Recently, there has been a debate about whether the government should step in and provide support to condo Management Corporation Strata Title (MCSTs) who may find themselves unable to fund essential works.

This comes as the government reviews the Building (Strata Management) Act, which outlines how MCSTs manage their estates.

But given that about 80% of Singaporeans don’t live in condos, extending government financial support in this area is not something I can ever see most taxpayers supporting.

However, I do recognise the wider underlying issue, in that poorly maintained features in condos become safety hazards that have implications beyond the private owners, but public funding for private property maintenance is an almost impossible sell.

A significant point that needs to be highlighted is the fact that 1,000 out of some 3,750 residential developments are over the age of 30. That’s a number much higher than I would have suspected, as our last deep dive suggested very few projects get that old.

As these projects age, maintenance costs are likely to keep mounting higher, and this may have implications for possible en bloc attempts by owners.

So far, in our young country’s history, the conversation around property en bloc sales has mostly centred on the upside benefits, such as the windfall that owners could make when it happens.

But rising maintenance costs introduce a different kind of pressure. As time goes on and condos age further, the question may shift from whether an en bloc is attractive to whether staying in the condo is even still viable.

Some developments may face a situation where the upkeep and cost to replace ageing features and equipment becomes increasingly expensive, yet they cannot secure the level of consensus needed for a collective sale. Without sufficient sinking funds and with major works looming, they risk being caught in a slow decline, with no clear way out.

One possible direction, at least in theory, is a more conditional approach to collective sale thresholds. For example, developments that are halfway through their lease and don’t have enough in their sinking fund for essential works could be given a lower threshold to attempt a collective sale.

To be clear, that won’t overcome some fundamental issues, such as whether the price makes sense to developers or the existing owners struggling to find a replacement home. But it could offer a possible way out, if any projects ever come dangerously close to wiping out their funds.

So far, we’ve yet to see a condo truly run aground this way, but it is a concern going forward, as more of those 1,000-odd projects start to reach the remaining years on their lease.

There’s another alternative, but it depends on the collective behaviour of the owners.

There have been cases where developments, after unsuccessful en-bloc attempts, have instead chosen to reinvest in maintenance. In some instances, this has proven to be a viable alternative to sale and redevelopment.

A good example is Mandarin Gardens. After its most recent collective sale attempt failed to secure the required 80% support, the direction among residents shifted. Instead of continuing to push for a sale, they focused on renewal and upgrading works.

Residents approved around $5 million in improvements, including works such as water tank replacements and waterproofing, which had previously been hard to gain consensus for.

The failed en bloc attempt partly made these upgrades easier to gain the consensus of most owners there. Once a collective sale is off the table, there may be less incentive to defer maintenance. This is the other path ageing condos can take, but it hinges entirely on the owners’ ability to make such collective efforts.

Going forward, this may also change how buyers consider older resale condos.

Right now, most buyers tend to acknowledge their condo maintenance from the monthly fee they’ll pay. But as more developments age, they’re going to have to pay more attention.

Buyers may need to start probing into the sinking fund, whether major works have been carried out or deferred, whether the MCST has been proactive in managing the estate, and so forth. All of these are factors we take for granted today, but this will have to change as more resale condos enter their final decades.

We also had some questions from readers this week.

I’m 33 this year and don’t have the luxury of waiting for a new launch to complete. I’m currently looking at options like Stirling Residences (newer, leasehold, strong MRT access) and Signature Park (older, freehold, larger units). My main concern is choosing the right first property that can appreciate well and still be easy to exit later. Could you share whether tenure vs location/liquidity matters more for capital gains?

What you’re describing is a common trade-off, and based on how we’ve seen different projects perform over time, here’s what I can say:

The freehold tenure of residential developments can support their property value over the very long term, but it also raises the entry price. That higher base means percentage growth is often weaker compared to leasehold projects in similar locations. In most cases, a much longer holding period is needed to justify the freehold premium; so, unless you’re looking at 15 to 20 years or more, freehold may not pay off in terms of gains.

(There’s a bit more detail on the freehold versus leasehold issue here.)

As for being able to exit easily, larger doesn’t always mean better. There are some nuances involved.

