Adulting is never easy, especially when circumstances don’t give you much choice. Today’s story is a really special one as we’ll be touching on a Singaporean’s journey and the challenges she faced when she bought her first HDB flat at the age of 24 as a single.

You might have already come across Lisa’s story on her YouTube channel where she shared an in-depth and emotional experience of why her predicament at that point in time led to her having to buy an overvalued property and how she felt about the entire journey. Her narrative might not be a typical one, but it definitely stirs up thoughts in many.

We know the instinctive question that many would have is “I thought singles can only buy an HDB flat when they turn 35?”. While that’s generally true (although Mr. Pritam Singh did push for a lower age requirement in Parliament recently) there are some exceptions depending on the situation – Lisa’s being one.

Truly, there’s no home journey that is alike, and everyone will have a different experience depending on their stage in life. It takes a lot to share such a personal moment in life publicly (whether it is the good, the bad, or the ugly) and we hope that her story can inspire and help those who are facing any difficulty in acquiring a home.

The challenge for many buyers today isn't access to information.

It's interpreting that information in a way that makes sense for their finances, goals, and stage of life.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

Introducing Lisa’s Story from Lisa’s Adulting in Singapore

To really understand Lisa’s situation, let’s go back in time before the whole situation happened, just to frame the story a little better.

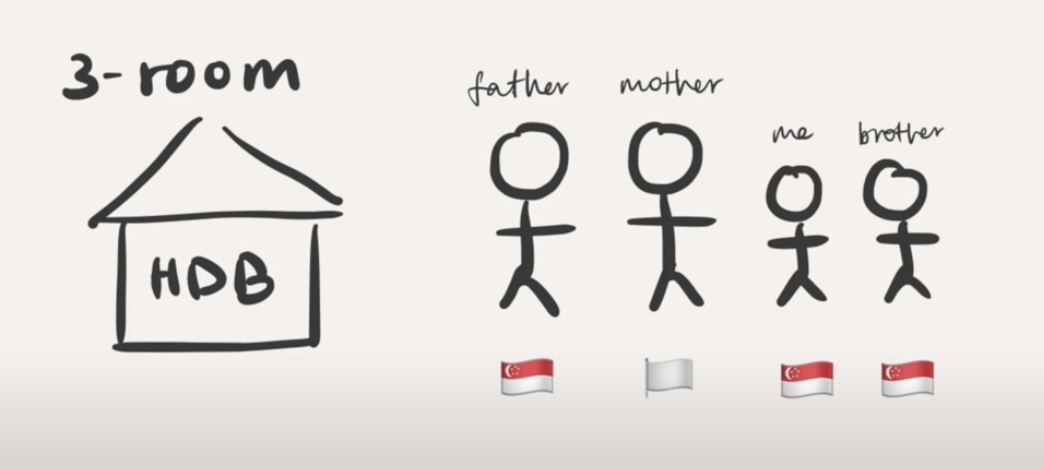

Just like many families in Singapore, Lisa grew up with her mom, dad, and younger brother in a Muslim family (her religion is very important in the later parts of her story) and they stayed in a 3-Room HDB flat.

This was typical in Singapore – younger children usually would share a room and the other would be occupied by the parents. What made Lisa’s situation a little different was that her mum was a non-Singaporean and this meant that the flat was only under her dad’s name.

Let’s pause here for a moment. Her mum’s citizenship was a really important detail in her story as this one simple detail meant that only one person (Lisa’s dad) was allowed to have legal ownership of the property. In the situation where the sole owner passes away, the house would have to be sold and that’ll compromise the sole shelter for the family. A typical Singaporean family would be better off with a Joint Tenancy, although some might prefer tenancy-in-common.

However, Lisa’s situation did not offer their family that luxury since her mother’s constant PR Application was often unsuccessful. Lesson learned here: Strategising the ownership of your real estate from the beginning will never do you wrong.

Okay, let’s jump back to the story.

When she was 12 years old, Lisa’s family had to, unfortunately, sell her childhood flat due to financial constraints. The family of four moved into her aunt’s place, which was also a 3-Room HDB flat. Her aunt stays alone, so she took up one room while Lisa’s family took up the other.

And that was their living arrangement for the next seven years. Over the course of that period, her dad offered to pay the remainder of Lisa’s aunt’s mortgage on that flat – and rightfully so. Both of them ended up sharing a joint tenancy on that unit.

Previously, we did mention that a typical family in Singapore would be better off to own the property under a Joint Tenancy agreement.

That means that usually the wife and husband would share the ownership of a unit and should one of them pass away, the other would inherit the other partner’s share and won’t need to sell away the property. And this makes sense because the remaining partner would have legal protection.

But in Lisa’s family’s case – it was a little bewildering that such an arrangement was decided between her dad and her aunt. This means that if her dad passed on, her aunt would inherit the full share of the property and have no obligation to take care of Lisa’s family.

