Dear Ryan,

I’ve been reading your articles and find them very informative. I would like to seek your advice on what I can do with regard to my property.

I am 45 years old and single and looking for passive income or capital gains for my retirement. I currently own a 2+1 bedder condominium (99 years leasehold) which is about 13 years old which I bought for about $700k with a remaining loan amount of about $330k. The condominium is in district 16. The place is currently unoccupied as I am staying with a friend.

I have currently about $240k in cpf and if I were to sell my current place, about $280k would be returned to my cpf. I earn about $10k per month.

I am thinking of the following options:

1. Sell the current place to earn capital gain and use the profits with a new bank loan to buy a new condominium and sell the new condominium upon TOP.

2. Rent out the current place for rental income.

3. Sell the current place to earn capital gain, keep the profits as retirement fund and buy a resale hdb flat as retirement home using cpf only.

4. Sell the current place to earn capital gain and buy a smaller unit at a new condominium for rental and keep as future retirement home.

Thank you.

(This is part of an ongoing series where we answer reader questions about the property market. If you have one of your own, send it to stories@stackedhomes.com.)

Hi there,

As always, happy to hear that our content has benefitted you in some way.

It’s always good to start your retirement planning early. You’re in a good position where you’re still working and able to take advantage of your age to secure a decent amount of loan. We will run through your affordability as well as the options you’ve listed, but the first step is to determine how your current property is performing.

The challenge for many buyers today isn't access to information.

It's interpreting that information in a way that makes sense for their finances, goals, and stage of life.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

How is your current property performing?