HDB upgraders make up a significant proportion of buyers in the private residential market, and these buyers almost always tend to be families. That means they often prefer family-sized units such as three-bedders and larger-sized units. In this sense, an exit strategy may be easier compared to some compact unit types like a one- or two-bedder.

But in the same vein, HDB upgraders are constrained by their affordability. In most cases, the sale proceeds from the sale of their flat govern what they can afford. As such, a very large unit with a high quantum may price them out, and may be harder to move. As of 2026, for example, a quantum of $1.8 million to $2 million is about what most upgraders can reach. Anything priced above this may see fewer prospective buyers.

(But bear in mind this number will probably change in future, when it’s time for you to sell.)

This can be a reason to go for something more manageably sized: perhaps not the biggest three-bedder in the brochure, but also not an overly compact unit like a one-bedder.

As for location, projects that boast a direct connection to MRT stations, primary school proximity, and nearby amenities tend to attract a broader pool of buyers. This is what supports liquidity and resale volume. In your example, Stirling Residences benefits from being in a city fringe location, with walking access to Queenstown MRT. That kind of positioning tends to attract both owner-occupiers and investors, which supports the underlying resale demand.

Signature Park offers larger units and freehold tenure, which can be appealing for long-term own stay. But as an older development in a less central location, the buyer pool may be narrower. This can affect how quickly you are able to exit, even if the unit itself offers more space.

The decision comes down to your priority. If your focus is on flexibility and ease of exit, Stirling Residences might fit the bill. If you’re more focused on long-term holding and space, then Signature Park may be a better fit.

As an aside, for a first property, your needs are likely to evolve – this is just the first stop on your home ownership journey. As such, most buyers in your position should prioritise the ability to exit cleanly.

Are the record-setting HDB resale prices in Bidadari the reason why prices at Woodleigh Residences have climbed significantly since the start of 2025? Three-bedroom units have gone from about $2.4 million to around $2.8 million. Would somewhere like Hougang make more sense instead, given the lower price and strong connectivity?

This is a good observation, and my answer is that you’re right, but in an indirect way.

Strong HDB resale prices in Bidadari do reinforce the overall positioning of the area. It doesn’t just signal demand and the desirability of the area. It’s because there’s an expectation that – when those Bidadari flat owners are able to sell – their very valuable resale flats will fuel a jump in the demand for private homes in that area.

In general, most HDB upgraders prefer to stay in the same area, even when they buy their next home. So it’s expected that these people will have the desire and the sale proceeds to afford nearby condo units. It sounds a little presumptuous, but that’s the general expectation, and based on anecdotal evidence we’ve heard from agents on the ground, it often bears out.

That said, the price movement at Woodleigh Residences is not just about Bidadari.

A big part of it comes down to its positioning as an integrated development. It’s still the only one in that immediate area with direct access to Woodleigh MRT and a mall. As a coincidence, we did a study on Park Colonial this week, which based a bit part of its marketing on being next to Woodleigh Residences but cheaper; some of the same insights apply, so check it out here.

In any case, what you’re seeing now is less about Bidadari alone and more about how Woodleigh Residences came in and set a much higher price benchmark.

As for Hougang, you’re right that it offers strong connectivity and a lower entry price. I do think a lot of properties here make sense right now, from a value perspective.

I’d say Woodleigh is more about convenience within a newer, curated environment. Hougang offers broader connectivity and a more mature estate, but besides the amenities being older (not necessarily something you might mind), Woodleigh has one other edge: it’s only one stop away from Serangoon, which is also home to NEX Megamall, and is itself as developed as Hougang.

Do write in if you have a shortlist of specific properties you’re comparing, as this will boil down to project specifics more than the general neighbourhoods.

Meanwhile, in other property news…

- With mortgage rates falling, it may be time to update yourself on how much you could be saving on home loans. Check out what you need to know about refinancing right now.

- Will the upcoming Dover Drive GLS site be a future condo worth watching? Check out the details here.

- Lease decay affects all HDB flats – but join us on Stacked Pro as we see how it’s not quite the same in every town, and how it’s happening in Woodlands.

