This contributed article was written by Sebastian Sieber, founder of Cashew (www.cashew.sg), a Singapore-based digital mortgage platform.

If you speak to a large enough group of Singaporean homeowners, most of them would probably say that the HDB concessionary loan is the safest option when it comes to financing a home purchase, while some might view bank loans as the riskier way to go.

Once they purchase their home and start living in it, most property owners also never revisit this perception. But according to our experience in the market, for property owners who intend to sell their unit in three to five years time, that ranking is usually upside down.

When we compare the different loan packages available on the market, the certain fixed packages from the right banks could cost you less in terms of interest payments, while exposing you to less risk on the way out as compared to staying with a HDB loan.

What makes this work is a clause that rarely gets enough airtime and awareness among property owners: the penalty waiver on a sale. To help us understand this, here are two financing routes as they stand, as of mid-2026.

| HDB concessionary loan | Bank fixed package (best in market) | |

| Interest rate | 2.6% p.a. | from 1.60% p.a. |

| Lock-in period | None | 1 – 5 years |

| Redemption Penalty if you sell | None | Typically 1.5%, waived on the right packages |

Market commentary like this is only useful if you can translate it into what it means for your own purchase: your entry price, holding period and exit options.

That's where many buyers get stuck. General market insights rarely tell you whether a specific unit, at a specific price, is the right decision for your circumstances.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

The Exit-Risk Myth

The anchor that tends to keep most sellers on a HDB loan is the lock-in penalty. But a typical bank loan package usually locks you in for a certain duration and charges roughly 1.5% of the outstanding balance if you leave early as a redemption penalty

This means that on a S$400,000 loan this works out to about S$6,000, which seems like reason enough to steer clear of banks when you’re preparing to sell your property.

However, this reasoning falters once we scrutinise the clause that governs it. We found that several banks in Singapore usually drop the redemption penalty when the transaction is a true sale of the property rather than a way to refinance with a rival lender.

So it’s possible for you to sell your property, realise the capital gain, and the penalty never bites. If you play it right, this means that you could hold the lower rate for as long as you keep the flat, then leave cleanly when the sale is completed.

Let’s take a look at the common beliefs among most Singaporean home owners, against what the terms of a package actually means for someone who is selling.

| The common belief | The reality for a confirmed seller |

| Bank loans trap you with early-exit penalties. | On the right package, the penalty is waived in full on a genuine sale. |

| Only HDB loans shield you from rate swings | A fixed term covers a seller’s whole horizon, and at a lower rate. |

| Bank loans always cost more than HDB loans. | Over the last 21 years, bank loans were cheaper about 78% of the time; As of May 2026 a bank loan is about one percentage point cheaper. |

How Do The Sale Waivers Actually Compare?

Next, let’s take a look at the sale waivers across some well-known banks in Singapore, across existing two-year fixed packages for completed HDB flats.

The waiver column determines whether a bank loan is safe for a seller, and it’s one of the most important details that is the hardest to pin down publicly.

Here are three examples of packages on the market for a loan amounting to $500,000.

| Bank | Fixed rate | Lock-in | Penalty | Penalty waiver if you sell |

| UOB | 1.65% | 3 years | 1.5% | 50% waived on sale, remaining 50% waived when you return to UOB with a new loan package. |

| OCBC | 1.98% | 5 yrs | 1.5% | Full waiver on a genuine sale after 12 months. |

| DBS | 1.78% | 2 yrs | 1.5% | Full waiver on a genuine sale. |

The headline mortgage rate and how safely could a seller dispose of their property are two different questions. Two lenders could post the same rate, but only one lets a seller walk away penalty-free.

In general, the partial waiver is designed to keep you in as a customer, so it’s designed to incentivise owners to return to that bank. But if you pick a loan package based on the headline mortgage rate alone, there’s a chance that you might land on a package that punishes the very thing you had planned to do.

Why Staying On A HDB Loan ‘Just To Be Safe’ Can Cost More Money

The HDB concessionary rate has held firm at 2.6% since 1999, it is pegged at 0.1% above the CPF Ordinary Account (OA) rate. For a first-time Build-To-Order (BTO) home owner who is still waiting for the project to be completed, that ‘fixedness’ is genuinely valuable.

On the other hand, for a buyer with a clear intention to sell once the flat reaches its minimum occupation period (MOP), with a firm sale date and the flat already in hand, it is a premium paid for protection they no longer need.

