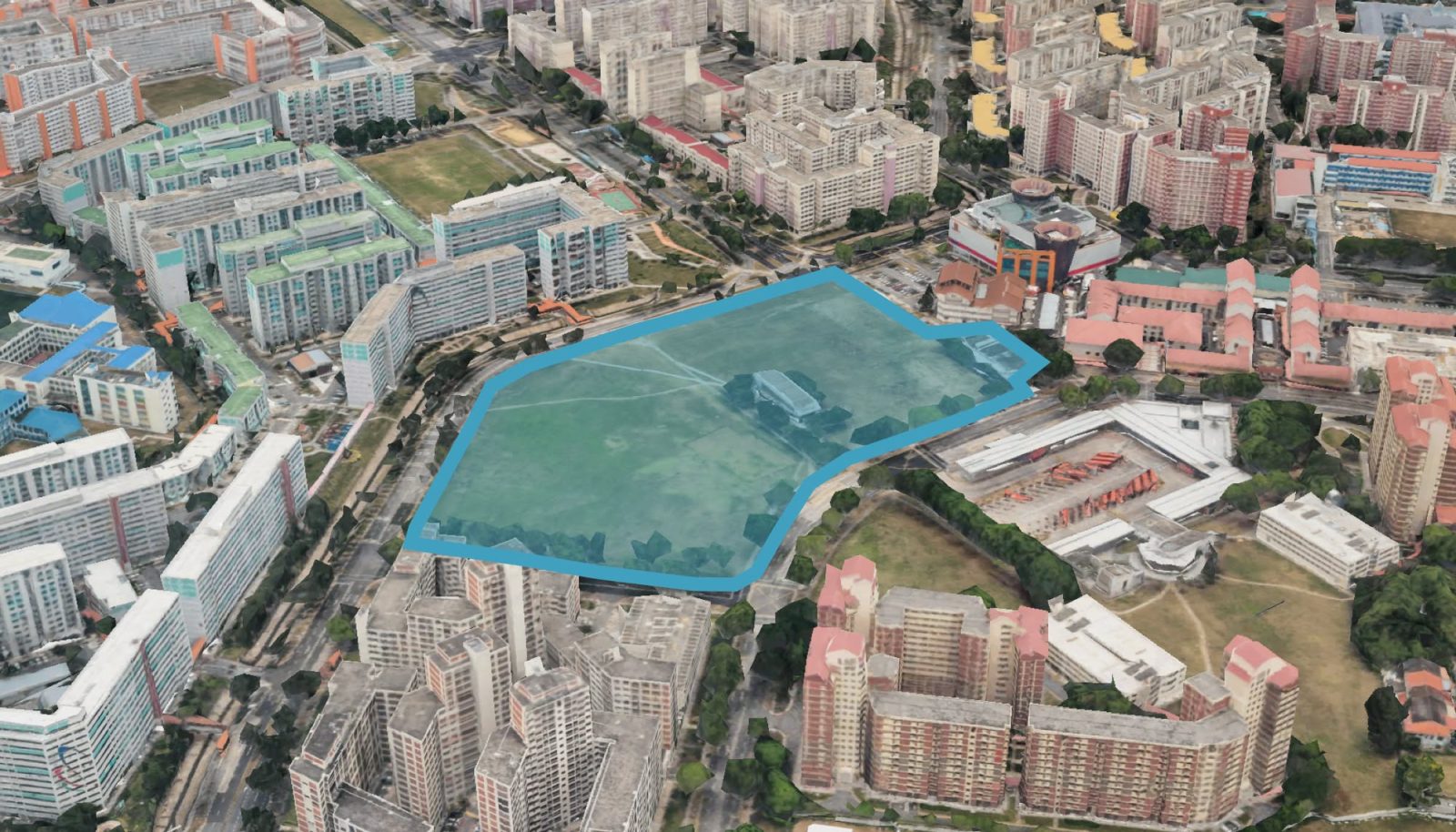

When CapitaLand and UOL Group were awarded the Hougang Central government land sale (GLS) site in January this year, the developers also secured the last undeveloped plot for a new integrated development above an MRT station on the North East Line (NEL).

The site, bounded by Hougang Avenue 10 and Hougang Central, was awarded to the consortium of developers after they put in the top bid of $1.5 billion for the 504,820 sq ft site. This works out to a land rate of $1,179 psf per plot ratio (ppr).