And that was exactly what happened.

In 2019, Lisa’s father’s passing was a huge blow to her and her family.

Especially when she found out that none of her dad’s share of the house would be passed down to her underaged brother nor her. She had expected that at least some form of legal rights over their ‘home’ would be granted to them.

But no, her aunt was now the sole owner of the entire unit.

All her father had left was his remaining Central Provident Fund money (that was not nominated, mind you), plus the daily anxiety of her family being kicked out of their only refuge by her aunt, and deep mourning for her loss.

Although her aunt offered to sell her the unit she was living in at that time, Lisa couldn’t be sure. While the living situation started out okay, it started to become toxic during the circuit breaker period. But even up till then, it never quite crossed their minds that it wasn’t their home any longer as they have been living there for close to a decade (plus after all, her dad did pay for the house too).

Any reasonable person would assume that they would still continue to live there, but that was obviously not going to be the case any longer.

Her sole solution was to find her own place. And fast.

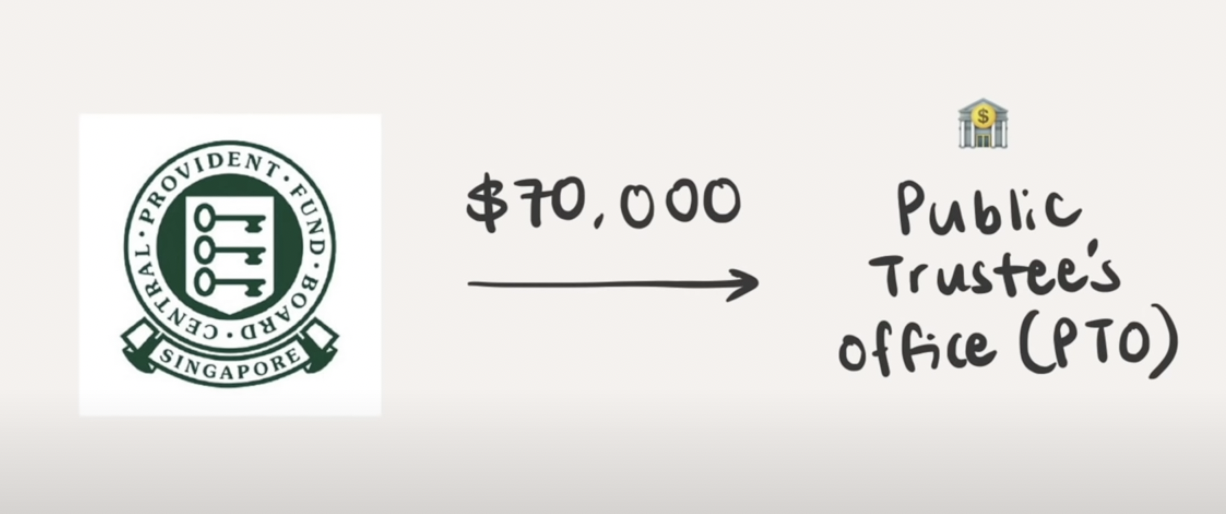

Her father did not leave a nomination for his CPF account before his untimely departure and naturally, CPF transferred all the amount in his retirement and Medisave accounts to the Public Trustee Office (PTO). (Lesson learned: make a CPF nomination, it’s really simple and seamless on CPF’s website).

In order for the surviving families to extract the money from the PTO, a few steps in order are necessary:

- Receive an Inheritance Certificate from the Court

- Produce this Inheritance Certificate to the PTO

- Provide Evidence of Relationship to PTO

- Receive disbursed funds.

There was an estimate of S$70K from those accounts which was vital for Lisa’s family. She had to write into PTO, requesting for the money to be disbursed back to her family. And this comes with the impact of her religion.

