Traditionally, cities have been neatly organised into dedicated zones, and Singapore’s development plan has also embraced this land planning approach.

Perhaps it was a response to our rushed housing needs in the post-Independence years, or perhaps it was a memory of how “messy” urban development during colonial Singapore was – with homes drowned in the noise and traffic from shops or warehouses right next door. But from around the 1960s to 1990s, Singapore was divided into very neat, clear-cut urban zones, and that resulted in:

- Jurong = Industrial

- CBD = Offices

- Orchard = Malls

- Changi = Anything related to planes

- Sentosa = High-end Tourism

- Pasir Ris = Chalets

These broad characterisations have shaped the way most Singaporeans view these locations. To some degree, these identities persist today, but you might notice they’ve also evolved in recent years.

A familiar example is Jurong which was initially “just” for industrial zones. Today, Jurong East is envisioned as the “second CBD,” whilst the Jurong Lake area has taken on a much stronger mixed-use colour. One of the newest GLS sites in the 2H2026 Confirmed List is at Town Hall Link, this mega-white site could yield 1,200 homes alongside offices, retail, and hotels.

We saw other examples of these hubs forming in city-fringe regions: Paya Lebar was once known for old shophouses, light industry areas, and the former airport. Today, it’s one of the largest regional commercial hubs in Singapore, and supports a growing residential population.

The development of Punggol and Sengkang also fits this trend. Once the definition of “ulu”, the development of new homes and the completion of the new Punggol Digital District has seen the area anchored by educational institutions, business parks, and future-forward digital industries.

The evolution in our urban landscape broadly began with URA’s concept plan in 1991

By then, Singapore was already building new towns and industrial estates, but the idea of creating multiple business centres outside the CBD was a novel concept at the time.

One can imagine the reaction of telling people back then that Jurong or Punggol might one day be commercial and residential hubs, would have been along the lines of:

Subsequent iterations of the concept plan, from 2001 onwards, accelerated the drive towards decentralisation. It was clear, more than two decades ago, that the previous urban development approach of highly specific zones (i.e., all offices in the CBD, all shopping in Orchard, all residential in Punggol, and so forth) wasn’t going to work to meet Singapore’s future needs. Not least because of Singapore’s transport infrastructure: our buses and trains can’t handle a growing population who surge in and out of a given central area on the same time schedule.

If you’re one of the people who has to commute to the CBD in the morning, you probably know how ridiculous the MRT situation can get.

Simply put, if almost every prime office building is in the CBD, every major retailer is in Orchard Road, and residential areas populate the rest of the island, Singapore quickly runs into physical limits. Cars, trains, and buses will all end up stuck at massive chokepoints.

So, it was clear that the idea was to develop different regional hubs, such as Paya Lebar Quarter, the Tampines Central node, Jurong East, and Punggol Waterway was essential. It took a long time and it paid off – but from what we’ve seen with recent Government Land Sales (GLS) sites, that was only the beginning.

It’s now clear that the plans to decentralise Singapore doesn’t end at building different hubs – it’s also about changing the nature of existing, high-value neighbourhoods.

Many of the newest GLS sites are not located in city-fringe regions. They’re located in places that are already valuable or already central:

- Marina South

- Tanjong Rhu

- The Greater Southern Waterfront

- Holland Plain

These are different from the previously developed regional centres and hubs, in that these locations are already relatively established.

For example, Marina South. When the development plans for the waterfront precinct were first announced, most casual observers viewed it as little more than an extension of Marina Bay. But now we’re looking at a third residential GLS site in this district. This is no longer about creating more offices or shops near Marina Bay; the government wants a resident population large enough to support shops, amenities, schools, and community life.

Even Tanjong Rhu represents a subtle shift. Once viewed as a private residential enclave, the area is becoming more integrated with the wider city through the Thomson-East Coast Line (TEL), Kallang Alive, East Coast Park, and new HDB estates. Incidentally, this also does a lot to balance out the area, as prior to the upcoming HDB clusters there wasn’t much here in the way of retail or entertainment.

Tanjong Rhu is close to the city centre, but is rarely a destination in and of itself if you don’t live there.

News pieces like this explain what's happening in the market. Our consultations are designed to help you understand what it means for your own property decisions.

If you're considering buying, selling or upgrading, we'd be happy to help you work through your options.

There are two important points to note about this shift:

The first is Singapore’s long-standing emphasis on social integration. This is already very clear in the development of new HDB flats, for instance, where we include rental housing in pricier Prime and Plus estates.

But now we see this on a broader scale, with developers incentivised to build homes that are affordable in the Rest of Central Region (RCR) and Core Central Region (CCR).

