The news of cooling measures in December 2021 came as a relief to many, but January’s numbers have thrown a wet towel over some homeowners’ hopes. Resale flat prices seem to be higher despite the cooling measures, and it begs the question: if cooling measures don’t calm the market, what will?

Table Of Contents

- Resale flat prices continued to climb in January 2022

- 1. Cooling measures may drive condo buyers to seek resale flats instead

- 2. Loan curbs on HDB properties are still insignificant

- 3. Demand comes from a demographic that can’t buy BTO flats

- 4. Combination of high rent, with a demand for immediate housing

News pieces like this explain what's happening in the market. Our consultations are designed to help you understand what it means for your own property decisions.

If you're considering buying, selling or upgrading, we'd be happy to help you work through your options.

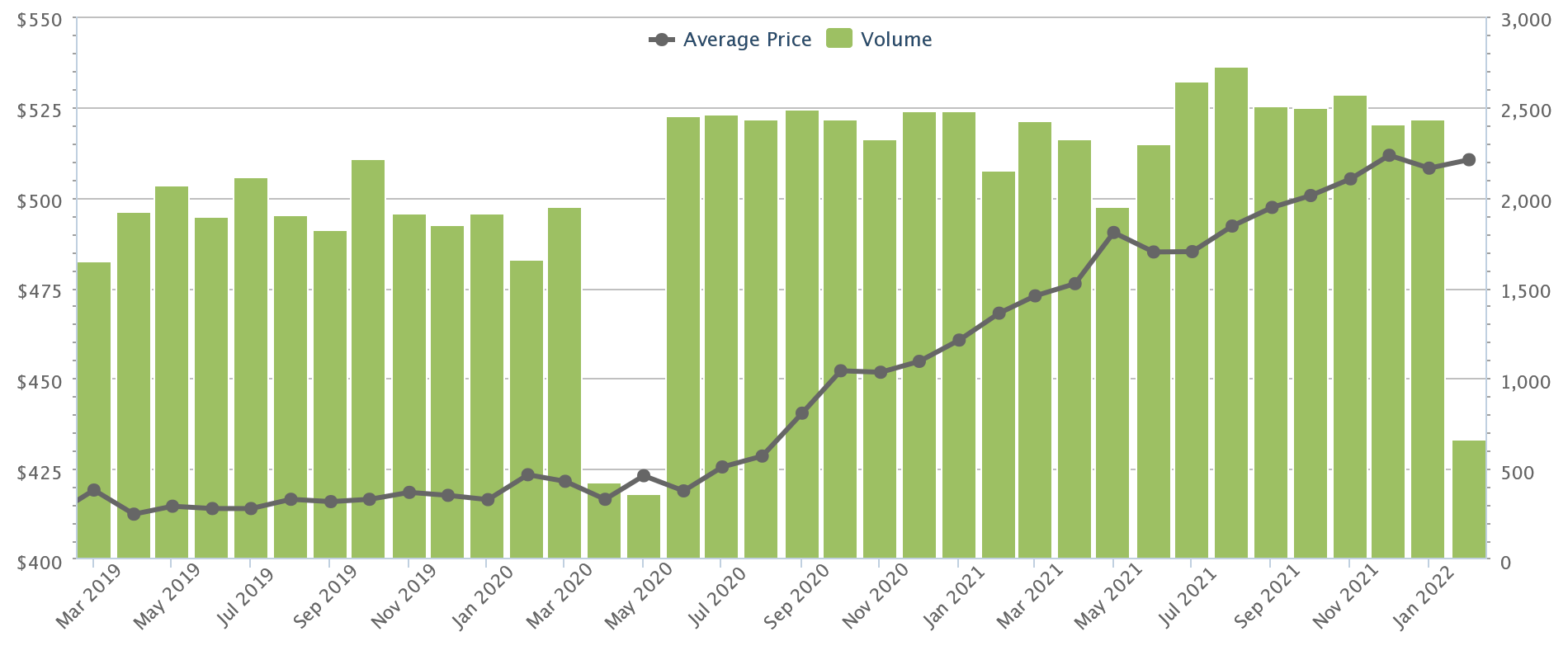

Resale flat prices continued to climb in January 2022

Flash estimates show HDB prices climbed by just over one per cent for January, up from 0.8 per cent in December, when new cooling measures were passed. This ran contrary to many expectations (even ours), which was that the market would switch to a “wait-and-see” mode, as a knee-jerk reaction to cooling measures.

Resale transactions also rose along with the price, from 2,428 units last month, to about 2,442 units in January. The only point of relief for buyers is that the volume is lower than the same time last year, when there were 2,432 transactions (it’s frankly not by much).

The number of million-dollar flats also dropped significantly for the month; from 38 transactions in December, to 27 in January; but million-dollar flats remain outliers, which doesn’t usually reflect well on the wider HDB resale market.