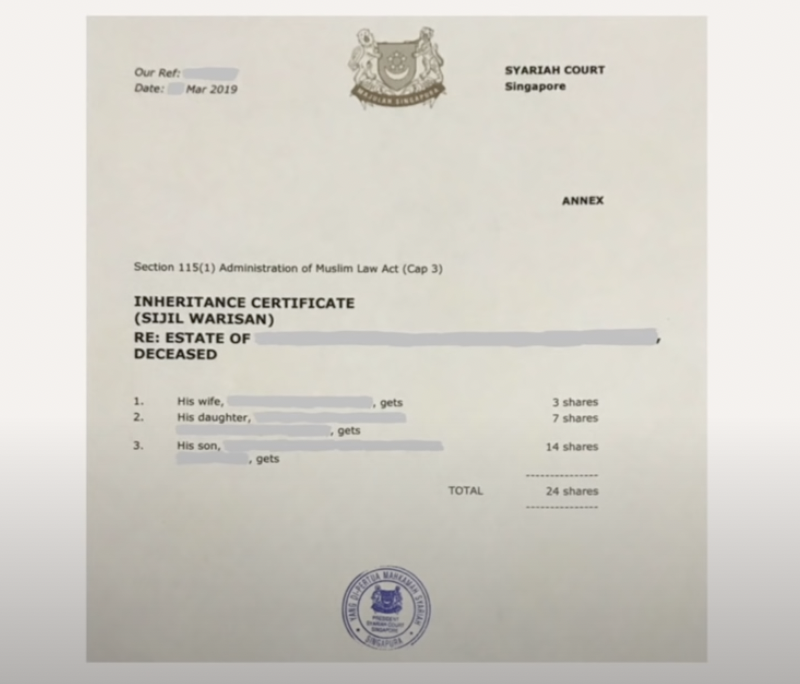

Remember that I mentioned that Lisa’s family is Muslim in the earlier parts of this piece? This information is really crucial here because this means that her dad’s proceeds are bound under the Sharia Law (instead of the Common Law).

Since there has been no assignment of his assets, the Sharia law decides on how the CPF monies were distributed. And it was distributed between herself, her mom, and her underaged brother. And the verdict was:

- Lisa’s Mother: 3 Shares

- Lisa: 7 Shares

- Lisa’s Younger Brother: 14 Shares

The amount was divided into 24 shares (that’s S$8,750 for her mum, S$20,417 for Lisa, and S$42K for her brother).

Using this official certificate, they visited the PTO branch and provided 3 different bank accounts to them, which they had to prove that the account was theirs. They also had to prove their relationship with their father (in the form of birth certificates and marriage certificates) before PTO can release any funds to the family.

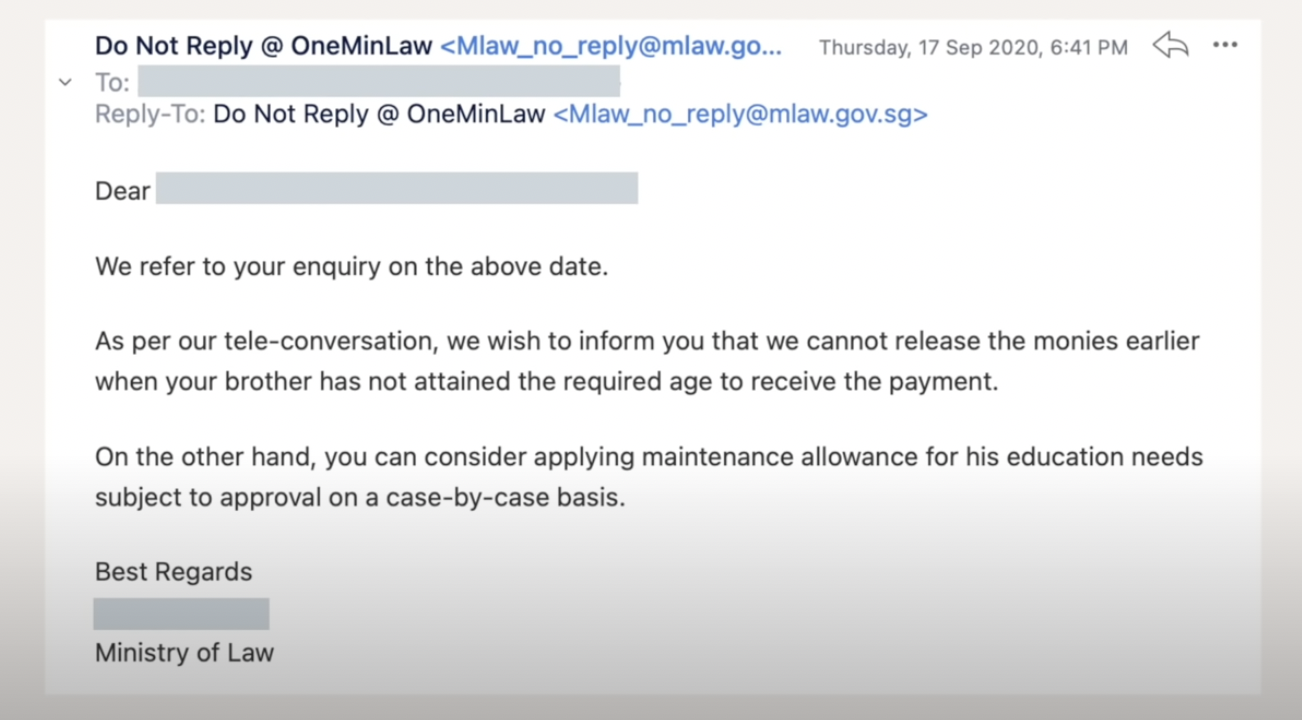

However, she faced yet another issue. She had expected to receive the full S$70K to comfortably put a shelter over her family’s head, but as there was no need for the funds then, she didn’t appeal at that time. It was only when she started house-hunting in 2020 that she wrote to appeal to PTO.

