Resale flat prices are at an eight-year high; but market watchers saw it coming as early as October 2020. At the time, the volume of resale transactions were at the highest point since 2010; and the momentum doesn’t seem to be slowing. This week, we took a look at the hottest HDB towns by sheer volume of resale transactions; and the names may surprise you:

HDB towns with highest resale volumes

The following are based on total resale transactions between January 2020, and February 2021:

Highest overall increase in transactions:

| HDB Town | Total transactions recorded | Volume increase | Percentage increase | Average price (as of Feb 2021) |

| Punggol | 2,090 | 252 | 146% | $480 psf |

| Sengkang | 2,414 | 105 | 33% | $443 psf |

| Choa Chu Kang | 1,015 | 77 | 65% | $402 psf |

| Toa Payoh | 792 | 72 | 84% | $561 psf |

| Bedok | 1,478 | 69 | 37% | $459 psf |

Highest increase in transactions for 3-room flats

| HDB Town | Total transactions recorded | Volume increase | Percentage increase | Average price (as of Feb 2021) |

| Clementi | 318 | 25 | 89% | $492 psf |

| Ang Mo Kio | 603 | 23 | 30% | $405 psf |

| Bukit Merah | 353 | 21 | 50% | $548 psf |

| Toa Payoh | 375 | 20 | 53% | $398 psf |

| Kallang / Whampoa | 306 | 18 | 53% | $434 psf |

Highest increase in transactions for 4-room flats

| HDB Town | Total transactions recorded | Volume increase | Percentage increase | Average price (as of Feb 2021) |

| Punggol | 1,185 | 140 | 156% | $479 psf |

| Sengkang | 1,281 | 57 | 32% | $452 psf |

| Choa Chu Kang | 539 | 41 | 61% | $412 psf |

| Queenstown | 342 | 37 | 116% | $798 psf |

| Bedok | 557 | 25 | 36% | $465 psf |

Highest increase in transactions for 5-room flats

| HDB Town | Total transactions recorded | Volume increase | Percentage increase | Average price (as of Feb 2021) |

| Punggol | 651 | 94 | 168% | $469 psf |

| Sengkang | 948 | 53 | 47% | $425 psf |

| Bedok | 279 | 29 | 74% | $486 psf |

| Toa Payoh | 168 | 28 | 165% | $685 psf |

| Choa Chua Kang | 395 | 26 | 59% | $385 psf |

What’s unusual about the resale market in 2020 to 2021?

A combination of two factors is supporting the resale HDB boom. First, we have a bumper crop of around 50,000 flats reaching their Minimum Occupation Period (MOP) over these two year. Among these are highly desired five-year old flats, as they have the advantage of being already built, but with negligible lease decay.

The second factor is Covid-19, which is causing some buyers to act more conservatively than they would otherwise. For example, some buyers have upgraded from their existing flat to a bigger or better located resale flat, instead of a new launch condo. This increases affordability, while at the same time alleviating worries of construction delay.

As such, we would expect the HDB resale market to sustain its momentum for the remainder of 2021 as well. However, not all HDB towns are benefitting proportionally. The following towns are doing better (see above), and these are some probable reasons:

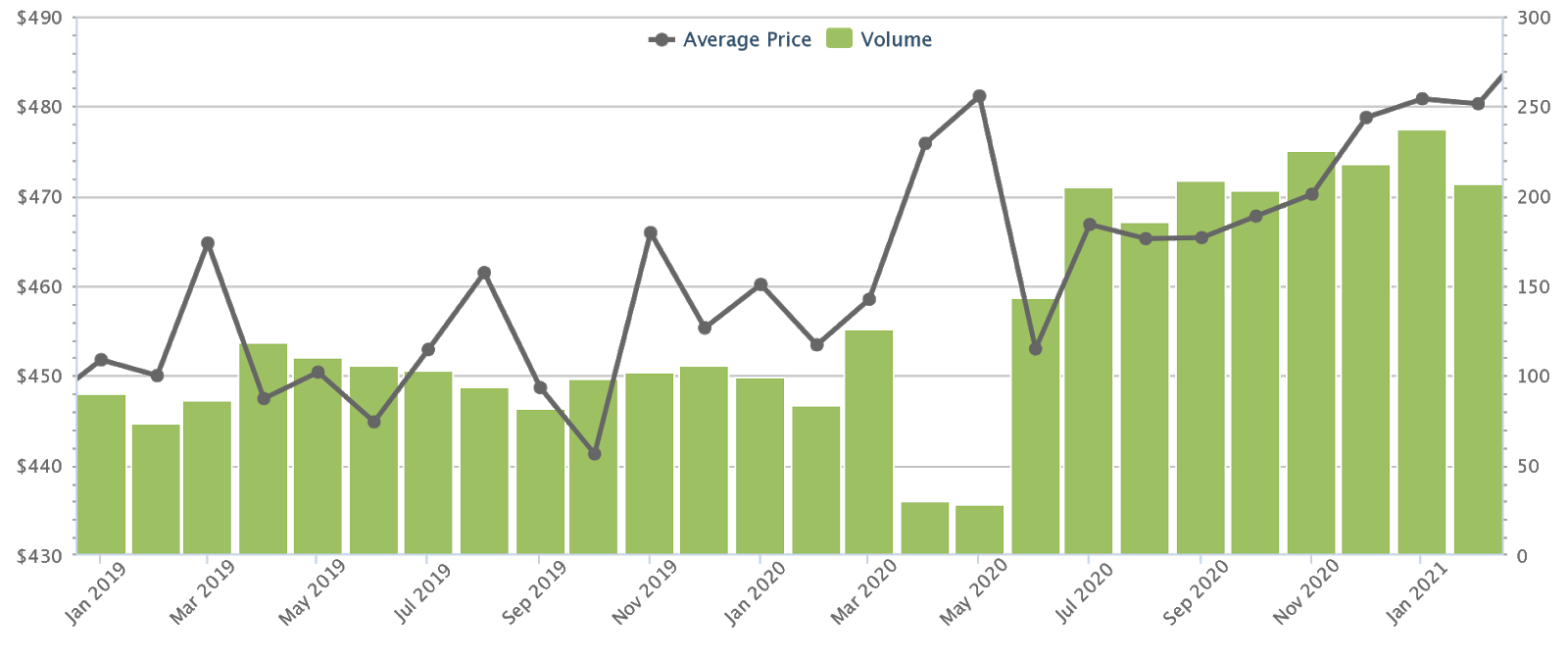

1. Punggol

Following the end of the Circuit Breaker, Punggol has managed to maintain transaction volumes exceeding 200 units for every month except August 2020. By contrast, there was no single month in which Punggol resale transactions crossed 118 units.

One reason is simply the number of flats reaching MOP in this town. An estimated 5,206 flats in Punggol will reach MOP in 2020/21, the third highest number behind Choa Chu Kang and Sengkang (see below).

The second factor is growing awareness of the Punggol Digital District (PDD), and the likely extent of the impact. This is an enterprise district, where Singapore Institute of Technology (SIT) will be clustered with tech businesses and test-bedding facilities. It will also feature Nexus, a major mall adjoined to the upcoming Punggol Coast MRT station. Those who have seen the transformation of the One-North tech-hub, and the resulting impact on neighbours like Clementi, are expecting a similar phenomenon.

Finally, the completion of Waterway Point resolves many of the longstanding issues here. While it’s not new (Waterway Point was announced in 2011, and completed in 2016), approximately 542,493 sq. ft. mall resolves many amenity issues that once plagued Punggol (It is currently very crowded though). The Boardwalk (linking the mall with Waterway Park and the MRT) forms a much-needed hub for retail, dining, and family recreation.

Punggol feels much less sparse compared to a few years ago, and latecomers are starting to pile into the district as they finally notice the changes (latecomers because, as you can see above, prices have already risen significantly since 2019).

2. Sengkang

From August to January 2020, Sengkang has mostly maintained resale transactions above 240 units per month. The exception would be November (still 221 units), and finally a dip in February to 205 units. By comparison, Sengkang never managed to exceed 193 transactions for any given month, for all of 2019.

Sengkang has the single highest number of flats reaching MOP for 2020 / 21, at around 6,618 units. This can be attributed to the massive developments in the Fernvale area, from 2015 – Fernvale Rivergrove and Fernvale Lea alone account for an estimated 2,678 flats reaching MOP.