CapitaLand and UOL have shared that the new integrated development will comprise 830 residential units, and with approximately 300,000 sq ft of net lettable area for retail and lifestyle concepts, the development will house the largest mall in Hougang.

Under the joint development structure, the residential component will be developed by CapitaLand Development and UOL Group in a 50:50 joint venture, while CapitaLand Integrated Commercial Trust will develop and own the entire commercial component.

This is the first GLS site in Hougang since 2019, and there was strong participation among established developers.

Three bids were received when the tender closed in December 2025. Sim Lian Group came in second with its $1.47 billion ($1,155 psf ppr) bid, followed by a Frasers Property-led consortium that included Sekisui House and Lum Chang who put in a joint bid of $1.4 billion ($1,100 psf ppr).

CapitaLand and UOL’s winning bid was 2.1% above Sim Lian’s offer, a tight spread that market analysts say suggested broad agreement among developers on the site’s value.

Based on the $1,179 psf ppr land cost, most market estimates place the future launch price for the residential component above $2,500 psf. For context, that would represent a 43% – 60% premium over the current median psf of the two largest existing condo projects in the immediate area, Riverfront Residences and The Florence Residences.

Market commentary like this is only useful if you can translate it into what it means for your own purchase: your entry price, holding period and exit options.

That's where many buyers get stuck. General market insights rarely tell you whether a specific unit, at a specific price, is the right decision for your circumstances.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

The launch of Sengkang Grand Residences and its impact on surrounding resale prices.

This is not the first time that a landmark project in this area will spur an uplift in resale private residential prices. When Sengkang Grand Residences launched for sale in 2019, the integrated development commanded an average selling price of $1,747 psf.

At the time, the development was introduced into a neighbourhood where existing nearby projects were trading at considerably lower resale prices.

For example, The Quartz, a 625-unit leasehold development along Compassvale Bow, recorded an average resale price of $987 psf at the time. That condo was completed in 2009.

Likewise, Esparina Residences, an executive condominium (EC) also along Compassvale Bow, was privatised in 2020 and resale units were going for around $1,106 psf. Jewel @ Buangkok, a 616-unit development next to Esparina, saw most of its resale units change hands at an average of $1,302 psf. That condo was completed in 2016.

Based on resale data compiled by Stacked, prices at Sengkang Grand appreciated at an annualised rate of 2.37% over the six years from 2019 to 2025. Resale price growth at the surrounding projects did considerably better.

Average $PSF: Sengkang Grand Residences And Nearby Condos

| Year | SENGKANG GRAND RESIDENCES | YoY | ESPARINA RESIDENCES | YoY | JEWEL @ BUANGKOK | YoY | THE QUARTZ | YoY |

| 2019 | $1,747 | $1,106 | $1,302 | $987 | ||||

| 2020 | $1,732 | -0.86% | $1,099 | -0.56% | $1,314 | 0.98% | $1,003 | 1.71% |

| 2021 | $1,719 | -0.73% | $1,165 | 5.98% | $1,347 | 2.53% | $1,060 | 5.60% |

| 2022 | $1,812 | 5.40% | $1,304 | 11.91% | $1,447 | 7.40% | $1,245 | 17.45% |

| 2023 | $2,001 | 10.44% | $1,502 | 15.20% | $1,625 | 12.31% | $1,303 | 4.70% |

| 2024 | $2,028 | 1.31% | $1,626 | 8.21% | $1,672 | 2.87% | $1,375 | 5.55% |

| 2025 | $2,011 | -0.82% | $1,673 | 2.90% | $1,745 | 4.37% | $1,515 | 10.16% |

| Annualised | 2.37% | 7.14% | 5.01% | 7.41% |

Early Sengkang Grand figures include developer new sales, which may be affected by unit type mix at different launch phases.

Based on data compiled by Stacked, the annualised figures — 7.41% for The Quartz, 7.14% for Esparina — reflect a lower entry price point that compounded over six years. But the year-on-year breakdown is more illustrative about where those capital gains actually came from.

Across all three surrounding projects, the sharpest single-year moves clustered in 2022 and 2023, the period leading into and through Sengkang Grand Residences’ Temporary Occupation Permit (TOP).

