Dear Stacked,

My husband and I are both in our 50s and we currently own two condos – one for our own stay and the other is rented out. We plan to sell both units in about five years’ time.

Although the mortgages won’t be fully paid off by then, based on our estimation, we should have sufficient net proceeds to accomplish the following:

1. Down-payments to help start our two children on their property journey

2. Fully purchase an HDB executive maisonette (EM) so that our family (parents, 2 kids, grandma, and helper) can continue to stay together.

3. Renovate the EM to rent out the upper floor once the kids move out permanently.

We reckon that EMs should have around 60 years left on their lease by the time we go about this purchase. This is not a concern for us since it will be more than enough to house us for our remaining years.

We are also less bothered about the impact of lease decay and the declining value. We are more concerned about how our children might sell the EM after we pass, so it won’t be a liability, since they will have their own homes. What options are there to get rid of the EM if there’s no longer any resale value?

(This is part of an ongoing series where we answer reader questions about the property market. If you have one of your own, send it to stories@stackedhomes.com.)

Hi and thanks for writing in!

Before we dive into this, here’s a quick reference for our readers who may not be familiar with executive maisonettes (EMs).

Broadly speaking, EMs are a discontinued type of public housing by HDB, and are typically two-storey flats connected by an internal staircase. Most of these flats span from about 1,500 – 1,600 sq ft, and the layout tends to work well for larger, multi-generational households.

From what you’ve shared, it seems like you’ve thoroughly considered the living arrangement carefully, and are upfront and clear about where your priorities lie.

In general, the negative impact of lease decay and the potential loss of value of the flat as it ages are not your main concern. What matters is that the property works for your family during the years you need it, and that it does not become a liability that your children have to untangle after you pass.

These are the right questions to ask yourself, and it is worth addressing head-on.

The concern is not whether the EM will have any resale value when the time comes to sell it, but what your children will actually be up against when they need to dispose of the property. In addition, what are the conditions at that point that make the process manageable or unnecessarily difficult.

Reader questions like the one above rarely have a clear-cut answer. The "right" move depends on your finances, timeline, long-term goals, and how much downside you're prepared to accept if things don't go to plan.

That's the hardest part of any property decision, not finding information, but understanding what it means for your situation before committing.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

The inheritance problem your children may not expect

The first challenge to address is the one that arises before your children even get to the question of selling.

You have mentioned that part of your plan is to help both of them onto the property ladder. If they own private residential property at the time they inherit the EM, they do not have a free hand in deciding what to do with it, based on prevailing regulations.

Under HDB’s current rules, a private property owner who inherits an HDB flat whose minimum occupation period (MOP) has been met can retain it without first disposing of their private property. However, the condition attached to that is occupancy: the inheriting owner must live in the inherited HDB flat, and not the private property.

For children who already own homes and have their own households, that occupancy condition is not workable in practice. Moving into the inherited EM would mean giving up their private property arrangement, which is unlikely to be a realistic option if they have families of their own by then.

From where we stand today, and looking at the housing regulations, their most realistic choice upon inheriting the EM is to sell it. That is not necessarily a problem, but it means the sale is not optional.

It is a transaction they will need to complete, under whatever market conditions exist at the time, and potentially within a timeframe set by HDB, depending on how the rules apply to their situation. How manageable that sale turns out to be depends on decisions your family can start making now.

Do note that HDB policies may change between now and the time your children inherit the property, so it would be worth verifying the current rules with HDB directly when the time comes.

