |

| Sengkang | 330 | 2.4% |

| Geylang | 319 | 2.4% |

| Sembawang | 310 | 2.3% |

| Hougang | 285 | 2.1% |

| Kallang / Whampoa | 243 | 1.8% |

| Bukit Batok | 221 | 1.6% |

| Woodlands | 172 | 1.3% |

| Total 13,480 | 100.0% |

[Source: data.gov.sg, ERA Research and Market Intelligence]

A larger MOP cohort broadens buyer choice and eases upward price pressure. Sellers of MOP-ed units in premium estates will be keen to realise substantial capital gains, a portion of which is likely to flow back into the resale market or into private residential purchases.

The MOP pipeline is linked directly to the moderation in the overall RPI. With more flats entering the resale pool, buyers have a wider range of options and less pressure to act quickly. “Demand fundamentals remain intact, supported by household formation and genuine housing needs, but the urgency that previously drove sharper price increases is gradually easing,” says Mohan Sandrasegeran, head of research and data analytics at SRI.

HDB rentals

HDB approved a total of 9,535 rental applications in 1Q2026, down 0.2% q-o-q from 9,557 in 4Q2025 and a decrease of 1.3% y-o-y against the 9,662 rentals in 1Q2025. The modest movement suggests the rental market has settled into a relatively stable range.

Location continues to drive a wide divergence in rental pricing. For four-room flats, Queenstown commanded the highest median rent at $4,150 per month, followed by Bukit Merah ($3,900). Woodlands ($3,100), Choa Chu Kang ($3,100), and Punggol ($3,200) were at the lower end for four-room rentals. For three-room flats, the spread ran from $2,500 per month in Woodlands to $3,000 in Queenstown, Clementi, Kallang/Whampoa, and Bishan.

As more MOP flats enter the pool, rental competition is expected to intensify, particularly in the suburban estates where the majority of completions tend to be more concentrated. As rental supply rises, tenants will also start to gain leverage. “Since tenants will have a wider range of housing options, they will have greater negotiating leverage and stronger bargaining power to secure better rental rates and leasing terms,” says Sun.

Realion also highlighted that newer MOP flats in well-connected suburban estates may begin to attract younger expatriates who previously defaulted to condominiums, squeezing private rental demand at the lower end of that market.

HDB market outlook

Most market analysts forecast that the full-year 2026 HDB resale price growth could range from 0.5% to 5%, with most research predictions clustering in the 2–4% band. ERA is at the more optimistic end, projecting 2–5% on the back of a strong price base and MOP-driven transaction activity. The more conservative projections reflect how much weight analysts are placing on incoming supply from both the MOP wave and the BTO pipeline.

The broader HDB resale market looks more likely to track the lower end of those forecasts. The near-doubling of MOP completions, combined with 19,600 BTO flats planned across three exercises this year (including a June exercise with sought-after sites in Bishan and Berlayar), will keep supply elevated and give buyers more room to negotiate. The sustained growth in million-dollar transactions is real, but concentrated in a handful of mature estates rather than spread across the market.

Whether the 1Q2026 dip proves to be a single quarter softening or the start of a more sustained moderation in the public housing market will depend on how quickly the sizable supply of newly MOP flats is absorbed and how much of the BTO pipeline pulls first-time buyers out of the resale pool.

A single headline is rarely enough to change your plans. The value comes from understanding how today’s news fits into the broader direction of the market.

If you’d like to talk through what a shift like this means for your own timing, purchase, or exit, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

2 Comments

why do u think good estates falling but some estates like simei just set new 1mil records for 5-room in apr26? what should we consider for the future?

Hi Janet,

Great observation. The index dip is an aggregate, so it really does mask what’s happening at the individual unit level.

Estates like Simei hitting new 5-room records while “good” estates soften slightly isn’t necessarily contradictory. It’s more about where prices already were vs. where demand is still catching up. A lot of the records in established estates were set years ago and are now consolidating, while emerging estates are still in price discovery mode. Another point to consider is that nearly 13,500 flats clearing MOP this year means more supply and more competition among sellers, and that pressure isn’t evenly distributed across the estates.

There’s genuinely a lot to unpack depending on your specific situation. If you’d like us to do a proper deep-dive on your circumstances, feel free to write in to stories@stackedhomes.com and we can work through the numbers with you!