The Quartz recorded its largest annual price increase in 2022 at 17.45%, before Sengkang Grand was completed. Esparina posted a price increase of 15.20% in 2023, and Jewel @ Buangkok 12.31% the same year.

By 2024 and 2025, resale price appreciation across all three developments had largely tapered. This means the repricing effect was front-loaded, concentrated during the construction and completion of Sengkang Grand, not in the years after the integrated development settled into the neighbourhood.

Overall, the transaction data suggests that Sengkang Grand Residences entered the market at a significant price premium. Thus, it had far less room for its resale units to notch significant price appreciation in percentage terms.

With resale units there going for an average of $2,011 psf in 2025, it remains well above its neighbours, but the 2.37% annualised growth rate reflects its higher entry price point.

The surrounding projects took most of their capital gains during the first two years of the launch of Sengkang Grand, rather than an evenly spread price growth across its entire six-year sales period.

Buyers who bought units at Jewel @ Buangkok, Esparina, or The Quartz in 2020 or 2021 caught that price appreciation window at its fullest, and by the time Sengkang Grand was completed, the sharpest price growth had already been realised.

Why Hougang was the NEL’s missing piece

To fully capture what the price trajectory at Sengkang Grand means for the upcoming integrated development at Hougang Central, we think that it would be instructive to examine the retail landscape along the North East Line.

Over the past decade, the suburban corridor along the NEL has taken shape in the form of a reasonably complete spine of integrated commercial nodes.

Potong Pasir has The Poiz Centre, and Woodleigh has Woodleigh Mall — directly connected to the station as part of an integrated development. Serangoon has Nex, one of the largest suburban malls in Singapore — also directly connected to the station and bus interchange.

Buangkok has Sengkang Grand Mall, which opened in 2023 as the retail component of the Sengkang Grand Residences integrated development. Sengkang has Compass One. Punggol has Waterway Point, which opened in 2016 and remains the primary retail anchor for the northern end of the line.

Hougang was the gap. Sitting between Serangoon and Buangkok, Hougang Central’s only major retail offering has been Hougang Mall, a shopping mall that opened in 1997 — pre-dating the MRT station — and is not physically connected to the station.

The upcoming Hougang Central development fills this gap with a landmark retail component that will be the largest mall in Hougang, directly integrated with the MRT station, a new bus interchange, and a new town plaza. At that scale, it has the strength to transform Hougang into a destination on the NEL in its own right.