Consider the recent wave of CCR launches. In the past, developers often assumed that buyers in central locations would prioritise luxury, prestige, and space. Large units were common, as the target audience was either wealthy Singaporeans or foreign buyers with deep pockets.

Today, the approach appears very different.

Projects such as River Modern, Promenade Peak, and One Marina Gardens have deliberately been priced within reach of local buyers. This has occurred alongside the 60% ABSD imposed on foreign buyers and entities, which has fundamentally changed the profile of the typical CCR purchaser.

Till now, many CCR districts have been dominated by transient populations: expatriates, investors, tenants, and wealthy households who own multiple properties. They’ve functioned more as prestige addresses than communities.

But if the current trend continues, we may see a day when these neighbourhoods develop stronger community identities like the heartlands; places where people grow up, attend school, and remain connected to the area. Qualities we see in places like Ang Mo Kio, Bedok, Tampines, or Sengkang.

I’m not saying that’s going to happen anytime soon, but that the trends we are observing lay the groundwork.

To make that happen though, we’re also seeing a shift in our approach towards aspects of urban planning

Planning zones increasingly favour mixed-use rather than specialisation. In our grandparent’s era, the ideal city was one where homes, offices, shops, and industries were neatly separated.

Today the goal has shifted from single-function districts, to districts that remain active throughout the day. This explains why so many of the recent GLS sites involve a combination of residential and commercial elements.

The Town Hall Link site in Jurong aside, we’ve also seen it in play out in one-north. Consider the launch of Hudson Place Residences and Bloomsbury Residences, both of which reflect awareness of how the profile of the area is changing.

The initial development of one-north began with several research and business park areas taking root, and it was anchored by developments such as Biopolis and Fusionopolis, and the nearby JTC Launch Pad. Since then, we’ve seen how subsequent phases in the master plan of one-north introduced more residential enclaves that are turning one-north a genuine neighbourhood.

This isn’t a uniquely Singaporean innovation, it’s been proven to work in other countries with mature and highly developed urban centres as well.

Back in 2022, I wrote about Japan’s zoning system and how it differs from Singapore’s. One of the key observations was that Japanese neighbourhoods are more flexible in their mix of uses. Residential areas can naturally incorporate offices, shops, clinics, schools, and other amenities, resulting in districts that remain active throughout the day.

Singapore’s approach is much more structured, though our direction appears increasingly similar.

This has happened in the Netherlands too. In Amsterdam and Rotterdam, former docklands such as the Eastern Docklands were redeveloped from port and industrial uses into mixed-use neighbourhoods with housing, retail, and cultural spaces.

Even the United States, which popularised strict zoning in the 20th century, has spent the past decade trying to reverse those policies. It’s an amusing coincidence that Hudson Place Residences is influenced by Hudson Yards in New York City; since much like One-North, Hudson Yards was a former rail yard that’s now being redeveloped into a mixed-use district.

So what does this mean for Singaporean homebuyers?

For starters, we can expect more integrated or mixed-use developments to crop up, since they’re a natural fit for this diverse neighbourhood development approach. I, for one, am expecting many more future debates about whether the higher $PSF for the local integrated project is “worth it.”.

That aside, the bigger lesson may be that buyers need to look beyond what a location is offering today.

Twenty years ago, many buyers viewed Jurong East as primarily an industrial area. Few would have predicted that it would one day be on the path towards becoming home to one of Singapore’s largest commercial regional centres. However, this also works both ways: an area that’s a major commercial hub now can’t be assumed to stay that way either. Recall that as early as 2017, there was already speculation about Orchard Road’s diminishment; and it may have prompted the Orchard rejuvenation project.

We see similar shifts elsewhere today. Marina Bay is no longer being planned purely as a financial district, One-North is no longer merely a research and business park, the Greater Southern Waterfront is no longer solely about HDB flats that may have a nicer view. The identity of different Singapore neighbourhoods, and what they’re “good” or “bad” for is much less fixed compared to the past.

The upside is that URA is unusually transparent compared to most cities. We get Concept Plans, Master Plans, GLS programmes, Draft Master Plans, or ministerial speeches.

So there’s no reason to be the type of buyer who only looks at what exists today. Check the available urban planning information, just as much as you check price growth and public transport accessibility.

Meanwhile in other property news…

- How would you like to own a home across from the Istana itself? Cavanagh Fortuna is up for grabs, and it’s possible for someone to own the entire small project.

- As also mentioned above, here is the list of GLS sites for the second half of 2026. We’ve reviewed them in detail for you.