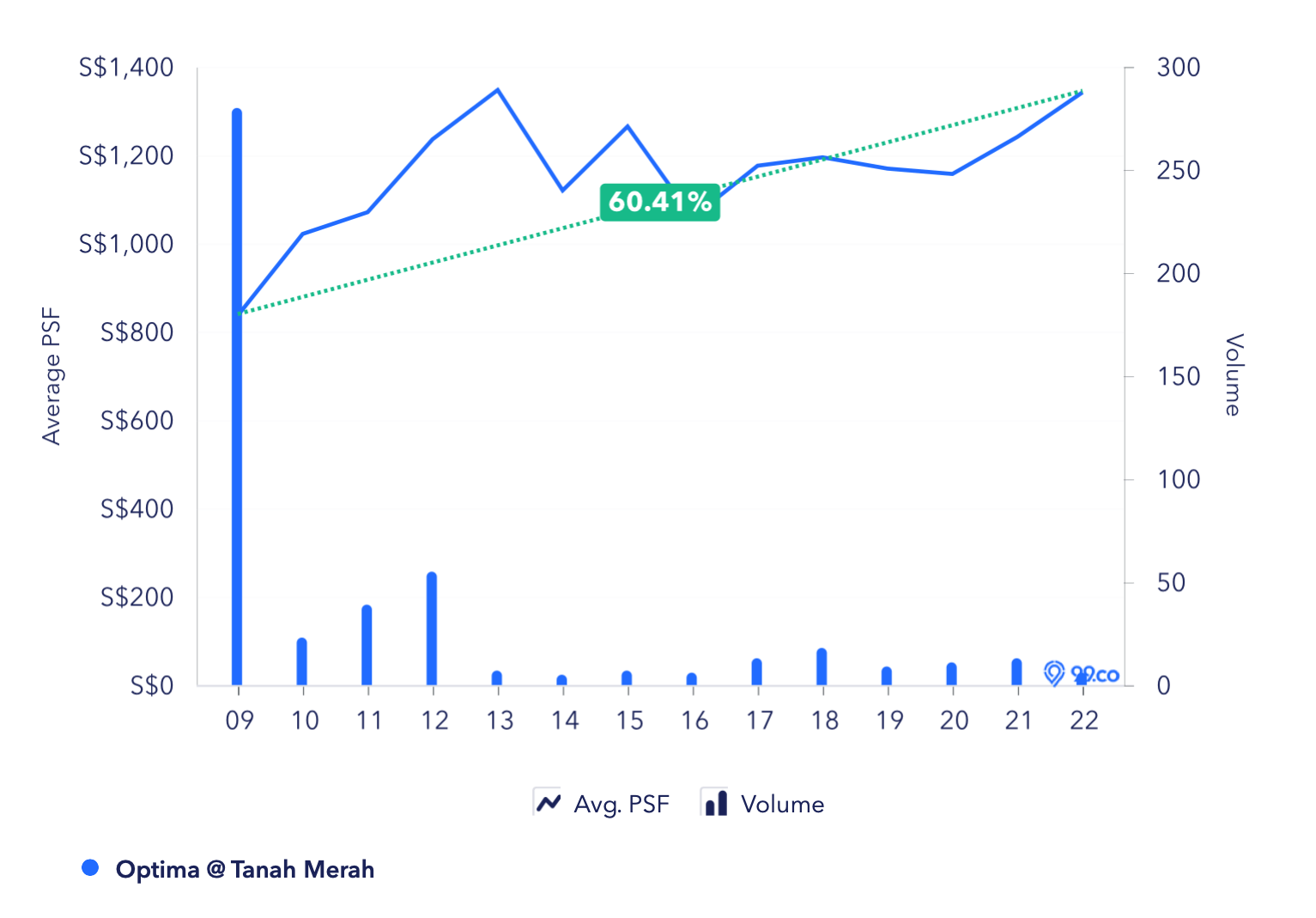

From the information that you’ve provided, it’s likely that the property you’re currently holding onto is a unit at Optima @ Tanah Merah. It’s the closest in age in District 16 with a lease starting from 2008 which would make it 14 years old this year.

With that out of the way, let’s take a look at how Optima @ Tanah Merah is performing:

Since its launch, prices have gone up by 60% which is excellent. From the graph it may seem like prices are going up and down between the years 2013 – 2017 but this is because there were very few transactions each year (less than 10 from 2013 – 2016 and only 13 in 2017) which affects the average PSF.

For instance, in 2013 there were just 7 transactions, out of which 5 are 1 and 2 bedders. Also, smaller unit types tend to have a higher PSF so naturally, the average PSF went up. Then in 2014, there were 5 transactions, out of which 3 are 3 bedders so the average PSF went down.

To date in 2022, there have only been 6 transactions out of 297 units. This translates to a 2% turnover rate which is rather low. A low turnover rate would mean prices are not able to grow as quickly because banks value a property based on recent transactions.

For example, let’s say that out of these 6 transactions in 2022, 1 or 2 owners are desperate and sold at a low price. This will likely affect the valuation of the other units as well, as there aren’t enough transactions to support a higher price.

Also, due to the low number of transactions, it may not always accurately reflect the performance of the project.

Based on the data from Edgeprop, there were 132 profitable sales and 12 unprofitable sales in the development.

