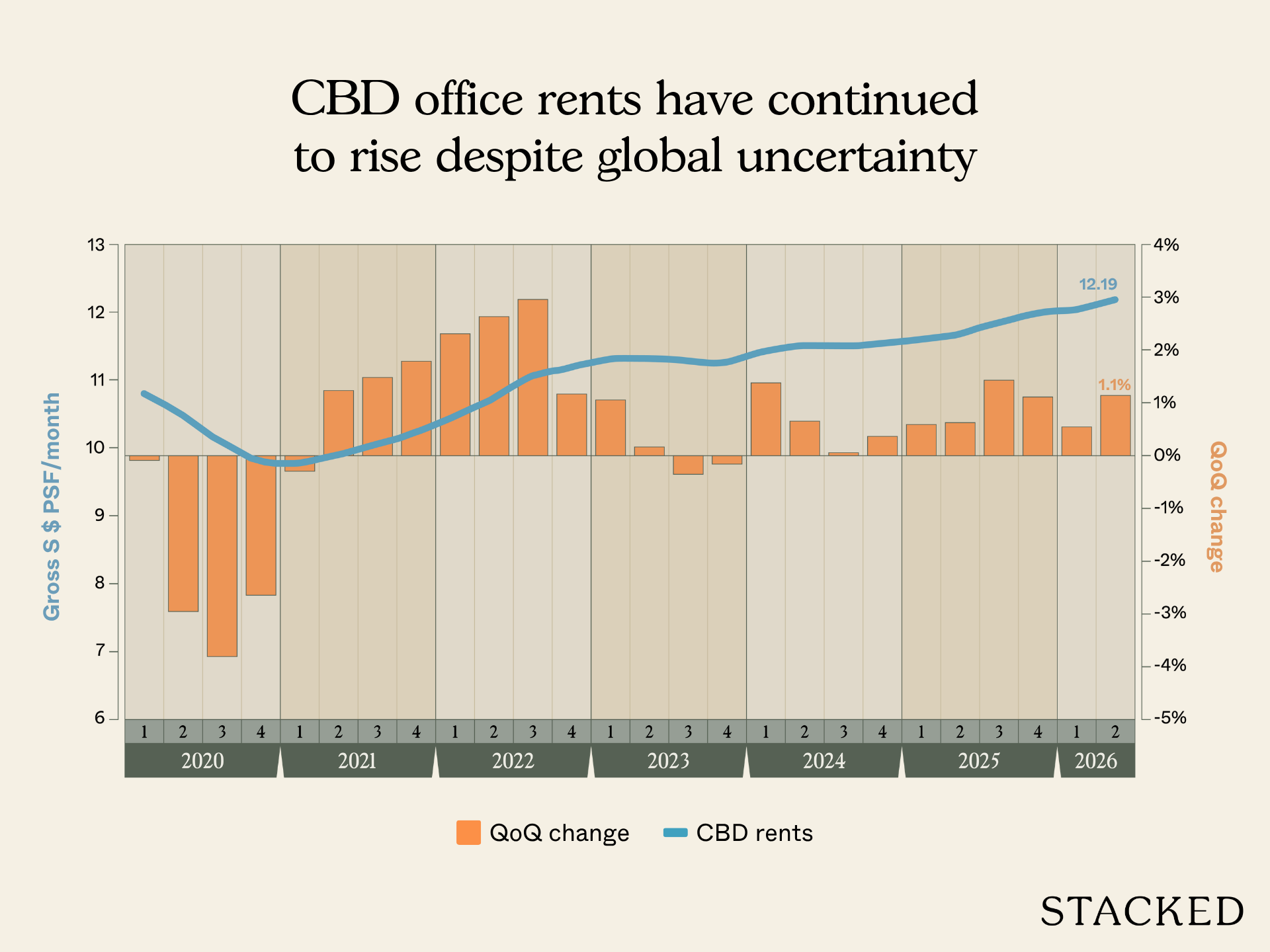

Global headwinds, geopolitical and economic uncertainty haven’t made a dent on Singapore’s prime office rents which are on track to record its sixth consecutive quarterly growth. According to data from CBRE, Grade A offices rents in the Central Business District (CBD) edged up 0.8% q-o-q to $12.50 psf per month (pm) in 2Q2026, up from $11.36 psf pm in 1Q2026.

This means that over the first six months of this year, Grade A office rents in the core CBD area have increased 1.6%, largely attributed to demand from corporate tenants and a flight-to-quality amidst tight supply in the core office market.

A separate market report by JLL also highlights that the vacancy rate of core Grade A offices in the CBD, excluding new supply, fell to 5.6% in 2Q2026 – the lowest level in nine quarters. JLL states that most Grade A office landlords have significant pricing power, leveraging Singapore’s structural advantage as a global and regional hub for corporate headquarters.

These ongoing factors should see the Grade A office market in the CBD pull off a full-year growth forecast of approximately 5% y-o-y, according to CBRE. On the other hand, JLL maintains a slightly moderate rental forecast of about 4%, with a cumulative five-year rental growth of around 15% projected through 2030.