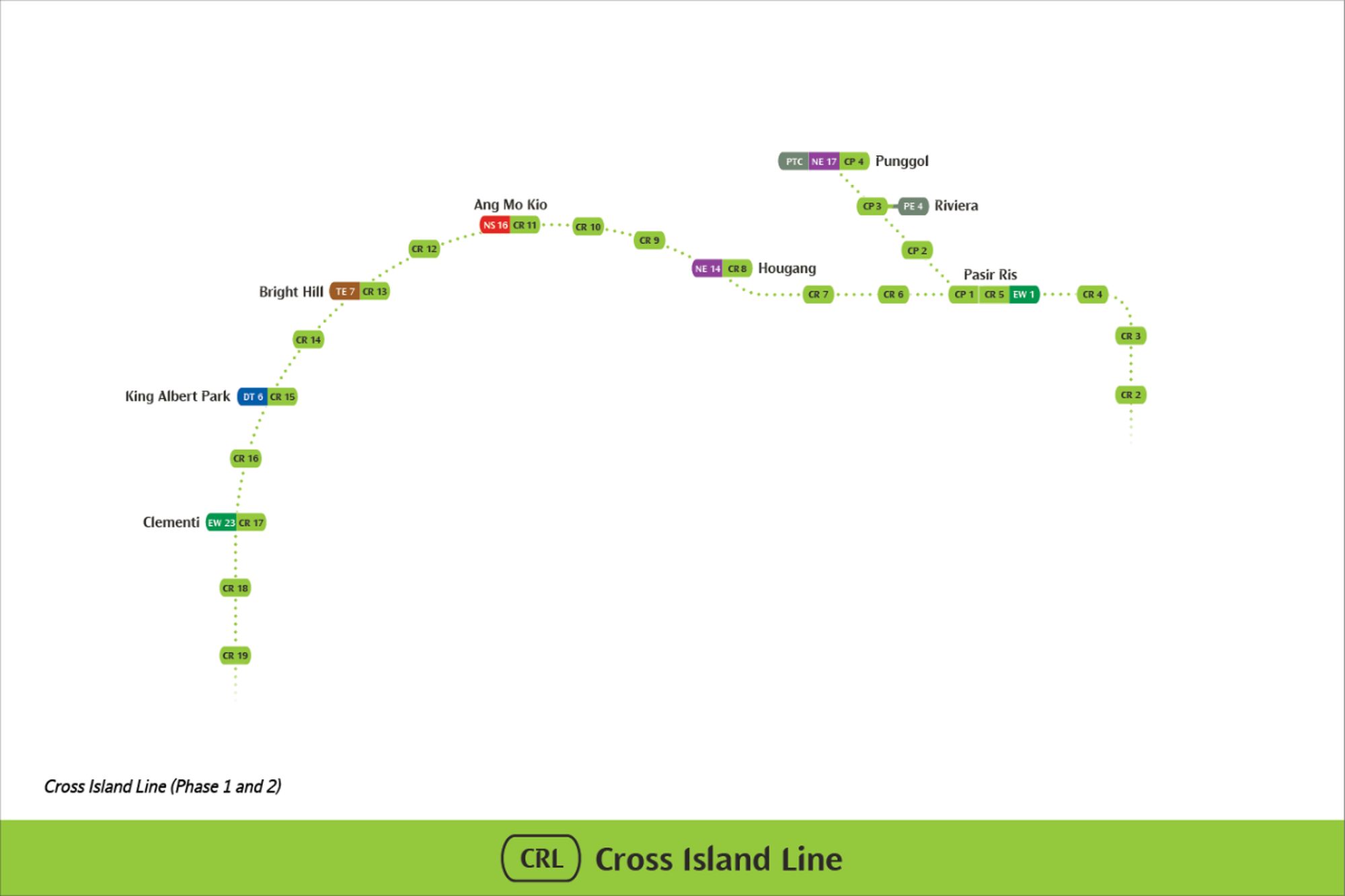

The next factor is the future Cross Island Line (CRL). Hougang is the only one of the 12 planned stations along that line which will intersect with the NEL.

Across all CRL stations in Phase 1 and the later Punggol extension, the only other interchange where an integrated development with a residential component sits directly above the tracks is Pasir Ris 8, at Pasir Ris MRT station. AMK Hub at Ang Mo Kio and Waterway Point at Punggol are retail without residential, while Bright Hill has no integrated development above it at all.

Hougang Central combines what none of the other CRL interchanges does: NEL access, CRL access, and 830 residential units in a single purpose-built development above the station.

By comparison, Nex at Serangoon is linked to the existing NEL–Circle Line interchange. But the area is one of the most expensive suburban residential submarkets in the region in terms of median psf prices.

“Hougang MRT‘s vicinity doesn’t have a well-connected project; there are only two comparable projects nearby, Riverfront and Florence,” says Norman Koh, a property agent in Stacked’s consultancy team.

He adds that Hougang has always been a strong demand location, especially District 19 in general, with multi-generational families. There are also no integrated projects in the Hougang/Kovan estate, so the upcoming integrated project is set to attract retirees, young adults, and families.

Meanwhile, Grady Chew, also a property agent in Stacked’s consultancy team, frames it as a supply constraint. “It’s fundamentally scarcity. Normal GLS residential plots come up regularly, but an integrated development with residential, commercial space, and an MRT station — there is only space for one at each station,” he says.

Chew also points out that this site also gets a dual-line interchange, which makes it even harder to replicate elsewhere. “Buyers who prioritise convenience, or who are aligned with Singapore’s car-lite planning direction, will find very few options that match what this represents,” he says.

The pool of HDB upgraders

Most of the expected buying demand for any large new suburban launch typically stems from households that are capitalising on hefty HDB resale proceeds. In Hougang, that pool of buyers has been progressively accumulating over the past six years or so.

In 4Q2019, the median price for a four-room HDB flat in Hougang transacted at around $388,000. By 4Q2025, that resale figure had reached $612,900, reflecting a nearly 58% increase over six years.

For five-room flats, the price trajectory moved from a median of $489,000 to $795,000, an over 62% increase across the same period.

