Historically, demand in Singapore’s office market is shaped by a trait among corporate occupiers to move into the newest and most premium office spaces when they become available. This flight-to-quality continues to shape the office market over the first three months of this year.

In 1Q2026, Central Business District (CBD) Grade A office rents reached $11.36 psf per month (pm), which is a quarterly increase of 1.4%. This is based on gross effective rents across a basket of Grade A office buildings located in Marina Bay, Raffles Place, Shentown Way, Tanjong Pagar, City Hall, Orchard Road, and Bugis – and compiled by Cushman & Wakefield (C&W).

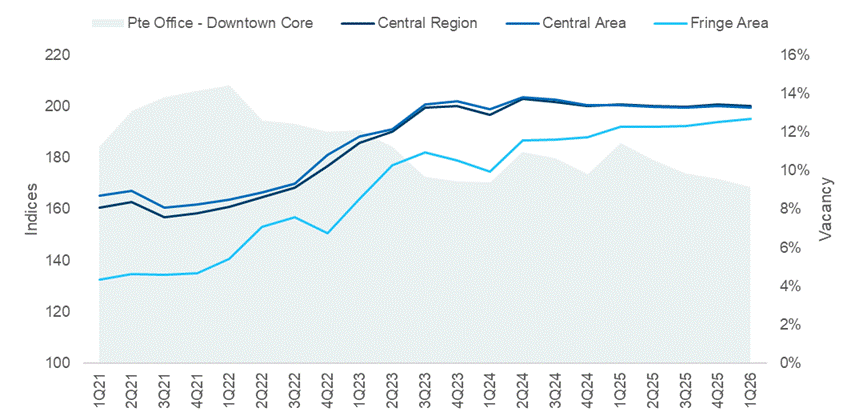

The latest quarterly statistics on the office market were also released by URA on April 24. The rental index of the Central Region increased 0.2% q-o-q, after five consecutive quarters of decline. This saw the median office rent increase to $2,230 psf in 1Q2026, from $2,169 psf in 4Q2026.

New office completions are expected to remain limited from now until 2027, with a larger pipeline of completions only anticipated from 2028 onwards.

“Amid the ongoing flight-to-quality trend, older Grade A buildings have seen backfill spaces emerge as tenants upgraded to newer, higher-specification buildings. However, these vacant spaces were quickly reabsorbed, reflecting the overall tightness of the market,” says June Chua, senior managing director and head of Singapore leasing at Newmark

News pieces like this explain what's happening in the market. Our consultations are designed to help you understand what it means for your own property decisions.

If you're considering buying, selling or upgrading, we'd be happy to help you work through your options.

Demand preferences turn to modern office spaces

Office vacancy for buildings in core business areas – the Downtown Core and Orchard Road planning area – tightened for the fourth consecutive quarter to 8.6% in 1Q2026. Office spaces in these two locations tend to be relatively modern and recently refurbished, with large floor plates and gross floor areas, and hence command the highest office rents.

On the other hand, the islandwide office vacancy (excluding the Downtown Core and Orchard Road) remained higher at 11.9% in 1Q2026.

The latest vacancy figures reflect sustained occupier preference for modern, and well-located Central Business District offices, that also offer strong connectivity, amenities, and workplace quality, says Wong Xian Yang, head of research, Singapore & Southeast Asia, at C&W.

He adds that this comes as more firms prioritise efficiency, talent attraction, and long-term resilience as they consider their corporate real estate needs in Singapore over the coming months.

According to analysis by CBRE, the flight-to-quality momentum was evident across key CBD developments, namely IOI Central Boulevard Towers, Marina One, and Marina Bay Financial Centre. These developments were the focal points of active leasing activity, with demand anchored by tenants seeking large, contiguous floor plates that match international specifications, says Tricia Song, head of research, Singapore and Southeast Asia, at CBRE.

New office supply tight until 2028

Likewise, leasing activity in the Central Region remained resilient, despite softer office rent growth there, falling 0.2% q-o-q in 1Q2026. This is attributed to the tight availability of office space, particularly prime and high-quality offices.

But this has not stopped corporate tenants, since the net demand for office space in the Central Region reached about 140,000 sq ft in the first quarter of this year. This is the fourth consecutive quarter of positive net absorption. The Downtown Core remained the primary demand driver in the Central Region, recording 118,000 sq ft of net office demand over the same period.

At the same time, new office supply in the Central Region remained limited, which led to office vacancy rates tightening to 10.5% in 1Q2026, while vacancy rates in the Downtown Core tightened for the fourth consecutive quarter to 9.3% in 1Q2026, a yearly decrease of 11.2%.

Overall, leasing demand was broad-based, but the financial services sector – which comprises commercial banking, wealth management, asset management, and quantitative trading – a key source of leasing activity.

Artificial Intelligence (AI) companies are increasingly graduating from coworking arrangements into dedicated, self-managed offices, says Song, adding that at the same time, coworking operators are expanding their footprint to serve a mix of start-ups and international occupiers.

Occupiers moving fast to secure early pre-committed leases

Ongoing geopolitical risks and inflation uncertainty may dampen occupier confidence over the coming months, and this could translate into some decision paralysis, says Wong of C&W, but he adds that Singapore’s office market also benefits from a strong underlying demand for high-quality space.

“Anecdotally, some upcoming Grade A developments completing in 2028 are already seeing healthy enquiry and pre-commitment interest,” says Wong. The consultancy predicts that CBD Grade A office rents could grow 4 – 7% in 2026, with demand supported by new completions in 2026 and 2027, as well as elevated development costs.

Shaw Tower, on Beach Road, will be the only major office completion this year and is unlikely to materially disrupt the current market equilibrium.

In general, the office market will remain largely favourable to landlords over the remaining nine months of this year, given the thin near-term supply pipeline and record low Grade A vacancy, says Song. “Large contiguous floor plates exceeding 20,000 sq ft are expected to remain scarce, with pre-commitment activity already registered for developments slated for completion as far out as 2029, underscoring the depth of forward-looking demand,” she says.

Meanwhile, given elevated relocation costs rising and limited relocation options, more occupiers may opt to stay put and renew existing leases until there is greater clarity on the macroeconomic outlook, says Chua of Newmark.

A single headline is rarely enough to change your plans. The value comes from understanding how today’s news fits into the broader direction of the market.

If you’d like to talk through what a shift like this means for your own timing, purchase, or exit, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

0 Comments