Overall, average resale flat prices have now been climbing non-stop since around July 2019; and they now appear to be defying cooling measures as well.

What’s happening, and is there hope for homebuyers?

Some opinions from realtors on the ground:

- Cooling measures may drive condo buyers to seek resale flats instead

- Loan curbs on HDB properties are still insignificant

- Demand comes from a demographic that can’t buy BTO flats

- Combination of high rent, with a demand for immediate housing

1. Cooling measures may drive condo buyers to seek resale flats instead

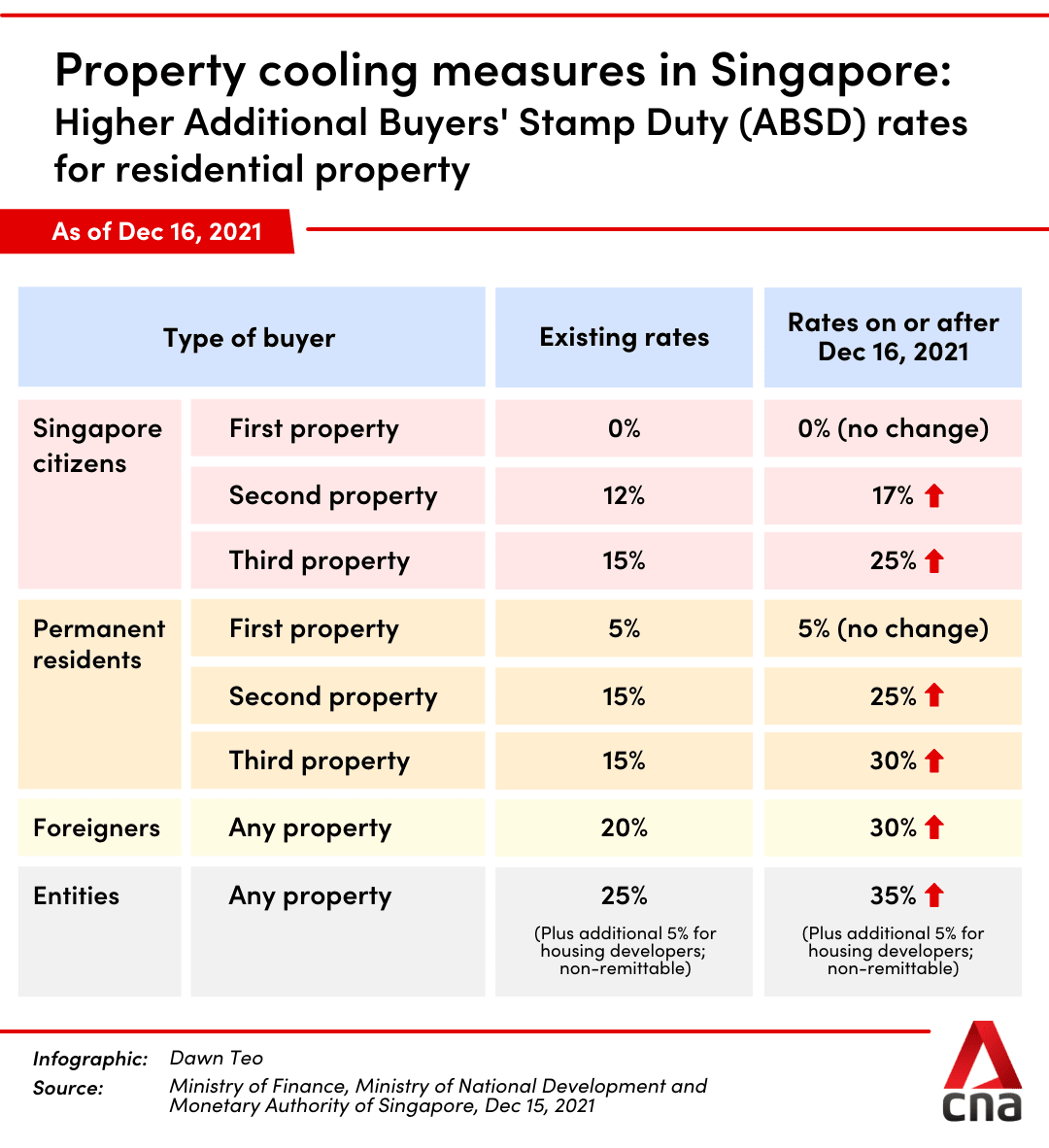

Some realtors opined that the cooling measures are targeted more at private properties than HDB flats. For example, a lower TDSR limit (see below) and a higher ABSD are only significant to condo buyers.

Consider that, for someone to upgrade from their flat to a condo, they could have to pay 17 per cent of the condo price as ABSD* (around $255,000 for the typical $1.5 million condo). While they can apply for ABSD remission later, it’s still a high upfront cost, with the added stress of ensuring the flat is sold within six months.