Hougang HDB Resale Median Prices

| Year | 4-Room Median | 5-Room Median |

| 2019 Q4 | $388,000 | $489,000 |

| 2020 Q4 | $410,000 | $521,500 |

| 2021 Q4 | $471,000 | $585,000 |

| 2022 Q4 | $518,000 | $627,500 |

| 2023 Q4 | $560,000 | $655,000 |

| 2024 Q4 | $615,000 | $760,000 |

| 2025 Q4 | $612,900 | $795,000 |

Based on data compiled by Stacked, prices are higher in streets immediately surrounding the new development site. Hougang Central and Hougang Avenue 10, which bound the GLS site directly, have seen average resale prices rise by over 43% and 54% respectively since 2015. The broader cluster of surrounding streets, Avenues 4, 6, and 8, has appreciated by broadly similar margins over the same period.

Average HDB Resale Prices Near Hougang MRT (All Flat Types)

| Year | HOUGANG AVE 10 | HOUGANG AVE 4 | HOUGANG AVE 6 | HOUGANG AVE 8 | HOUGANG CTRL |

| 2015 | $433,741 | $417,305 | $473,625 | $391,296 | $612,919 |

| 2016 | $461,160 | $401,377 | $507,419 | $375,304 | $635,492 |

| 2017 | $457,942 | $397,794 | $485,961 | $405,424 | $607,187 |

| 2018 | $489,062 | $420,591 | $517,020 | $400,919 | $656,997 |

| 2019 | $445,895 | $367,625 | $524,514 | $392,125 | $581,814 |

| 2020 | $464,900 | $399,630 | $543,568 | $410,112 | $677,150 |

| 2021 | $549,286 | $457,994 | $546,988 | $445,240 | $729,636 |

| 2022 | $544,825 | $480,042 | $567,346 | $486,271 | $770,364 |

| 2023 | $604,212 | $510,778 | $599,942 | $537,265 | $843,250 |

| 2024 | $686,444 | $634,960 | $699,392 | $563,203 | $792,980 |

| 2025 | $668,069 | $620,270 | $733,871 | $601,682 | $879,457 |

| % change from 2015 (or earliest available data) to 2025 | 54.02% | 48.64% | 54.95% | 53.77% | 43.49% |

One stop north at Buangkok, where Jewel @ Buangkok and Sengkang Grand Residences are located, HDB prices in the surrounding Compassvale estate have followed a similar trajectory. Compassvale Bow, Compassvale Link, and Sengkang Central have each risen by 63%, 53%, and 57% respectively since 2015.

Average HDB Resale Prices Near Buangkok MRT (All Flat Types)

| Year | COMPASSVALE BOW | COMPASSVALE LINK | SENGKANG CTRL |

| 2015 | $494,308 | $509,263 | $508,725 |

| 2016 | $475,652 | $510,708 | $499,436 |

| 2017 | $477,100 | $496,596 | $495,295 |

| 2018 | $500,491 | $505,722 | $507,200 |

| 2019 | $482,077 | $513,220 | $515,524 |

| 2020 | $476,722 | $528,287 | $531,951 |

| 2021 | $611,428 | $554,382 | $551,434 |

| 2022 | $641,770 | $599,050 | $607,334 |

| 2023 | $707,193 | $673,375 | $676,077 |

| 2024 | $752,182 | $720,016 | $743,146 |

| 2025 | $806,877 | $780,893 | $802,903 |

| % change from 2015 (or earliest available data) to 2025 | 63.23% | 53.34% | 57.83% |

How Riverfront Residences And The Florence Residences Are Positioned Today

The two largest condo projects near the Hougang Central site are Riverfront Residences, a 1,472-unit 99-year leasehold development along Hougang Avenue 7 that launched in 2018, and The Florence Residences, a 1,410-unit 99-year leasehold project along Hougang Avenue 2 that launched in 2019. Both are fully sold out.

Based on URA caveats, median psf prices across all units at both projects have been on a steady upward trajectory since 2021.

Annual Median $PSF: Riverfront Residences And The Florence Residences

| Year | Riverfront Residences | The Florence Residences |

| 2021 | $1,394 | $1,695 |

| 2022 | $1,512 | $,1734 |

| 2023 | $1,636 | $1,779 |

| 2024 | $1,664 | $1,773 |

| 2025 | $1,738 | $1,796 |

| 2026 (YTD) | $1,747 | $1,877 |

For reference, median three-bedroom units in Riverfront Residences and The Florence Residences have been changing hands for approximately $1.62 million and $1.85 million, respectively.