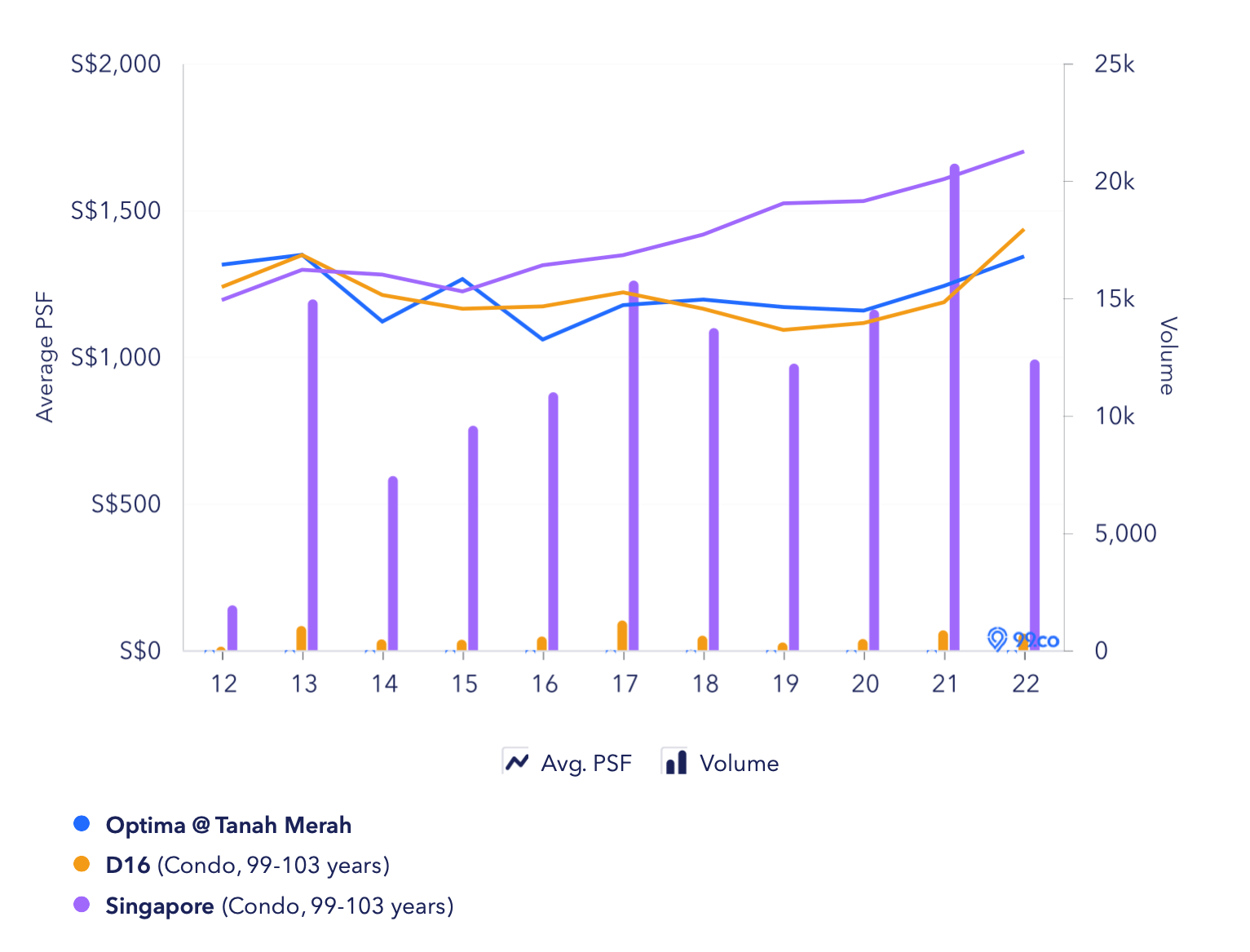

The price trend of Optima @ Tanah Merah is pretty comparable to the average prices of 99-year leasehold developments in District 16. Its low number of transactions causes more peaks and troughs and is probably the reason they are not exactly parallel. However, we can see from the graph that there is a growing gap between the prices of Optima @ Tanah Merah and the overall prices of 99-year leasehold developments in Singapore.

These are some of the recent 2-bedroom transactions in Optima @ Tanah Merah:

| Date | Size (sqft) | Unit type | PSF | Price | Level |

| Nov 2022 | 840 | 2 | $1,257 | $1,055,000 | #06 |

| Apr 2022 | 850 | 2 | $1,388 | $1,180,000 | #07 |

| Apr 2022 | 840 | 2 | $1,310 | $1,100,000 | #13 |

| Dec 2021 | 969 | 2 + S | $1,239 | $1,200,000 | #12 |

In the past year, only one 2 + S was sold. The average PSF for these transactions is at $1,299 and the average price is at $1,133,750.

So assuming you purchased the 915 sq ft 2 + S during the launch at $700,000 and using the average PSF of $1,299, the selling price is approximately $1,188,585. As such, we will use $1,180,000 to determine your affordability for the next place.

Affordability

For selling

| Description | Amount |

| Selling price | $1,180,000 |

| Outstanding loan | $330,000 |

| CPF refund | $280,000 |

| Estimated cash proceeds | $570,000 |

For buying

| Description | Amount |

| Maximum loan based on a fixed monthly income of $10K and age 45 | $907,620 (20 years tenure) |

| CPF funds ($240K in OA + $280K refund after the sale) | $520,000 |

| Cash | $570,000 |

| Total loan + CPF + cash | $1,997,620 |

| BSD based on $1,997,620 | $64,505 |

| Estimated affordability | $1,933,115 |

Now that we know your affordability, let’s run through the options you’ve listed!

Option 1: Cash out on the current property to purchase a new condominium and sell it upon TOP

For this, let’s be conservative and look at a purchase price of $1.5M instead of maxing out your budget at $1.9M, as it is only prudent to save some funds for emergency purposes considering the loan depends solely on your income.

These are some of the new launches that are currently available on the market below $1.5M:

| Project | District | Tenure | Unit type | Level | Size (sqft) | PSF | Price |

| Lentor Modern | 26 | 99 years | 1b1b | #25 | 527 | $2,550 | $1,344,000 |

| Leedon Green | 10 | Freehold | 1b1b | #11 | 474 | $2,941 | $1,394,000 |

| Kopar @ Newton | 09 | 99 years | 1b1b | #20 | 517 | $2,756 | $1,425,000 |

| Bartley Vue | 19 | 99 years | 2b1b | #15 | 657 | $2,204 | $1,448,000 |

| Pasir Ris 8 | 18 | 99 years | 2b1b | #04 | 710 | $2,076 | $1,474,000 |

Do note that these developments were picked purely on the basis that they are within your affordability so it’s advisable to consult an agent for further analysis.