Weekly Sales Roundup (16 – 22 March)

Top 5 Most Expensive New Sales (By Project)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| 32 GILSTEAD | $14,488,320 | 4219 | $3,434 | FH |

| UPPERHOUSE AT ORCHARD BOULEVARD | $7,911,000 | 2056 | $3,848 | 99 yrs (2024) |

| SKYE AT HOLLAND | $5,924,000 | 1765 | $3,356 | 99 yrs (2024) |

| NAVA GROVE | $4,629,800 | 1722 | $2,688 | 99 yrs (2024) |

| GRAND DUNMAN | $4,498,000 | 1787 | $2,517 | 99 yrs (2022) |

Top 5 Cheapest New Sales (By Project)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| NARRA RESIDENCES | $1,366,000 | 646 | $2,115 | 99 yrs (2025) |

| THE SEN | $1,515,000 | 678 | $2,234 | 99 yrs (2025) |

| COASTAL CABANA | $1,554,000 | 915 | $1,698 | 99 yrs (2024) |

| THE SEN | $1,556,000 | 678 | $2,295 | 99 yrs (2025) |

| RIVELLE TAMPINES | $1,588,000 | 883 | $1,799 | 99 yrs |

Top 5 Most Expensive Resale

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| LE NOUVEL ARDMORE | $19,500,000 | 3843 | $5,074 | FH |

| BISHOPSGATE RESIDENCES | $15,000,000 | 4607 | $3,256 | FH |

| BOULEVARD 88 | $10,500,000 | 2799 | $3,752 | FH |

| LEEDON RESIDENCE | $6,098,000 | 2110 | $2,890 | FH |

| MARTIN PLACE RESIDENCES | $5,650,000 | 2002 | $2,822 | FH |

Top 5 Cheapest Resale

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| PALM ISLES | $668,000 | 506 | $1,320 | 99 yrs (2011) |

| HAIG 162 | $695,000 | 366 | $1,899 | FH |

| RIVIERA 38 | $735,888 | 452 | $1,628 | 999 yrs (1882) |

| ALEXIS | $785,000 | 420 | $1,870 | FH |

| EIGHT RIVERSUITES | $793,000 | 441 | $1,797 | 99 yrs (2011) |

Top 5 Biggest Winners

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | RETURNS | HOLDING PERIOD |

| LE NOUVEL ARDMORE | $19,500,000 | 3843 | $5,074 | $3,510,000 | 5 Years |

| MARTIN PLACE RESIDENCES | $5,650,000 | 2002 | $2,822 | $2,966,760 | 17 Years |

| URBAN EDGE @ HOLLAND V | $4,100,000 | 2325 | $1,763 | $2,370,000 | 20 Years |

| CASHEW HEIGHTS CONDOMINIUM | $2,770,000 | 1658 | $1,671 | $2,050,000 | 28 Years |

| THE BAYCOURT | $2,680,000 | 1647 | $1,627 | $1,815,325 | 22 Years |

Top 5 Biggest Losers

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | RETURNS | HOLDING PERIOD |

| SCOTTS SQUARE | $4,028,000 | 1249 | $3,226 | -$818,120 | 19 Years |

| OUE TWIN PEAKS | $1,050,000 | 549 | $1,913 | -$360,930 | 9 Years |

| V ON SHENTON | $1,240,000 | 689 | $1,800 | -$207,000 | 14 Years |

| AVENUE SOUTH RESIDENCE | $980,000 | 527 | $1,858 | -$99,000 | 5 Years |

| THE CREST | $3,380,000 | 1658 | $2,039 | -$36,340 | 6 Years |

Top 5 Biggest Winners (ROI%)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | ROI (%) | HOLDING PERIOD |

| CASHEW HEIGHTS CONDOMINIUM | $2,770,000 | 1658 | $1,671 | 285% | 28 Years |

| MANDARIN GARDENS | $1,450,000 | 1001 | $1,448 | 237% | 23 Years |

| THE BAYCOURT | $2,680,000 | 1647 | $1,627 | 210% | 22 Years |

| HILLINGTON GREEN | $2,225,000 | 1356 | $1,641 | 208% | 23 Years |

| CASPIAN | $2,338,000 | 1399 | $1,671 | 173% | 17 Years |

Top 5 Biggest Losers (ROI%)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | ROI (%) | HOLDING PERIOD |

