Against an uncertain geopolitical climate, rental growth for prime retail properties in Singapore is expected to remain measured in 2026, despite growth in international visitor arrivals.

According to a 1Q2026 Retail Market report by Knight Frank Singapore, there were 12.9 million international visitor arrivals that resulted in a corresponding $23.9 billion in tourism receipts from January to September 2025.

For the entire 2025, the consultancy expects that visitor spending will exceed the $29.8 billion that was recorded in 2024.

In 1Q2026, Singapore welcomed 4.4 million international tourists, which is a 9.8% q-o-q increase compared to the incoming arrivals in 4Q2025, and is 2.8% y-o-y higher compared to the visitor arrivals in 1Q2025.

As Singapore strengthens its position as a regional entertainment and events hub, the positive impact on tourist numbers is likely to continue, which in turn impacts on prime retail sales and rental.

Despite cost pressures from geopolitical shocks, Singapore’s prime retail properties can retain their competitive edge if landlords and retailers are able to work together to protect occupancy rates and capture diverted demand, says Galven Tan, CEO of Knight Frank Singapore.

Market commentary like this is only useful if you can translate it into what it means for your own purchase: your entry price, holding period and exit options.

That's where many buyers get stuck. General market insights rarely tell you whether a specific unit, at a specific price, is the right decision for your circumstances.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

Spike in visitor arrivals support retail spend

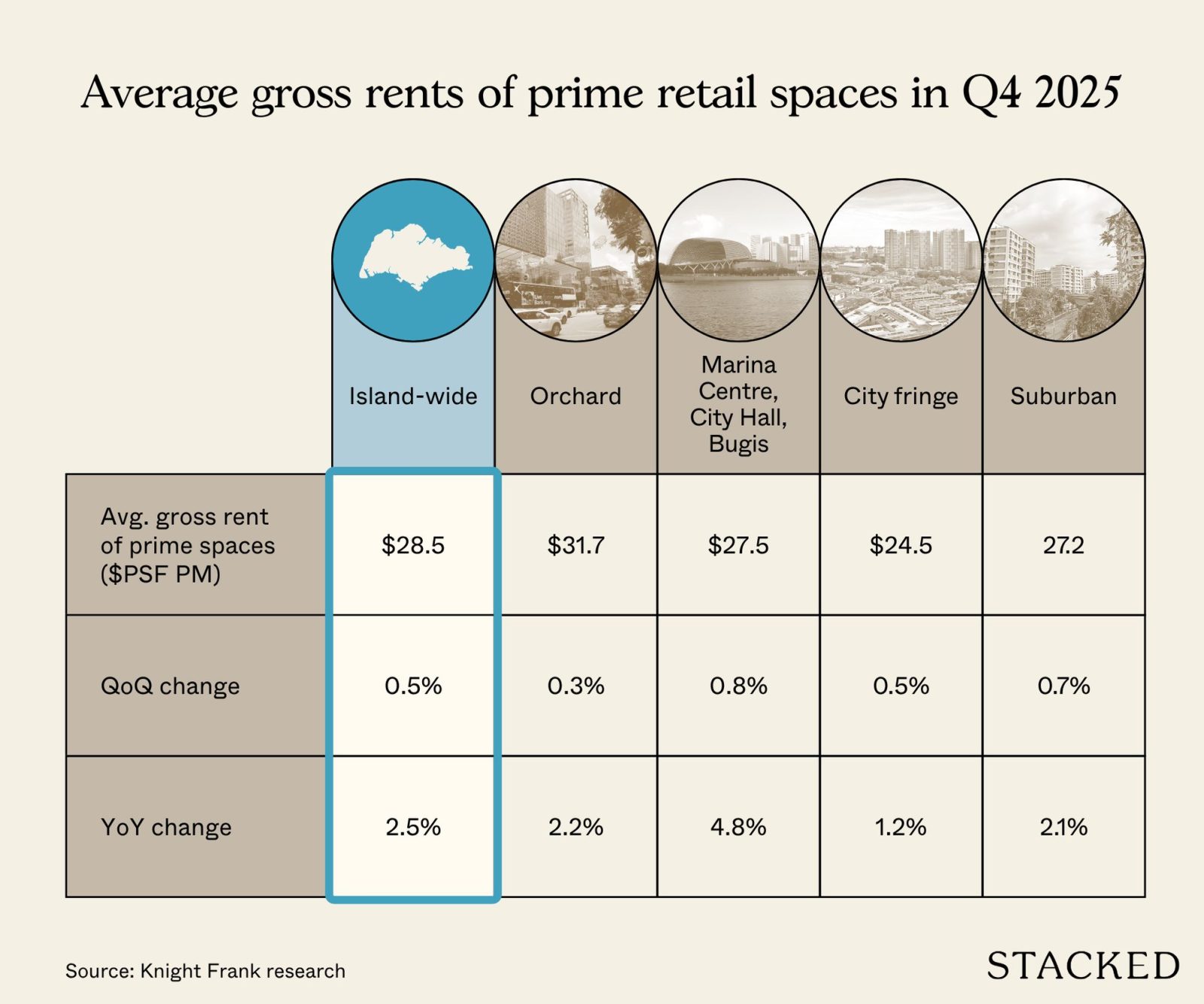

In 4Q2025, the island-wide average gross rent of prime retail spaces increased slightly by 0.5% q-o-q to $28.50 psf per month (pm). On a yearly basis, rents rose 2.5% compared to the 3.0% growth recorded in 4Q2024.