Today, based on our compilation of various mortgage rates available on the market, the gap between a HDB loan and most bank loans is close to a full percentage point: 2.6% on a HDB loan compared to approximately 1.65% on a fixed loan package by a bank.

The spread, or gap in the interest rates, also compounds across each year you continue to hold on to the property. To help visualise this, here’s how it might play out on a $400,000 loan with 25 years left. We examine a HDB loan against a 1.65% bank package for a property that is held until it is sold.

| Sell at | Interest paid on HDB (2.6%) | Interest paid on bank (1.60%) | Interest saved |

| Year 3 | about S$29,900 | about S$18,900 | about S$11,000 |

| Year 5 | about S$48,200 | about S$30,300 | about S$17,900 |

| Year 7 | about S$65,200 | about S$40,800 | about S$24,400 |

Assumes the bank rate is re-fixed at a similar level after the initial two-year term. A more conservative re-fix at 1.80% still saves roughly S$10,900, S$16,700 and S$22,200 over the same windows.

When Does The Higher-Risk Logic Hold True?

There are occasions when a bank loan is not the safer choice, and the degree of exposure depends on the interest rate movement after the fixed term ends.

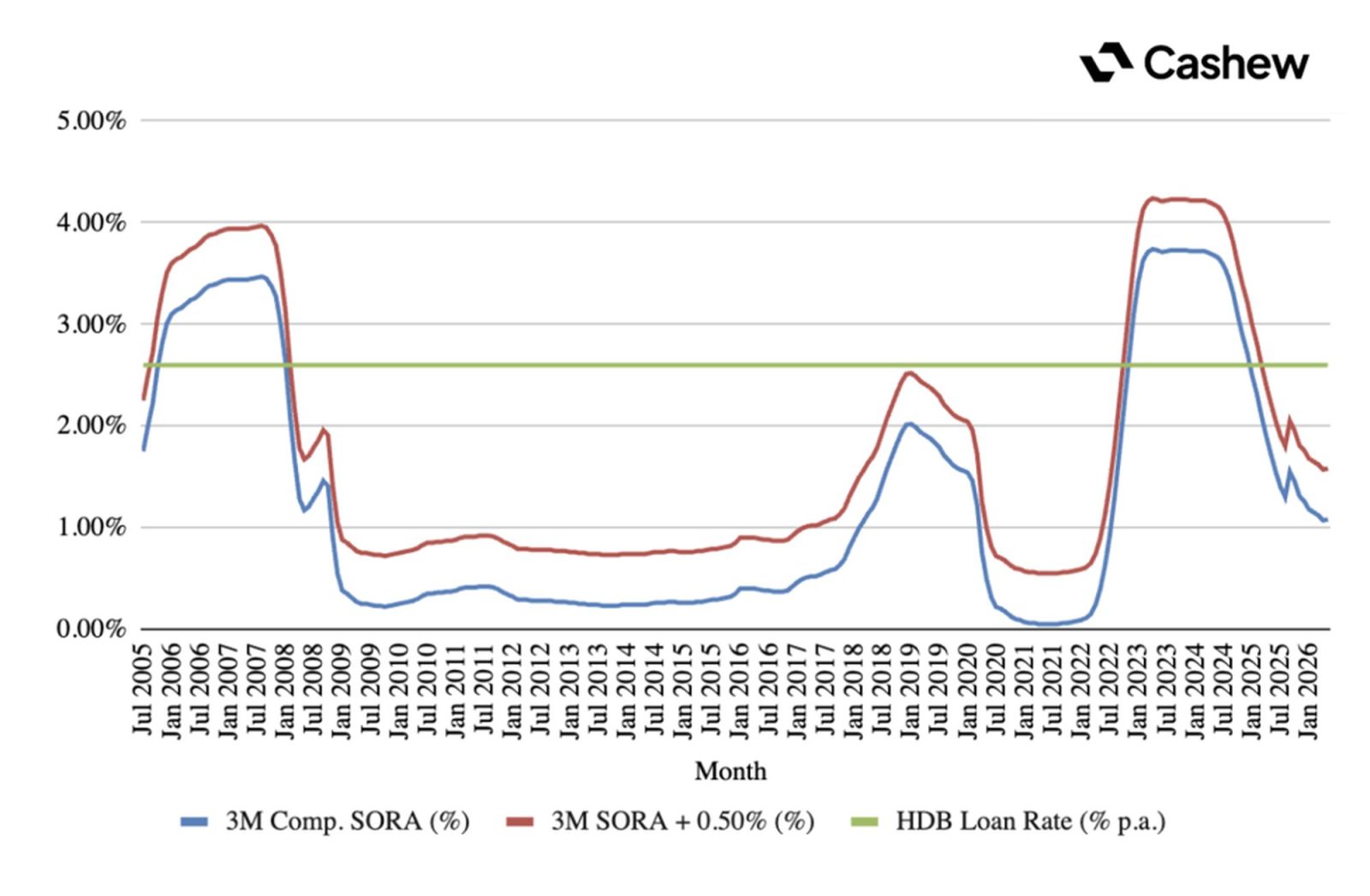

For sellers with a more open-ended timeline to sell their property, there is a chance that you could refinance several times across a 20-year tenure. This means riding through each cyclical movement in the Singapore Overnight Rate Average (SORA), including any spikes that may occur.

According to the financial data, there have been two relatively recent periods in Singapore’s interest rate history when the bank rate sat above 2.6% and HDB borrowers paid less. The first took place from September 2005 to January 2008, and the next period was from October 2022 to February 2025. Each of these time periods lasted 29 months.

Sellers without a firm date to sell their property are much more exposed to these interest rate events. On the other hand, a seller with a definite three- to five-year horizon is generally protected from this, since the fixed rate blankets nearly all of the planned holding period.

The other cost faced by sellers is that the move is one-way. Once you shift from a HDB loan to a bank loan, you cannot shift back. For a seller who is fixed on exiting their property that is a moot consideration since the loan ends at the sale completion either way.

However, other sellers who might hold the flat for decades, it becomes a very real consideration.

The Long View Backs This Up

This is not just a snapshot of an unusually low-rate moment in the interest rate environment.

If we look across the monthly three-month (3M) compounded SORA series from July 2005 to May 2026, a bank loan priced at SORA + 0.5% was cheaper than the 2.6% HDB rate for 191 of the 251 months in that period – or about 76% of the time.