| OUE TWIN PEAKS | $1,050,000 | 549 | $1,913 | -26% | 9 Years |

| SCOTTS SQUARE | $4,028,000 | 1249 | $3,226 | -17% | 19 Years |

| V ON SHENTON | $1,240,000 | 689 | $1,800 | -14% | 14 Years |

| AVENUE SOUTH RESIDENCE | $980,000 | 527 | $1,858 | -9% | 5 Years |

| KINGSFORD WATERBAY | $1,118,000 | 850 | $1,315 | -2% | 8 Years |

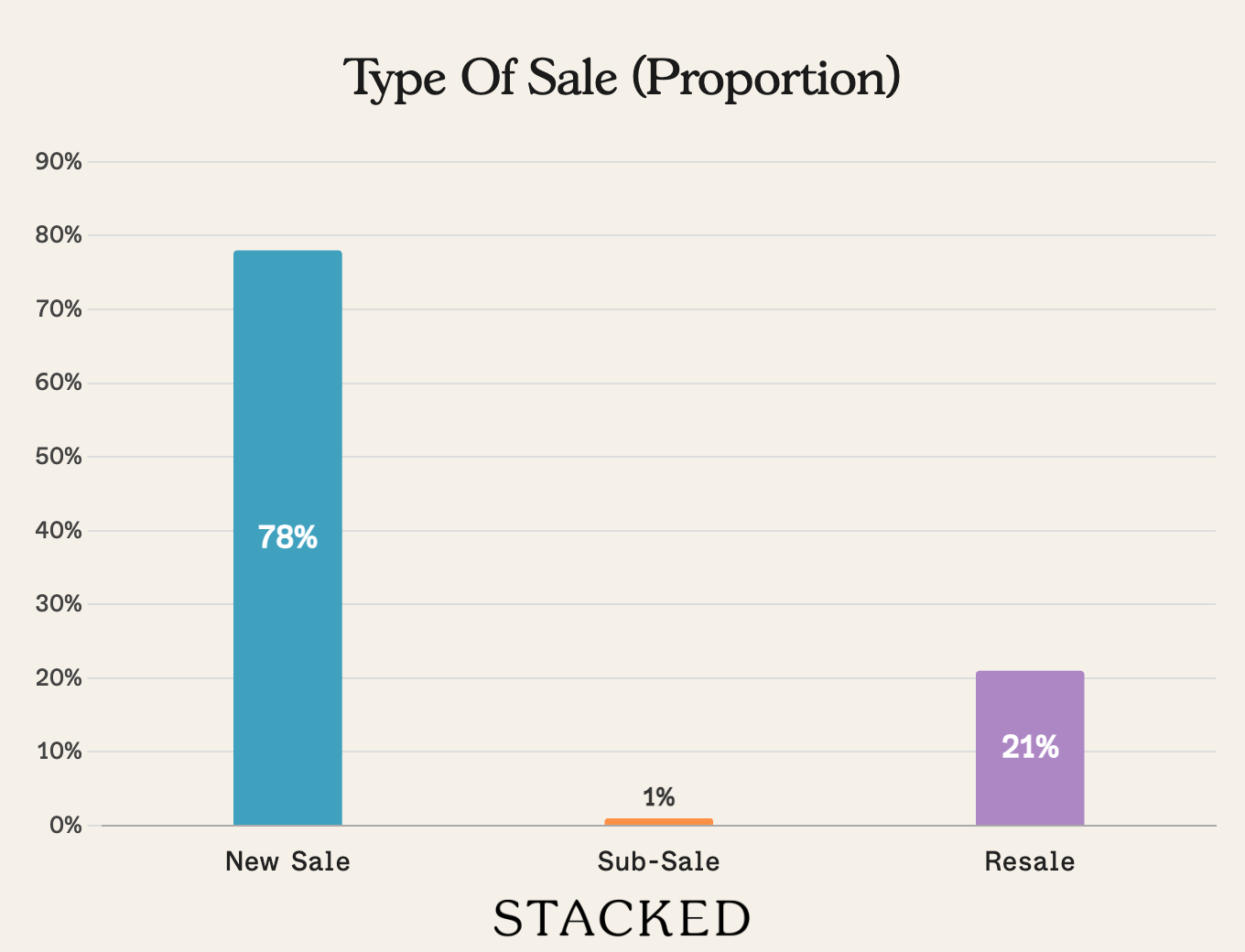

Transaction Breakdown

Follow us on Stacked for more news and updates on the Singapore property market.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

0 Comments