Many buyers have the impression that buying a new launch and selling it upon TOP will most definitely be profitable but this is a misconception. There are new launches that are unprofitable, people just don’t talk about them as much. We have previously done an article on this and you can read more on that here.

For a more balanced view, here’s a simplified look at some of the pros and cons of buying a new launch:

| Pros | Cons |

| You are buying in at a similar price range with your neighbours (who will be your competitors when you decide to sell the place) | Locations are limited to wherever the launches are (not an issue if you’re buying for investment) |

| The financial burden will not be as heavy for an initial couple of years with the progressive payment scheme | Longer waiting time (unable to rent out while the building is under construction) |

| Development is brand new so you have a fresh lease and can save on renovations | Unable to see the unit physically and don’t know who your neighbours are |

Since your intention is to sell upon TOP, let’s do a 5-year projection assuming you were to sell your existing property and purchase a unit at Bartley Vue for $1,448,000.

For our growth rate, we’ll look at how the private property index has fared in the past 10 years but we’ll halve this since we are looking at a 5-year horizon:

| Year | Property Price Index |

| 2012 | 151.5 |

| 2013 | 153.2 |

| 2014 | 147 |

| 2015 | 141.6 |

| 2016 | 137.2 |

| 2017 | 138.7 |

| 2018 | 149.6 |

| 2019 | 153.6 |

| 2020 | 157 |

| 2021 | 173.6 |

| 2022Q3 | 187.1 |

| Construction progress | Time period |

| Completion of foundation | 6 – 9 months |

| Completion of reinforced concrete | 6 – 9 months |

| Completion of brick wall | 3 – 6 months |

| Completion of ceiling/ roofing | 3 – 6 months |

| Completion of electrical wiring/ plumbing | 3 – 6 months |

| Completion of roads/ car parks/ drainage | 3 – 6 months |

| Issuance of Temporary Occupation Permit (TOP) | 3 – 6 months |

| Certificate of Statutory Completion | 6 – 12 months |

| Description | Amount |

| Assuming 11.7% growth over 5 years | $1,617,416 |

| Current valuation | $1,448,000 |

| Interest costs (Assuming loan of $855,600 at 4% interest with 20 year tenure) | $60,419 |

| MCST (Assuming $300/month – only pay for a year as estimated TOP is in 2026) | $3,600 |

| Estimated gains | $105,397 |

Do note that these projections are just meant to be a guide and will change depending on market conditions.

The actual gains may be more because you still have some cash proceeds leftover from the sale of your current property which we set aside for emergency funds.

Option 2: Rent out the current place

In the last 6 months, there were 23 2-bedder rental transactions in Optima @ Tanah Merah:

| Date | Size (sqft) | Price ($) |

| Sep 2022 | 800 to 900 | 3,700 |

| Sep 2022 | 1,300 to 1,400 | 4,600 |

| Sep 2022 | 800 to 900 | 4,000 |

| Sep 2022 | 1,000 to 1,100 | 3,600 |

| Sep 2022 | 800 to 900 | 3,700 |

| Sep 2022 | 800 to 900 | 3,100 |

| Sep 2022 | 600 to 700 | 3,700 |

| Aug 2022 | 900 to 1,000 | 3,600 |

| Aug 2022 | 900 to 1,000 | 3,900 |

| Aug 2022 | 1,000 to 1,100 | 3,300 |

| Jul 2022 | 1,000 to 1,100 | 4,000 |

| Jul 2022 | 900 to 1,000 | 3,050 |

| Jul 2022 | 600 to 700 | 3,000 |

| Jul 2022 | 1,000 to 1,100 | 3,500 |

| Jul 2022 | 1,000 to 1,100 | 4,500 |

| Jul 2022 | 600 to 700 | 4,000 |

| Jul 2022 | 800 to 900 | 3,700 |

| Jul 2022 | 900 to 1,000 | 3,650 |

| Jul 2022 | 1,000 to 1,100 | 3,300 |

| Jul 2022 | 900 to 1,000 | 3,800 |

| Jun 2022 | 900 to 1,000 | 3,500 |

| May 2022 | 900 to 1,000 | 3,600 |

| May 2022 | 800 to 900 | 3,400 |

The average rental for a 2 bedder is at $3,661 per month. If we were to only look at the 2 + S which are between 900 – 1,000 sq ft, the average rental is $3,586 per month. Based on the estimated selling price of $1,180,000, the rental yield will be 3.65%.