But if you upgrade from a flat to a larger flat, however, or upgrade to an Executive Condominium (EC), you’re spared the ABSD. And along with the already-high condo prices in 2022, this may cause some upgraders to eye larger flats instead of switching to private property.

As these upgraders are already saving a tremendous sum by not going private, many are unfazed by Cash Over Valuation (COV), or rising resale prices. As one realtor pointed out, anyone prepared to pay five per cent of a condo in cash (often about $75,000) is more than prepared to pay COV of $30,000 or even $50,000.

As private property prices keep climbing, and upgrading to them becomes more complicated, a portion of the demand could filter into the resale flat market instead.

*This is assuming they buy the new property before selling their flat. However, there are challenges with interim housing, if you sell your home before purchasing a new one.

2. Loan curbs on HDB properties are still insignificant

Some realtors expressed that the loan curb on HDB flats is too minuscule to be felt; a point that we’ve agreed with in some earlier articles.

The maximum loan amount for an HDB property, via an HDB Concessionary Loan, is now 85 per cent of the price or value (whichever is lower). This is down from 90 per cent previously.

The minimum down payment on a $500,000 flat, using an HDB loan, would now be $75,000, payable with cash or CPF. However, most Singaporean couples in their 30’s (the typical age of many home buyers) have over $100,000 in their combined CPF; in fact, common for many Singaporeans to pay more than 15 per cent down anyway*.

Bank loans are completely unaffected, as banks continue to provide up to 75 per cent financing for flats.

The Total Debt Servicing Ratio (TDSR) for bank loans has been tightened by five per cent, and this places higher income requirements on home buyers. However, HDB properties – which already have a Mortgage Servicing Ratio (MSR) of 30 per cent – are unaffected by TDSR changes.

In short, loan curbs from the cooling measures do little or nothing to cool resale flat prices at this point in time.

*You don’t really have a choice, as you’re only allowed to retain up to $20,000 in your CPF OA when you purchase the property.

3. Demand comes from a demographic that can’t buy BTO flats

One realtor pointed out that some homebuyers cannot afford private properties, but at the same time cannot qualify for BTO flats:

“If husband and wife are both Permanent Residents (PRs), then they cannot buy a BTO flat. If a couple is unmarried, they can only buy two-room if they buy BTO, it may not be big enough for their family. If they are downgrading from private property, they won’t want to wait more than two years* before they can apply for BTO.

In all these situations, the buyers have no choice but to fight for resale flats.”

The realtor noted that, among those “downgrading” from private properties, there are many who are not retirees: this group includes young couples looking to start families, who have found their one or two-bedder condos to be too restrictive.

Regardless of the number of BTO launches, it’s not possible to bleed off demand from this particular group. Bear in mind that those who are downgrading from private properties will enter the resale markets flush with cash, making it tough for first-time homebuyers to compete.

*You have to wait 30 months after disposing of a private property before you can ballot for a BTO flat. This more or less necessitates resale, as you still need to wait four to five years for construction after those 30 months.

4. Combination of high rent, with a demand for immediate housing

While there will be more BTO launches in the next two years, this is an abstraction to those who find it difficult to Work From Home in a flat with parents, siblings coming home from school, etc.

At the same time, we’re in a period where rental rates are a six-month high; and they look set to increase.

So at this point, we can see why the cooling measures have all the strength of a snowball in a microwave when it comes to the resale flat market. There are large groups of Singaporeans who need immediate housing but can’t afford resale condos either. As such, the surging demand for resale flats continues unabated.

There is also the consideration that given the mild nature of the cooling measures on this end of the market, we might only see the effects of it further down the road. With other headwinds that may come into play such as a record number of HDB flats reaching MOP in 2022 (31,325 units), a higher number of BTO flats that will be released, and the easing of construction delays as Covid-19 hopefully subsides. All these may contribute to a general easing of the growth of prices and demand.

Perhaps at this stage, if you’re a first-time homebuyer, you should realistically be looking in non-mature areas with some future growth potential. While you may take a bit longer to realise gains, further out areas like Sengkang or Yishun still offer reasonable amenities, at prices that are (not yet) off-the-charts.

And unless you’re going to live out the rest of your life there, buying a very old flat for a million dollars is still not the best path for most, however “normal” that’s starting to look.

Drop us a note at Stacked, and we can find experts in your specific neighbourhood; there may be outliers that remain affordable. In the meantime, follow us on Stacked Homes as we monitor the situation, and for reviews on new and resale condos alike.

A single headline is rarely enough to change your plans. The value comes from understanding how today’s news fits into the broader direction of the market.

If you’d like to talk through what a shift like this means for your own timing, purchase, or exit, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

1 Comments

Not enough new HDB is the main problem