The price gap between these current resale psf levels and a likely $2,500+ psf new launch quantum is substantial. The experience from the sales launch of Sengkang Grand suggests that the gap can narrow over time, rather than simply persist.

But the pace and extent of any repricing will depend on how the area’s profile shifts after the integrated development opens and after the CRL interchange becomes operational, both of which are several years away.

The transaction data also seems to suggest that most sellers in Riverfront Residences and The Florence Residences are not currently pricing in a CRL premium. That positioning may change as the opening date of the new MRT line approaches.

Koh sees the price gap as the primary mechanism, saying: “To a large extent, given there is a price gap based on the developer’s land bid price. And based on historical buyer behaviour, the surrounding projects will gain the benefits of an MRT interchange and a new mall.”

But Chew draws a finer distinction, saying: “It is two different products at different price points — the launch itself may not move surrounding condo prices dramatically.” He opines that what could happen is that when buyers see new launch pricing at that level, resale units nearby will look like good value.

“Once Hougang Central is built and operational, it becomes the dominant product in the area. The condos most at risk are those closest in proximity that are not well-maintained or have compromised layouts. The ones that will hold up best are those with differentiated attributes — river views, larger unit sizes, proximity to good schools,” says Chew.

When To Sell

For owners of existing condos near the Hougang Central site who are weighing their exit timing, Koh identifies three distinct windows. “This opportunity presents a few exit points. First, ride on Hougang Central’s preview sales. Second, when the project TOPs. Third, when the MRT interchange with the CRL is completed. The lack of supply in the Hougang area is the main fuel for demand across all three windows,” he says.

On the other hand, Chew has a more front-weighted perspective. “Before launch and during launch — that is when buyers are around, looking at both new launches and resale. Once new launch pricing is released, and if buyers are priced out, they would go for the resale. Or if their queue number is not favourable, they would also secure the resale. Ride the hype and demand. Not the aftermath.”

Both perspectives describe the same underlying dynamic from different angles. The Hougang Central launch creates a concentrated window of buyer attention in the precinct.

The point made by Chew that the resale market benefits most from the period when the new launch is actively selling is consistent with what the transaction data, as evidenced by the launch of Sengkang Grand, illustrates. Namely, the sharper repricing in The Quartz and Esparina happened during and shortly after the period when Sengkang Grand was the active conversation in the market.

What This Depends On

A crucial variable is pricing. At a land rate of $1,179 psf ppr, it is possible that CapitaLand and UOL will need to price the residential component substantially above current resale benchmarks to recoup that capital investment.

Price estimates that put a potential price of above $2,500 psf imply a two-bedroom unit that would fetch above the $1.5 million mark, and a three-bedroom unit well above $2 million threshold.

At these prices, the pool of buyers that directly stem from HDB upgraders may be narrower than what was seen at Sengkang Grand, which launched at $1,747 psf in 2019 when the area’s HDB price base was considerably lower.

On the other hand, the CRL variable works in the other direction. At Sengkang Grand, Buangkok is a single-line station. But the new integrated development at Hougang Central will open into a dual-line interchange, a category with no precedent in the OCR.

It is not clear how buyers might price this improved connectivity, compared to Serangoon–Nex. But what the transaction data during and after the launch of Sengkang Grand tells us is that the spillover effect from the launch of a new integrated development does translate into a price uplift, and that projects positioned below the new price ceiling have historically been the ones that benefited from this appreciation.

Whether the gap between $1,700 psf and $2,500+ psf in Hougang closes as quickly as the comparable gap did in Sengkang will depend on market conditions that are several years out. The CRL timeline, take-up rate at the new launch, and the broader OCR price environment will all play a role.

But for owners already holding units in the precinct, the strong argument of a dual-line interchange, 300,000 sq ft of integrated retail, and the area’s first large new launch in seven years is not difficult to follow.

Commentary like this is useful for understanding the broader market. The harder part is applying those ideas to a specific property, budget or decision you’re actually considering.

That’s often where a second opinion becomes valuable.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

0 Comments