Unfortunately, the appeal was rejected yet again on the grounds that her brother wasn’t able to receive his share since he was below 21 at that point in time. His portion was held back and Lisa only received S$30K from her share and her mother’s share.

Her initial plan of using a part of her dad’s CPF money to put in the downpayment for the house and grow it through investments was shattered just from this one response.

Making The Hard Decision

Being the person responsible for settling all the paperwork and handling all the matters after her father’s passing, she dived deep into research mode.

There’s not much for her to choose from other than her four main options:

- They could rent an apartment for now,

- Buy over the current house from Aunt,

- Perhaps they could wait for a Build-To-Order Flat (BTO)?

- Or they can buy a resale HDB flat?

Option 1: Renting

This option was quickly turned down by Lisa herself as she felt that ultimately, renting was a waste of money and she would rather spend it on paying off her mortgage.

Option 2: Buying over her aunt’s home

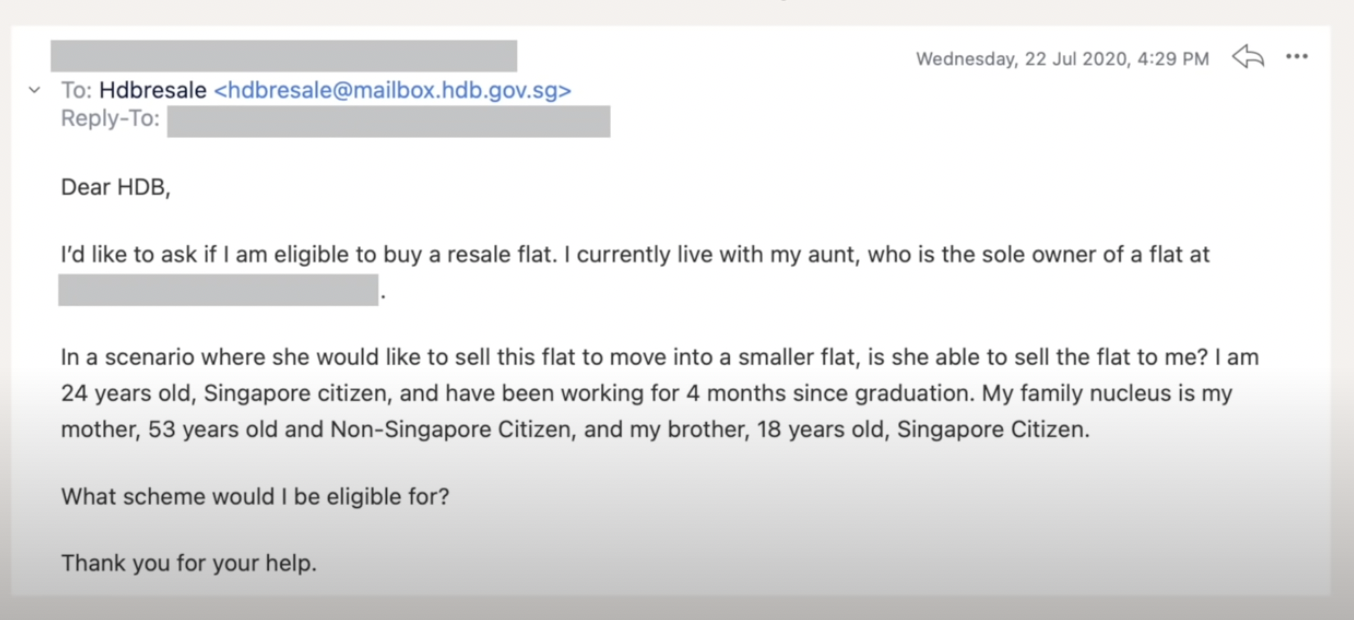

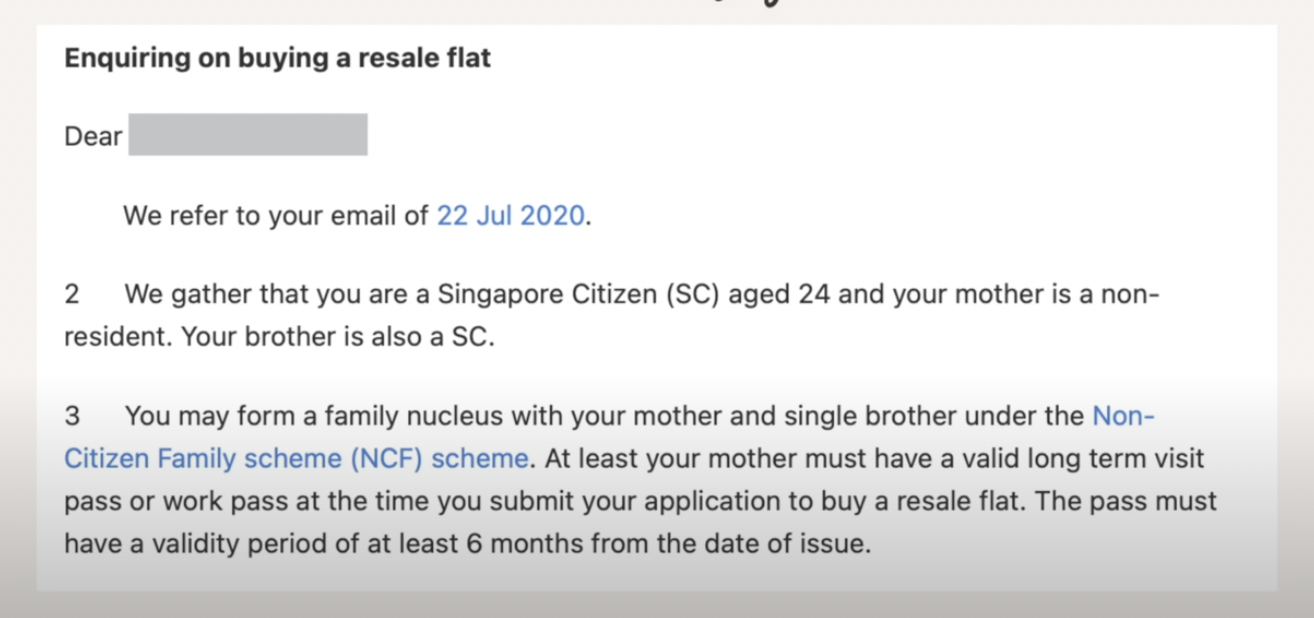

There was an initial discussion on Lisa’s family buying over her flat since her aunt has plans to downgrade into a smaller unit. Lisa immediately consulted with HDB on her eligibility to buy over at her aunt’s home.

The great news was that she could form a family nucleus with her mother and brother under the Non-Citizen Family (NCF) Scheme.

However, this offer quickly turned the other way due to her aunt’s change of heart. She wanted to keep the house for herself and made unjustified remarks about her decision to do so. Even when the topic was broached about her father’s share (as he had paid too), her reaction was that it was justified because he never shared in the utilities.

From then on, her aunt was slowly but surely chasing them out of her house – thus the brewing toxic environment. Staying at the house was definitely not a viable option and she’d have to look elsewhere. However, one important thing we learned here was that her family was eligible to purchase a resale HDB flat!