Who can actually buy the property when they need to sell

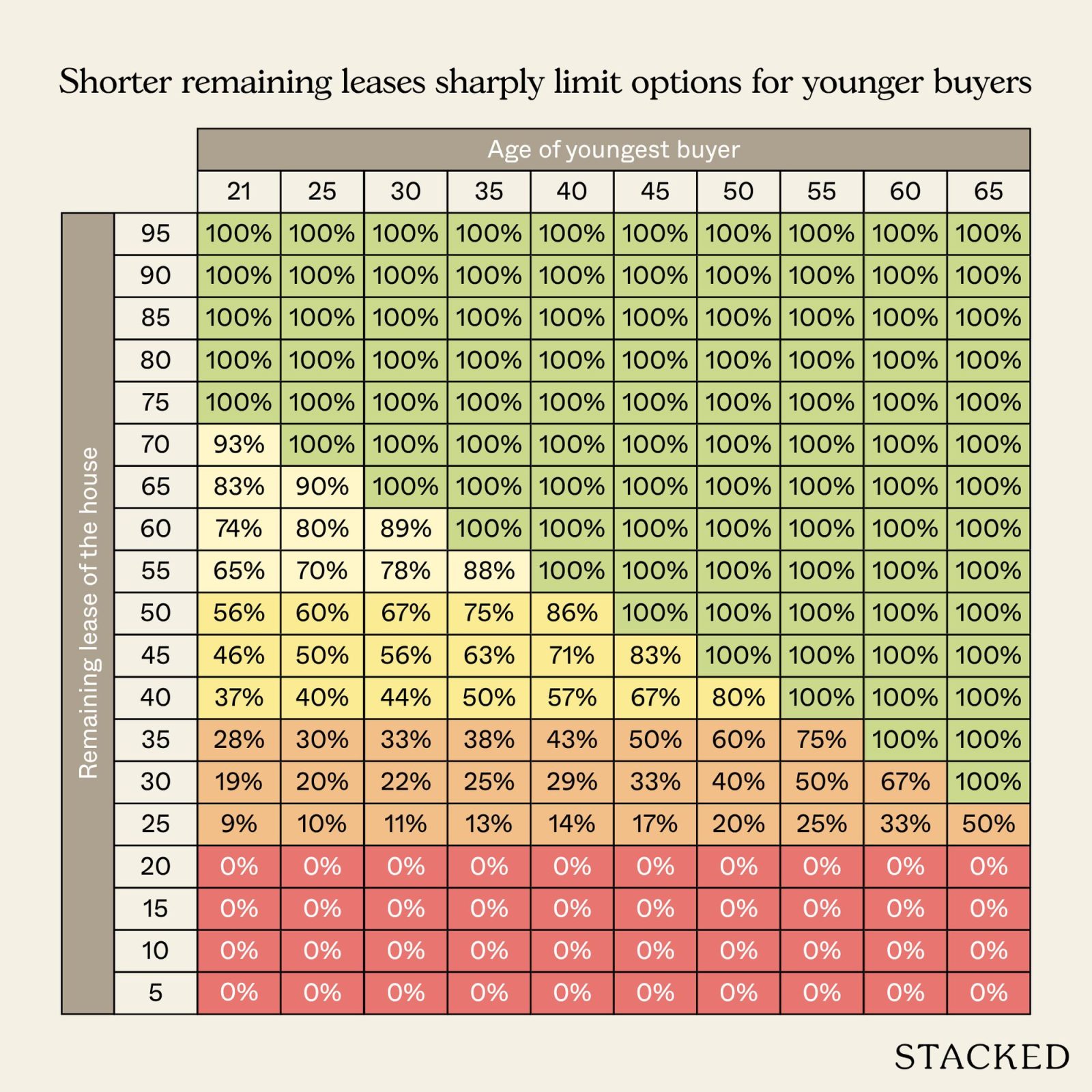

The second constraint they will likely face is appealing to the right pool of buyers. As the remaining lease on the EM shortens, the pool of buyers who can finance this type of public housing purchase narrows because CPF usage is tied to the remaining lease.

The prevailing regulations work as follows: CPF can be used in full only if the remaining lease covers the youngest buyer to age 95. When it does not, CPF usage is prorated, and loan tenures are also compressed accordingly. The table below shows how the numbers shift as the lease shortens.

At the point you purchase the EM in roughly five years, the property will have approximately 65 years remaining on its lease, even with the latest constructed EM on the market. Buyers aged 30 and above can use their CPF in full at that lease length, and the purchase remains accessible to a wide range of buyers.

But the conditions at the time of inheritance are different. For example, if you and your husband both pass in 35 years, the remaining lease at that point would be around 30 years. A 35-year-old buyer at that stage would be limited to using roughly 25% of their CPF. Younger buyers would face even tighter restrictions, and both CPF and loan amounts would be curtailed.

To make up for the difference, buyers in that position will need substantially more cash upfront, and the group of buyers that can meet all of that criteria is much smaller.

Moreover, the appreciation in average EM prices over the past decade compounds this issue.

Based on data compiled by Stacked, average resale prices across all lease cohorts now sit between $950,000 and just over $1 million, up 38% to 52% from a decade ago. This is largely attributed to the price premium that some buyers have placed on flats with larger layouts, and the appeal of a split-level public housing home at a fraction of landed property prices.

Average EM resale prices by lease start year, 2015-2025

| Year | 1975-1984 | 1985-1994 | 1995-2004 |

| 2015 | $725,643 | $664,924 | $627,465 |

| 2016 | $732,861 | $684,677 | $638,393 |

| 2017 | $730,455 | $682,042 | $644,820 |

| 2018 | $746,572 | $677,706 | $634,927 |

| 2019 | $720,413 | $666,735 | $612,837 |

| 2020 | $703,150 | $676,141 | $649,322 |

| 2021 | $790,094 | $751,148 | $732,922 |

| 2022 | $878,960 | $830,017 | $819,968 |

| 2023 | $930,071 | $874,604 | $840,201 |

| 2024 | $948,317 | $927,109 | $894,088 |

| 2025 | $1,004,711 | $980,500 | $954,020 |

| % change from 2015 to 2025 | 38.46% | 47.46% | 52.04% |

At those price points, a CPF restriction of even 33% means a buyer must find close to $640,000 from a bank loan and cash combined, with the loan tenure also compressed due to the shorter lease. The higher the purchase price, the larger the gap CPF restrictions leave, and this shrinks the pool of buyers who can practically bridge it.

The EM could still be sold, but it will probably take a longer marketing period, and with less room to hold out for a better offer.