Our analysis suggests that the exceptions are tidy and symmetric, with two 29-month long stretches – in 2005 to 2008, and another in 2022 to 2025 – that account for nearly all of the months in which a HDB loan came out ahead.

During those periods, the average bank rate was about 1.8%. This swung from 0.55% at the post-crisis floor after the Covid-19 pandemic to a peak of 4.24% in 2023, while the HDB rate never moved off 2.6%.

Recently, the bank rate has sat below 2.6% every month since April 2025, with the 3M SORA down around 1.08% by May 2026. On a S$500,000 loan over 20 years, the difference is large.

| Loan type | Average rate | Interest paid over 20 yrs | Difference |

| HDB loan | constant 2.6% | about S$141,700 | — |

| Bank loan (3M SORA + 0.5%) | variable; averaged about 1.8% (ranging 0.55%–4.24%) | about S$95,800 | about S$45,900 less |

Frequency and rates from the monthly 3M compounded SORA series, July 2005 to May 2026 (251 months); Interest modelled on a S$500,000 loan over a 20-year tenure (June 2006 to May 2026).

In our view, for a long-term homeowner, the history of Singapore’s interest rate movement presents a strong case for refinancing after collecting the keys to your home and riding the market cycles. Meanwhile, there is a more straightforward message for sellers: lock in today’s low fixed rate, confirm the sale waiver is in place, and let the lower rate do its work over the few years you have left in the flat.

Our Key Takeaway

For a homeowner with a firm plan to sell in the next three to five years, a bank fixed-rate package with a sale waiver is usually both the cheaper and the lower-risk option. The penalty that makes bank loans feel dangerous is exactly what the waiver removes, and the interest saved against the 2.6% HDB rate runs into five figures even on a modest loan.

In our view, the mistake is not switching to a bank loan. Staying on HDB financing out of habit and picking a package based on its headline rate without checking the one clause that actually matters to a seller could also be viewed as a mistake in this case.

Don’t forget that each situation is different, and the right move depends on your loan size, your timeline, and the exact terms of the package in front of you. If you are weighing a sale in the next few years it pays to check the numbers before you commit.

Cashew is an independent, tech-enabled digital mortgage platform that compares home loan packages across all banks in Singapore and pairs you with an advisor who handles the rest, from paperwork to approval. It’s free to use, with no cold calling, and because Cashew isn’t tied to any bank, the recommendation is based on what fits you best.

Commentary like this is useful for understanding the broader market. The harder part is applying those ideas to a specific property, budget or decision you’re actually considering.

That’s often where a second opinion becomes valuable.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

0 Comments