While Sengkang is far from mature, it’s actually one of the best-connected towns.

From inception, Sengkang’s HDB projects have been constructed in tandem with its public transport nodes. As a result, Sengkang’s LRT system is top-notch, linking Sengkang MRT station, bus interchange, and Compass One mall all at a single point. Sengkang also has two MRT stations on the North-East Line (NEL), with Buangkok MRT station in Sengkang Town itself.

Age may also have something to do with the area’s popularity; Sengkang is associated with younger families – this provides a reputation of being vibrant and dynamic, instead of plain “ulu”. It’s an advantage that towns like Sembawang and Punggol never experienced.

Incidentally, an overlooked aspect of Sengkang is the Seletar Aerospace Park. This is a much-underrated dining and recreational hub.

3. Choa Chu Kang

Choa Chu Kang has the 2nd highest number of flats reaching MOP (around 6,250 units). The bulk of these come from Keat Hong, which saw aggressive development in the previous decade; an impressive 4,800+ resale flats reaching MOP are all from this general area.

Choa Chu Kang is one of the more affordable HDB towns, with resale prices averaging $402 psf; by comparison, the average across Singapore, in February 2021, was $468 psf. Note above that Choa Chu Kang’s 5-room flats average $385 psf, making them one of the most affordable housing options for larger families.

Ironically, Choa Chu Kang also saw the single most expensive resale flat transaction for a non-mature estate in February; this was $890,000 for a rare maisonette at Choa Chu Kang Street 64. But this was an outlier, which doesn’t reflect on the overall resale flat market here.

Choa Chu Kang is currently benefiting from the development of the Rail Corridor, which cuts across its eastern fringe. Note that completion is scheduled for 2021, so there’s almost no wait time for home buyers who move in this year.

Choa Chu Kang won’t be cheap for too long; we expect prices to start meeting the island-wide average by 2025 / 26. This is when the Jurong Rail Line (JRL) will be nearing completion, providing better access to the retail hub of Jurong East.

4. Toa Payoh

Toa Payoh saw a surge of interest in its larger 5-room units, with prices hitting a remarkable $685 psf for the month of February. Previously in January, Toa Payoh also saw four resale flats meet the million-dollar mark; these were for 5-room DBSS flats at The Peak.

That said, we probably don’t need much explanation as to why Toa Payoh (and neighbouring Bishan) are resale flat hotspots – they have been for many years, and likely will be for many more.

This is thanks to their city fringe location and heavily built-up amenities. The Thomson Line, with Brighthill, Upper Thomson, and Caldecott MRT, have further helped to improve connectivity for Toa Payoh and Bishan alike. As such, even the higher prices are doing very little to put off buyers; especially HDB upgraders (considering many have the funds for a condo, a Toa Payoh resale unit is well within their means).

5. Bedok

For all of 2019, it was rare to see Bedok cross 101 transactions; this only happened on four occasions in July, September (barely at 104 transactions), October and November.

After the Circuit Breaker however, resale transactions in Bedok remained above 130 transactions for every month except November 2020 (122 units), and recently in February 2021 (117 units).

That said, Bedok is difficult to generalise due its staggering size – this is the largest planning area in Singapore, spanning from Changi to Bedok Reservoir to the boundary lines of Eunos and Pasir Ris. Being such a large mature area, it’s unsurprising that many resale flat transactions will fall somewhere within its borders.

We would expect continued interest in Bedok North and Bedok South in coming years, thanks to increasing development of the Tanah Merah Kechil link area. Tanah Merah being a connecting point to Changi airport will also help to maintain interest.

Is the surge in the resale flat market sustainable?

There’s growing preference for resale flats as a first-time home, as more Singaporeans aspire toward the private market.

The MOP countdown begins at completion, not purchase. This means that if you buy a BTO flat, the time before you can sell is typically eight to nine years (around three to four years for construction, plus the five-year MOP). With a resale flat, there is only the MOP to contend with. Given that private property prices tend to rise faster than flat prices, many upgraders feel a sense of urgency.

That said, transaction volumes are likely to level off going into 2022/23, as the bumper crop of resale flats is absorbed.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

0 Comments