Option 3: Wait and buy over a BTO flat

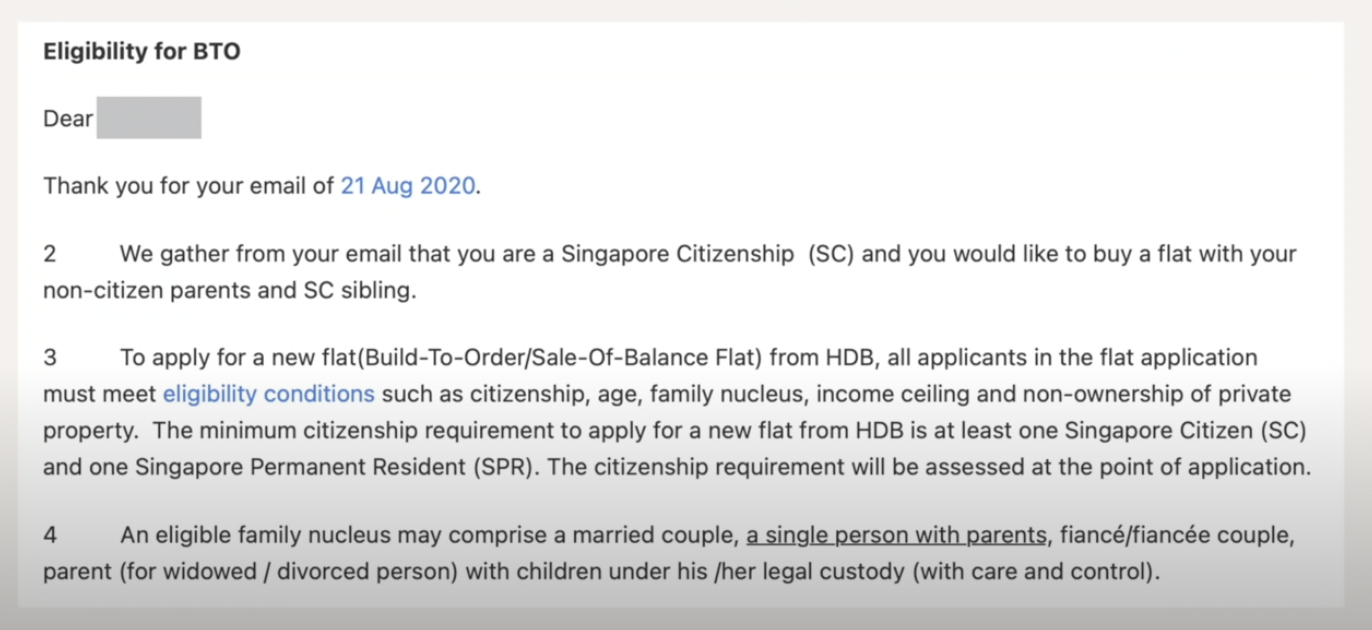

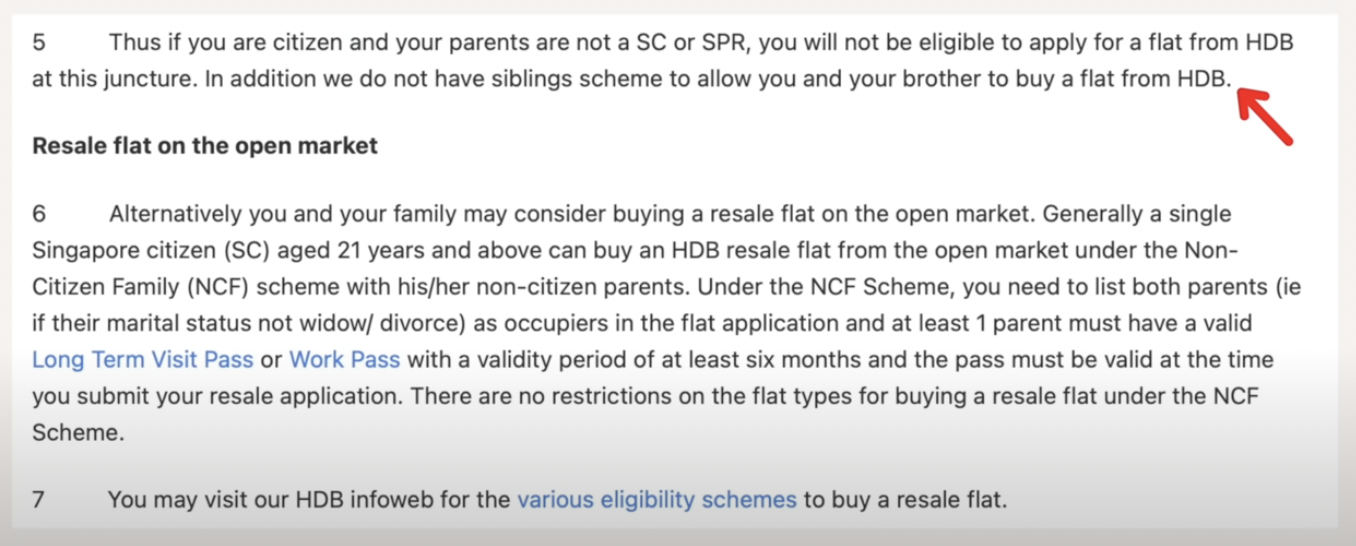

This was Lisa’s best option and she wanted to choose a BTO as it was the most affordable option. However, the minimum requirement to purchase a BTO flat was 1 Singaporean citizen and 1 Permanent Resident if the buyer is under the age of 35. And obviously, her family did not meet that requirement.

Lisa appealed to HDB regarding her situation but was faced with a firm no. Despite her brother being a Singaporean, HDB does not offer sibling schemes for Lisa and her brother to own an apartment together. This eventually led to her crossing this option out.

Lisa did point out that she felt that the BTO rejection was plainly unfair. It’s not that her mum did not want to become a PR, but rather her numerous applications were rejected. And just because of this, they were not granted affordable housing.

Option 4: Buy a Resale HDB

This was her last option – and the only route viable to her.

She learned from her previous experience of planning to take over her aunt’s unit that her family can form a family nucleus to buy over the flat (finally some good news).

As such, she came to the conclusion that she would use 100% of all her family funds to purchase their home. It’s a really tough decision but in the long run, it’ll definitely pay off.

Lisa’s Process and Experience

Once Lisa knew that she was going for a resale flat, she dived deep into research, looking for listings to help her with her shortlisting process.

On top of that, she decided to engage a property agent and they spoke for the first time on 3rd September 2020.

While we know that some may point out that she could’ve saved thousands if she just followed through with the process herself, frankly, a good agent is worth their weight in gold. Again, the keyword here is good.

Eventually, Lisa’s habit of always keeping track of her family’s finances which was especially important when it came to budgeting for her home.