Amid the limited pipeline supply of new prime retail space in 2026, Knight Frank projects prime retail rents to grow by 2 – 4% this year.

Homing in on specific micro-markets, the Marina Bay-City Hall-Bugis cluster posted the strongest rental growth – climbing 0.8% q-o-q in 4Q2025 and clocking in at a 4.8% y-o-y increase.

This was driven partly by the Singapore Grand Prix which took place in October 2025. Due to the spike in affluent leisure and business travellers to this area, spurred by the increase in Meetings, Incentives, Conventions, and Exhibitions (MICE) events, prime rents in this micro-market grew 4.8% y-o-y in 4Q2025.

While Orchard remains the highest in terms of average retail gross rent at $31.70 psf pm, the prime shopping belt only recorded a y-o-y increase of 2.2%. On the other hand, suburban areas reported a 2.1% y-o-y increase, while retail rents in city fringe areas saw a 1.2% y-o-y uptick.

While the retail sector remains on a growth trajectory, high operating costs and intensifying competition have contributed to several high-profile closures in 2025.

Singapore is an aspirational launchpad for retailers’ regional expansion

Total retail sales rose slightly in October and November 2025 to reach $7.6 billion, up from $7.3 billion in July and August 2025.

From August to November 2025, sales of recreational goods have been leading growth in the retail sales index, expanding by 14.6%. It is followed by cosmetics, toiletries and medical goods.

Excluding motor vehicles, retail sales for January and February 2026 saw a slight dip at $7.5 billion, compared to $7.7 billion in October and November 2025.

Data from the Department of Statistics Singapore shows that demand for retail and food & beverage (F&B) rental remains high. The number of retail outlets grew by 3.7% y-o-y to 37,154 while the number of F&B establishments increased 5.3% y-o-y to 19,600 in 2025.

In the retail scene, the dominant players are Chinese F&B brands, which saw a rapid rollout of major mass-market chains in recent years.

In a more strategic move, operators are now recalibrating their strategies to tighten competitiveness and cater to discerning consumers by moving to higher traffic locations or refurbishing existing outlets and introducing more premium options for broader appeal.

The Knight Frank report also cited growing interest from Japanese, Korean and American F&B operators looking to establish or expand their presence in the SEA market.

However, high manpower and operational costs here typically mean that such market entry moves are constrained to larger and better capitalised chains with the resources to support long-term growth.

As the conflict in the Middle East unfolds, the near-term implications for the retail sector would likely result in delays or reassessments of new store rollouts, signalling longer leasing decision cycles despite stable underlying demand for now.

Innovative concepts and social commerce setting off new trends

Despite the cautionary stance, opportunities remain viable, especially when businesses are willing to take on an innovative approach, based on the conclusion in Knight Frank’s report.

An example would be Chinese wellness brand House+ Bubble, which opened a 50,000 sq ft 24-hour spa at Perennial Business City in March.

The juxtaposition of lifestyle retail in a primarily commercial or industrial setting lends itself to the unconventional approach taken by the business operator, which could potentially maximise upside.

Another point to note is the accelerated shift towards social commerce, supported by the Singapore Retailers Association, TikTok Shop and Workforce Singapore to build livestreaming capabilities and consumer reach.

Backed partially by SkillsFuture funding, the programme combines institutional support for social commerce as a structural growth channel. The aim is to help retailers to operationalise digital platforms to deepen customer interaction through immersive, content-led experiences and drive higher conversion.

Luxury, beauty and wellness – the frontrunners driving retail demand

As tourist spending and high-net-worth local consumption recovers, luxury segments such as watches, jewellery and designer labels are poised to remain among the more resilient segments of the retail market.

This translates to demand for premium-format stores along Orchard Road and Marina Bay, which is also drawing keen leasing interest from fitness, health and beauty services, personal care operators and omnichannel showrooms that integrate retail with experiential elements.

Beauty, wellness, fitness and enrichment are other experiential and service-led categories that are expected to thrive in the ongoing competitive retail climate.

On the other hand, mounting pressure may extend towards mid-market fashion, large-format department stores, and low-margin mass-market retailers, who need to find a strong differentiator.

Occupancy in well-managed malls is expected to remain firm, with F&B operators expected to make up new leasing demand particularly in prime and well-performing suburban malls.

Nevertheless, factors that are likely to cap any rental upside this year include rising operating costs for labour, utilities and import expenses, which would affect tenants’ ability to absorb rental hikes. Another factor which presents additional risks is intensifying competition and pockets of oversupply, particularly within certain F&B sub-segments.

Commentary like this is useful for understanding the broader market. The harder part is applying those ideas to a specific property, budget or decision you’re actually considering.

That’s often where a second opinion becomes valuable.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

0 Comments