From an optimistic perspective, since the government has stopped building new EM flats, the available supply of these flats is fixed. This generates a degree of scarcity that could offer some degree of price support among buyers who specifically want the split-level layout.

Recent transactions reflect this: EMs in mature, central estates such as Bishan and Queenstown have been changing hands between $1.3 million and $1.6 million, while those in newer towns such as Sengkang typically fetch between $950,000 and $1.1 million.

But supply scarcity cannot offset the financing constraints on the demand side. If buyers genuinely want the property but cannot structure the financing to complete a purchase, that interest does not translate into a transaction.

What your exit options actually look like

Given the constraints we’ve laid down – the inheritance rules and the financing limits on buyers – there are three broad paths available to you and your family. None eliminates the eventual need to sell, but they differ significantly in how much control your children have over the timing and terms of that sale.

Option 1: Agree on an exit window now, while you still can

The most useful thing you can do for your children is to take the decision-making out of their hands before the circumstances do it for them. That means your family agreeing, while you are still around, on a rough trigger point for when the property should be sold.

A useful benchmark is the remaining lease at which the financing constraints start to noticeably restrict the buyer pool. Based on the CPF table above, a remaining lease in the 45-50 year range still gives buyers in their 40’s access to a substantial portion of their CPF, and loan tenures remain workable. Below 40 years, the restrictions tighten quickly, and the buyer pool contracts.

If your children can initiate the sale while the lease is still in the 45-50 year window, they have time to find a motivated buyer at a reasonable price without pressure. Below that threshold, they are increasingly dependent on cash-heavy buyers, and the negotiation shifts in the buyer’s favour.

This does not require a fixed calendar date. It requires the family to treat the eventual disposal as a planned event rather than an open question, and it needs to be decided while you are around to be part of that conversation.

Option 2: Rent out the upper floor and use the income to hold the property

Your plan to rent out the upper floor once the children move out is a sensible one, and the EM layout suits it. A self-contained upper floor is a more natural rental proposition than individual room letting, and demand for affordable rental space in established HDB estates tends to be steady.

The rental income helps the property pay for itself through the holding period, covering maintenance fees, property tax, and incidental costs. That reduces the financial drag of holding an asset your children are not living in.

What it does not change is the eventual sale. The CPF constraints and inheritance rules discussed above apply regardless of whether the property was rented during the holding period. Rental extends the useful life of the property, but it does not improve the exit conditions. Your children would still be selling under the same buyer pool and lease constraints, just at a later point.

There are also practical trade-offs to manage: tenant sourcing and turnover, lease renewals, and the coordination involved in a rental arrangement on a property neither of them is living in. These are manageable, but they are real, and they become less straightforward as both the children and the property age, particularly given the maintenance issues that tend to surface in older flats.

This path works if your children are willing to go into it with a clear sense of when the rental period ends and the sale process begins, rather than treating the rental as an indefinite arrangement that defers the harder decision.

Option 3: Rent the space you need, and own something your children can more easily capitalise later on

Given that your primary concern is your children’s eventual position rather than the property itself, it is worth considering whether buying an EM is the only way to achieve what you need.

An alternative is to rent a large-format home for your multi-generational household in the near term, while directing your capital towards an asset that your children can handle more easily, such as a freehold or longer-lease property with fewer restrictions on who can buy it and how it can be financed.

The test of whether this works financially is whether the income from whatever you own can offset, or at least partly cover, the rent on the home you are living in. That alignment is not always achievable, and it depends on how you deploy the capital after selling your condos.

Our suggestion is that this is worth checking out before ruling this structure out.

When the space is no longer needed in a smaller household, and you no longer require the multi-generational layout, you can move. Your children inherit no disposal problem and no financing constraint to navigate.

The trade-offs are equally material, since renting means ongoing costs, less permanence, and less control over the living environment. These are considerations that matter particularly for a household that values stability and staying together.

So what should you do?

You have already made peace with the eventual low value of the EM, which is the right call given what you have laid out. The question is whether the process of getting there is manageable for your children.

There is scope for it to be manageable, but only if it is properly planned and your children agree to go through with it.

The prevailing inheritance rules mean that a child who owns private property may not have the option of simply holding on to the flat. They may need to sell it on a timeline that is partly outside their control. The financing constraints on buyers also mean that a sale under time pressure, with a shortening lease, is not a sale on favourable terms.

The one variable your family controls is the exit window. Agreeing on a target remaining lease at which the property should be on the market (somewhere in the 45-50 year range) gives your children a sale they can execute without being forced into it. The longer that decision is deferred, the less room they have.

What remains within your control is agreeing on that window now, rather than leaving it as an open question for your children to resolve under whatever market conditions exist at the time.

The questions our readers send in are rarely about the market in general. They’re about a home they’re considering, a timeline they’re working towards, or a trade-off they’re trying to make.

That’s where we usually help readers go a step further, applying the same research and decision-making framework behind our articles to their own situation.

If you’re facing a similar decision and would like someone to help you think it through before you commit, you can book a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com. We read every message.

0 Comments