- Will you always make money with a new launch? Okay, it generally does happen, but that doesn’t mean exceptions don’t occur; and there are nuances to understand.

- Orchard versus River Valley: which of these two titans are the best place to buy a home? Join our Stacked Pro readers as we examine the subtleties of each neighbourhood.

Weekly Sales Roundup (25- 31 May)

Top 5 Most Expensive New Sales (By Project)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| RIVER MODERN | $6,147,000 | 1830 | $3,359 | 99 yrs (2025) |

| THE CONTINUUM | $5,473,000 | 2034 | $2,690 | FH |

| TERRA HILL | $4,797,000 | 1862 | $2,576 | FH |

| ELTA | $3,906,000 | 1776 | $2,199 | 99 yrs (2024) |

| NEWPORT RESIDENCES | $3,564,000 | 980 | $3,639 | FH |

Top 5 Cheapest New Sales (By Project)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| TENGAH GARDEN RESIDENCES | $1,238,000 | 624 | $1,983 | 99 yrs (2025) |

| UNION SQUARE RESIDENCES | $1,376,000 | 506 | $2,720 | 99 yrs (2024) |

| THE SEN | $1,531,000 | 678 | $2,258 | 99 yrs (2025) |

| HUDSON PLACE RESIDENCES | $1,656,000 | 646 | $2,564 | 99 yrs |

| BLOOMSBURY RESIDENCES | $1,731,000 | 678 | $2,553 | 99 yrs (2024) |

Top 5 Most Expensive Resale

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| SEVEN PALMS SENTOSA COVE | $13,380,000 | 4273 | $3,131 | 99 yrs (2007) |

| ARDMORE PARK | $11,050,000 | 2885 | $3,830 | FH |

| BEVERLY HILL | $9,580,000 | 3778 | $2,536 | FH |

| GRANGE RESIDENCES | $8,400,000 | 2583 | $3,252 | FH |

| LEEDON RESIDENCE | $7,550,000 | 2669 | $2,828 | FH |

Top 5 Cheapest Resale

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| THE PLAZA | $660,000 | 474 | $1,394 | 99 yrs (1968) |

| RIVERBAY | $660,000 | 388 | $1,703 | 999 yrs (1882) |

| PARC SOMME | $666,000 | 344 | $1,934 | 99 yrs (2008) |

| KEMBANGAN SUITES | $750,000 | 420 | $1,787 | FH |

| THE ALPS RESIDENCES | $765,000 | 506 | $1,512 | 99 yrs (2015) |

Top 5 Biggest Winners

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | RETURNS | HOLDING PERIOD |

| ARDMORE PARK | $11,050,000 | 2885 | $3,830 | $3,500,000 | 17 Years |

| THE DAIRY FARM | $3,500,000 | 1948 | $1,796 | $2,400,000 | 31 Years |

| SHELFORD VIEW | $5,880,000 | 3122 | $1,884 | $2,000,000 | 11 Years |

| GRANGE RESIDENCES | $8,400,000 | 2583 | $3,252 | $1,920,000 | 15 Years |

| VALLEY PARK | $4,648,000 | 1808 | $2,570 | $1,698,000 | 9 Years |

Top 5 Biggest Losers

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | RETURNS | HOLDING PERIOD |

| THE SCOTTS TOWER | $1,880,000 | 872 | $2,156 | -$1,078,400 | 9 Years |

| MARINA BAY SUITES | $4,080,000 | 2056 | $1,985 | -$774,000 | 16 Years |

| OUE TWIN PEAKS | $1,100,000 | 570 | $1,928 | -$530,776 | 10 Years |

| PATERSON SUITES | $4,500,000 | 1744 | $2,581 | -$273,000 | 15 Years |

| MARINA ONE RESIDENCES | $1,300,000 | 764 | $1,701 | -$185,000 | 5 Years |

Top 5 Biggest Winners (ROI%)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | ROI (%) | HOLDING PERIOD |

| WU DE BUILDING | $1,600,000 | 1259 | $1,270 | 330% | 20 Years |

| THE DAIRY FARM | $3,500,000 | 1948 | $1,796 | 218% | 31 Years |

| PARKVIEW APARTMENTS | $1,100,000 | 1119 | $983 | 168% | 23 Years |

| THOMSON IMPERIAL COURT | $1,938,000 | 1281 | $1,513 | 158% | 26 Years |

| COTE D’AZUR | $2,050,000 | 1152 | $1,780 | 147% | 19 Years |

Top 5 Biggest Losers (ROI%)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | ROI (%) | HOLDING PERIOD |