The absence of any new major office completions in the CBD will likely lead to a long-term structural undersupply in the Grade A office market, which will underpin this rental cycle until the end of 2027, says Tricia Song, Head of Research, Singapore and Southeast Asia at CBRE Singapore.

“The market’s continued performance reflects a structural imbalance between occupier demand and available supply. Core CBD (Grade A) vacancy held firm at 3.3% – a record low – as the completion of Shaw Tower in the Fringe CBD marks the close of all meaningful new supply for 2026, with no further significant completions projected through 2027”, says Song.

Besides the lack of new supply, the withdrawal of Harbourfront Centre from the active office inventory in the market will further tighten islandwide supply. Grade A office vacancy rates look set to fall from 5.6% in 1Q2026 to 3.6% in 2Q2026.

Harbourfront Centre will close on July 27 after Mapletree Investments, the owner of the building, announced plans to redevelop the site into a new 33-storey mixed-use office and retail development. The new project is expected to be completed in 2031.

News pieces like this explain what's happening in the market. Our consultations are designed to help you understand what it means for your own property decisions.

If you're considering buying, selling or upgrading, we'd be happy to help you work through your options.

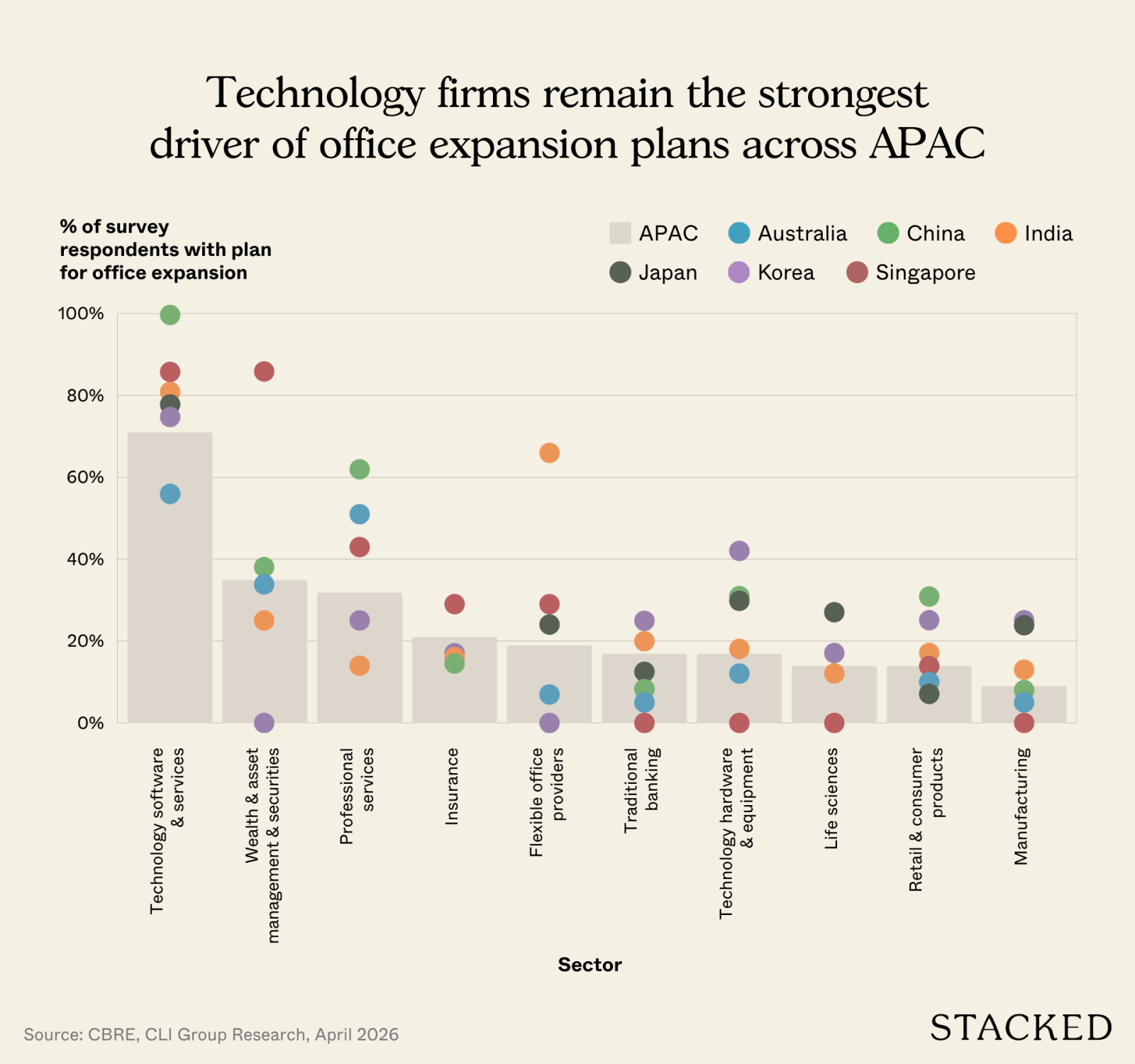

AI innovation is changing office use and corporate real estate needs

Taking a step back, both consultancies observe that office demand is increasingly being driven by AI innovation and shifts in the office needs by different industries. This trend has been observed among companies in the technology sector, financial services, and professional services industries.