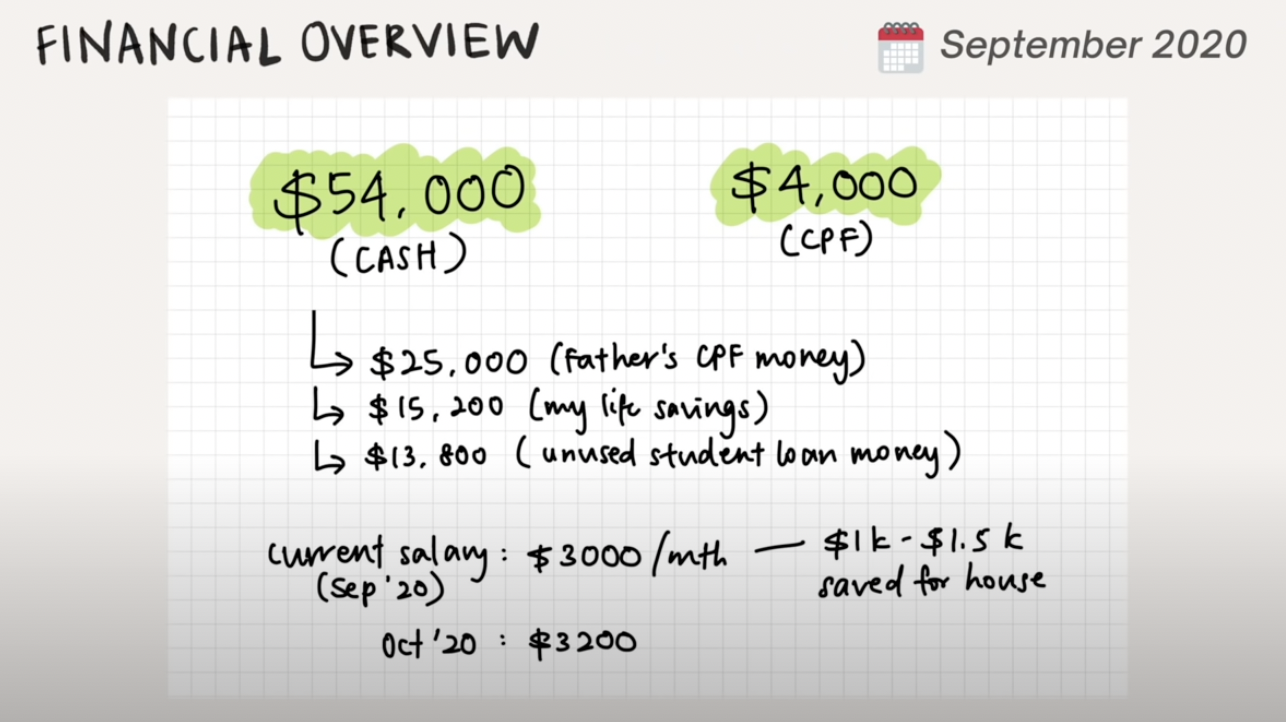

As of September 2020, this was her entire family’s financial overview.

Due to her brother’s bulk of the CPF funds that were not released, they had a total of S$58K from her father’s CPF distribution to her mum and her, her own personal CPF, and her life savings from working part-time, and her remaining unused student loan money.

If you’d do the math, a 10% downpayment is required for any resale HDBs in the form of CPF or cash (back during that time, it’s now 15%). And that includes all other fees and renovation costs payable – that really didn’t leave her with much wiggle room.

She really hoped to purchase a 3-room flat (in which she can share a room with her mum and her brother can use the other room), but a 2-room was what they could afford. The cheapest 3-room at that time ranged from S$300K to S$400K. This meant that she had to fork up S$102K upfront (a S$44K shortfall). She tried again to appeal to PTO’s release of her brother’s share but they were unwilling to budge.