| THE SCOTTS TOWER | $1,880,000 | 872 | $2,156 | -37% | 9 Years |

| OUE TWIN PEAKS | $1,100,000 | 570 | $1,928 | -33% | 10 Years |

| MARINA BAY SUITES | $4,080,000 | 2056 | $1,985 | -16% | 16 Years |

| MARINA ONE RESIDENCES | $1,300,000 | 764 | $1,701 | -13% | 5 Years |

| PATERSON SUITES | $4,500,000 | 1744 | $2,581 | -6% | 15 Years |

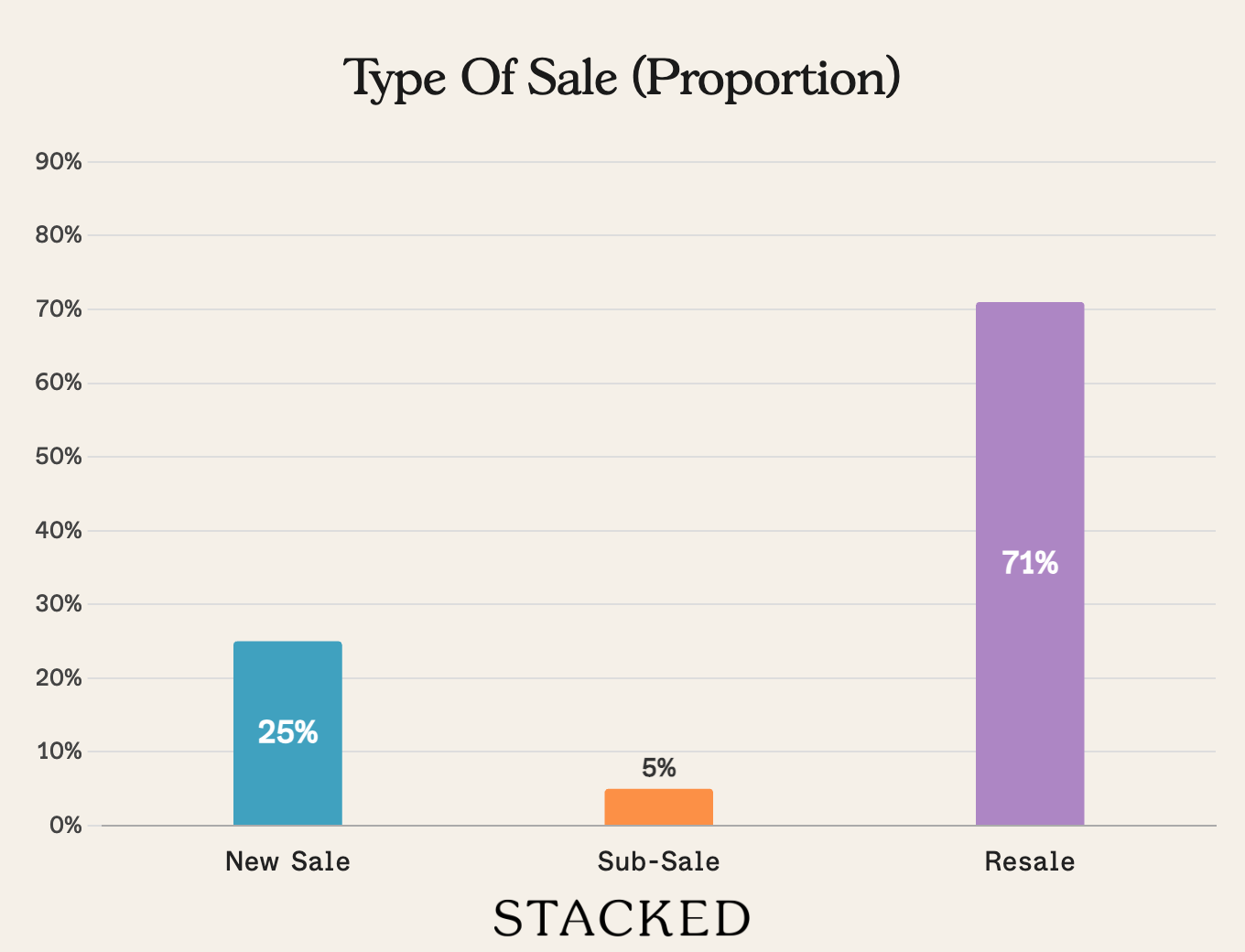

Transaction Breakdown

Follow us on Stacked for more news and updates on the Singapore property market.

A single headline is rarely enough to change your plans. The value comes from understanding how today’s news fits into the broader direction of the market.

If you’d like to talk through what a shift like this means for your own timing, purchase, or exit, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

0 Comments