As a result, a ‘K-shaped’ market is emerging, this describes the effect of an economic split between thriving and lagging industries.

The utilisation of AI in different industries does not equally affect their real estate needs. The office market, in particular, is most subjected to scenario-driven variability as demand is tightly linked to knowledge-worker employment and space intensity.

Another challenge brought on by AI and its impact on office demand is how it has increased heterogeneity in the type of offices required, meaning no two offices will be exactly the same.

In a research paper by Cushman & Wakefield, titled ‘AI Impact on CRE: The Next 10 Years’, the deployment of AI will accelerate office bifurcation, raising the premium and demand for high-quality, well-located spaces. This may see office design shift from supporting individual tasks, to one that supports accelerating decisions that require human context and shared commitment.

For occupiers with medium-term requirements, the window to secure quality space on favourable terms is narrowing. “While some tenant resistance to prevailing rents has been understandably observed, the fundamental market dynamic remains firmly in landlords’ favour,” says David McKellar, Head of Leasing at CBRE Singapore.

He adds that CBRE currently advises occupiers who have plans to increase their corporate real estate needs over the next two to three years to engage the market now, as conditions are not likely to ease.

Meanwhile, Chua Yang Liang, Head of Research and Advisory for JLL Southeast Asia, says the office market’s economic resilience, combined with Singapore’s reputation as a trusted, politically stable hub, continues to attract steady wealth inflows.

“Singapore’s office market is benefiting from a rare convergence of macro tailwinds. Following Singapore’s strong first-quarter performance, the government has maintained its 2026 GDP growth forecast at 2% to 4% despite ongoing geopolitical uncertainties in the Middle East,” says Chua.

Earlier, the Stacked editorial team reported that flight-to-quality momentum was the most evident across key CBD developments, namely IOI Central Boulevard Towers, Marina One, and Marina Bay Financial Centre.

Demand is driven by tenants seeking large, contiguous floor plates over 20,000 sq ft, which are scarce among Singapore’s Grade A offices and hence command a rental premium. The breadth of leasing demand is expected to continue to widen in the near term, with more AI and technology firms joining financial services and professional services as active movers.

One of them is OpenAI’s first Applied AI Lab outside the United States, a $300 million investment that will see more than 200 specialist AI professionals hired over the coming years.

Michael Glancy, Country CEO, Singapore & Southeast Asia at JLL, observes that the flight-to-quality narrative has evolved from a trend into a structural reality. He adds that leading organisations are treating their workplace as a competitive asset, and they are doing so before the availability diminishes. He cites Shell’s pre-commitment of approximately 100,000 sq ft at Asia Square Tower 1 and Databricks’ expansion at IOI Central Boulevard Towers as reflective of this shift.

“Tenants across various sectors, from AI and fintech to professional services and insurance, are committing to premium, well-located spaces ahead of need, recognising that the window to secure contiguous, large floor plates is closing fast,” says Glancy.

With tight supply in the office market, Marina Bay remains the main focus for corporate occupiers. Recent high-profile occupiers moving to the area include global data and AI company Databricks, which quadrupled its Singapore footprint to 32,000 sq ft. Other notable occupiers completing relocations include A&O Shearman, Franklin Templeton, and Virtu Financial.

Following the completion of IOI Central Boulevard Towers, the next major office completion is Shaw Tower, which is expected to receive its temporary occupation permit (TOP) approximately by the end of this month.

With Newport Tower the only non-strata new development to complete in 2027, new supply will not arrive until 2028, including The Skywaters, The Clifford, One Comcentre and Union Square Central.

What this means for Singapore’s office market

In 2Q2026, the depth and diversity of office demand stood out to industry observers, with growth not only from one or two dominant sectors.

“Financial services – spanning banking, wealth management, insurance, and asset management – remain active, but they are now joined by a meaningful cohort of AI businesses of all sizes, as well as professional services occupiers in decentralised locations. This breadth gives us greater confidence in the durability of the rental recovery,” says McKellar.

He cites the shift in office needs among AI-related firms, which were previously housed in co-working environments but are increasingly moving into core CBD spaces, as a hint of the direction that the AI industry in Singapore is evolving.

“Their graduation into permanent, dedicated office space this year signals a maturation of this cohort – signalling their commitment to Singapore for the medium to long term,” says McKellar. He adds that this maturity involves a desire for operational certainty, brand presence, and the ability to customise their corporate workspace.

Song concludes that with no new near-term supply arriving, even a moderate softening of external pressures – such as easing oil market volatility – could translate into a meaningful uplift in leasing confidence in the second half of 2026.

In this climate, landlords with a pragmatic approach to lease structuring and timing will be well-placed to capture this potential.

A single headline is rarely enough to change your plans. The value comes from understanding how today’s news fits into the broader direction of the market.

If you’d like to talk through what a shift like this means for your own timing, purchase, or exit, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

0 Comments