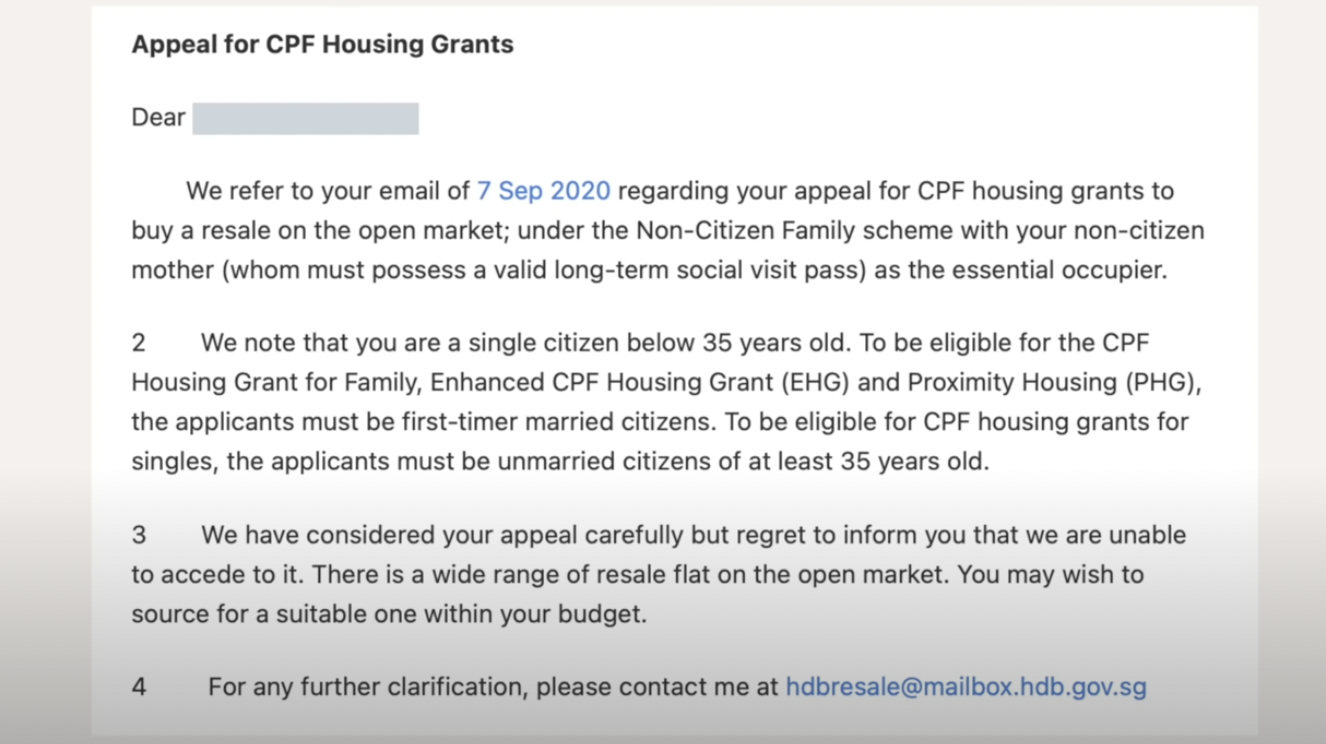

In the meantime, she appealed to HDB and her Member of Parliament (MP) via email for available grants that they could provide, such as the Singles Grant (up to S$25K), or the Proximity Housing Grant (up to $15K) or the enhanced CPF Housing Grant (up to $40K), but all to no avail due to how strict HDB were with their requirements. And there were no replies from her MP.

And so after trying all known available options, she knew that settling for a 2-room was the best she could do.

Although taking a bank loan did cross her mind, she refused to fall deeper and deeper into debt and settled with what she could afford (for now). Even so, that was the moment that she felt the most financially insecure.

And for good reason why.

Thankfully by September 2020, her brother was already serving NS and had already moved into another relative’s spare bedroom. As such, the demand for space wasn’t as bad as when the three of them had to live together.

She soldiered on and went for several house viewings across Singapore.

On the 3rd of October 2020, she went for a viewing and realised that she had found ‘the one. It ticked off all of her requirements at that point in time and she immediately requested for her agent to engage in a bidding war.

Her requirements were pretty simple actually, she just needed the unit to be:

- Within her budget

- No long waiting time between exercising OTP and submitting a resale application

- In a liveable condition

Fun fact, she found her home exactly 1 month after meeting her agent on the 3rd of September 2020.

Her final purchase price of the 2-room unit was S$256K, and she agreed to it despite knowing that it was overvalued.

For those who are interested in knowing the step-by-step HDB process outline, do check out Lisa’s recount on YouTube.

She paid a total of $63,500 for the downpayment, legal fees, agent fees, and other miscellaneous fees.

Final Thoughts

Despite having to grow up due to her circumstances, Lisa did a wonderful job at navigating adulthood just to put a roof over her family’s head. She reflected that compromise was the biggest lesson she’s learned, but there are so many other takeaways that we can learn from and be inspired by her journey.

Lisa shared her vulnerability and in return, we gained knowledge of her entire experience of owning a property at 24. What was your biggest lesson learned just from reading this? Do share in the comment section below.

Thank you, Lisa, for sharing your inspiring journey with the world.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

1 Comments

Thank you, Lisa, for sharing a very difficult and stressful part of your life. And you have emerged a champion, well done!

“Prosperity tries the Fortunate, adversity the great” (Rose Kennedy)

“The flower that blooms in adversity is the rarest and most beautiful of all.” (Walt Disney)

“Resilience is our ability to bounce back from life’s challenges and unforeseen difficulties, providing mental protection from emotional and mental disorders.” [Michael Rutter (1985)]