Let’s take a look at how that compares with other 2-bedroom rentals in the immediate vicinity:

| Project | Completion date | Size range (sqft) | Average rent (last 6 months) | Average price (last 10 months) | Rental yield |

| Grandeur Park Residences | 2020 | 500 – 900 | $3,344 | $965,000 (only 1 transaction) | 4.16% |

| eCO @ Bedok South | 2017 | 800 – 1100 | $3,502 | $1,332,000 | 3.15% |

| Urban Vista | 2016 | 500 – 1300 | $2,722 | $874,631 | 3.73% |

| The Glades | 2016 | 500 – 900 | $3,188 | $983,429 | 3.89% |

Given that Optima @ Tanah Merah is older compared to these developments (TOP in 2012), the rental yield is pretty decent.

We will also do a 5-year projection to compare with Option 1.

| Description | Amount |

| Assuming 11.7% growth over 5 years | $1,318,060 |

| Current valuation | $1,180,000 |

| Interest costs (Outstanding loan of $330,000 at 4% interest with 17-year tenure) | $58,869 |

| MCST (Assuming $300/month) | $18,000 |

| Rental income ($3,586/month for 11 months a year) | $197,230 |

| Agency fees ($1,793/year) | $8,965 |

| Estimated gains | $249,456 |

To rent out the current unit instead of selling and buying a new launch will make you $144,059 more ($249,456 – $105,397). These additional gains are mostly from the rental income and also assuming the growth rates are the same for both developments.

Option 3: Cash out on the current place, keep the profits as retirement funds and buy a resale HDB as a retirement home using only CPF funds

Unfortunately at this point in time, this option is not as feasible due to the September 2022 cooling measures. This is because there is now a 15-month wait-out period if you sell your private property to downgrade to a resale HDB flat. (Although they have stated that this is a temporary measure rather than a permanent one).

And since you are below the age of 55, that concession doesn’t apply to you as well. If anything, the wait-out period may be beneficial for you, as more supply will be coming onto the market in the next few years.

Nevertheless, let’s just see the options available to you at this point in time.

After selling your condo, your CPF funds will add up to $520,000. Setting aside $20,000 for BSD, legal and agency fees will mean you’ll have a budget of $500,000.

These are the median resale prices by town and flat type for resale cases registered in the third quarter of 2022:

| TOWNS | 1-ROOM | 2-ROOM | 3-ROOM | 4-ROOM | 5-ROOM | EXECUTIVE |

| ANG MO KIO | – | * | $365,500 | $516,500 | $800,000 | * |

| BEDOK | – | * | $355,000 | $475,000 | $680,000 | $820,000 |

| BISHAN | – | – | * | $640,000 | $855,000 | $1,045,000 |

| BUKIT BATOK | – | * | $353,000 | $500,000 | $720,000 | $790,900 |

| BUKIT MERAH | * | * | $368,000 | $765,000 | $875,000 | – |

| BUKIT PANJANG | – | * | $386,500 | $471,900 | $610,000 | $750,000 |

| BUKIT TIMAH | – | – | * | * | * | * |

| CENTRAL | – | * | $460,000 | $680,000 | * | – |

| CHOA CHU KANG | – | * | $380,000 | $493,900 | $588,000 | $742,000 |

| CLEMENTI | – | * | $385,000 | $555,000 | * | * |

| GEYLANG | – | * | $320,000 | $560,000 | $738,900 | * |

| HOUGANG | – | * | $370,000 | $506,000 | $648,400 | $822,000 |

| JURONG EAST | – | * | $355,000 | $460,000 | $619,000 | * |

| JURONG WEST | – | * | $339,000 | $475,000 | $565,000 | $665,000 |

| KALLANG/WHAMPOA | – | * | $390,000 | $778,400 | $840,000 | * |

| MARINE PARADE | – | – | $412,500 | * | * | – |

| PASIR RIS | – | * | * | $519,000 | $619,000 | $780,000 |

| PUNGGOL | – | * | $436,900 | $555,000 | $612,000 | * |

| QUEENSTOWN | – | * | $395,000 | $860,000 | $894,000 | * |

| SEMBAWANG | – | * | * | $515,000 | $566,000 | $636,500 |

| SENGKANG | – | $317,500 | $438,000 | $536,000 | $595,400 | $723,600 |

| SERANGOON | – | – | $380,000 | $520,900 | * | * |

| TAMPINES | – | * | $395,000 | $530,000 | $650,000 | $844,000 |

| TOA PAYOH | – | * | $341,400 | $740,000 | $870,000 | * |

| WOODLANDS | – | * | $345,000 | $468,000 | $560,000 | $778,000 |

| YISHUN | – | * | $362,000 | $473,000 | $608,000 | $748,000 |

Unless you’re aiming for flats in Central Area, Queenstown or Toa Payoh (particularly newer flats), $500,000 in CPF funds will not be an issue if you are considering just 3 or 4-room flats.

HDB has a ruling that owners are not allowed to rent out their whole unit before the flat obtains its MOP, but you are allowed to rent out the bedrooms. You’ll also need to stay in the flat. So perhaps you can rent out one or two of the bedrooms depending on whether you purchase a 3 or 4-room flat and earn some passive income.

The assumption here is that you’ll invest the remaining cash proceeds for at least the next 5 years:

| Description | Amount |

| Assuming 7% returns annually | $799,454 |

| Initial investment | $570,000 |

| Estimated gains | $229,454 |

This option is definitely the least stressful financially as you would have fully paid off the property, plus you will be earning a passive income if you rent out the rooms and also gains from investing the cash proceeds.

Option 4: Cash out on the current property to buy a smaller unit at a new condominium for rental and keep it as a future retirement home

If you were to buy a brand new condominium, that would mean you have to wait 3 – 4 years for it to be completed before you can rent it out, so unless you can stay in the alternative accommodation during that period, this may not be a viable option.

Currently, the lowest-priced new launch condo is at $1.23M for a 398 sq ft studio unit at Irwell Hill Residences. If you were to utilise all your CPF funds plus pay the 5% downpayment in cash, you’d still need to take a loan of $648,500.

At 4% interest with a 20-year tenure, this would mean a monthly repayment of $3,929.52 after the project obtains its CSC. Renting it in the future could partially help to cover the monthly mortgage.

However, in 10 years time you will be 55 years old and if you do plan to move in by then, paying $3,900 monthly may be a rather heavy financial burden. Plus, you will still have another 10 years of payment to go. Although you likely won’t be retired at 55, it’s worth taking into consideration that you might prefer to be more financially free at that stage of your life.

Let’s say you were to purchase this new launch at $1.23M and rent it out for 5 years upon TOP:

| Description | Amount |

| Rental income (Assuming $3,100/month for 11 months a year) | $170,500 |

| MCST (Assuming $250/month) | $15,000 |

| Agency fees ($1,551/year) | $7,755 |

| Interest costs (Assuming loan of $648,000 at 4% with a 20 year tenure) | $118,471 |

| Estimated gains | $29,274 |

As you can see, the interest costs will significantly reduce your gains.

If your plan is to keep the property as a retirement home, you won’t be able to cash out from it so the most important thing is whether or not the property you purchase can also meet your lifestyle needs. If you do prefer having facilities at your doorstep, you could also consider purchasing a resale project which you can immediately rent out for rental income while you’re staying at the alternative accommodation.

One good thing about a new launch is that it’s nice and new. But if your plan is to buy and rent it out, it becomes irrelevant as, by the time you move in further down the road, you would not have been able to enjoy the development while it was brand new. Also, given the higher price you’re paying for a new launch (per square foot, at least), the rental yield may not necessarily be better than a resale unit.

These are some of the most affordable 1 bedder units currently on the market:

| Project | District | Tenure | Unit type | Size (sqft) | Asking price |

| Cavan Suites | 08 | Freehold | 1b1b | 365 | $620,000 |

| Suites @ Shrewsbury | 11 | Freehold | 1b1b | 370 | $620,000 |

| Thomson V One | 20 | 99 years | 1b1b | 420 | $620,000 |

| Riverbay | 12 | 999 years | 1b1b | 387 | $625,000 |

| Mountbatten Lodge | 15 | Freehold | 1b1b | 334 | $648,880 |

We will assume you use your CPF funds and cash to fully pay off this property. Let’s say you were to purchase the unit at Riverbay at $625,000 and rent it out for 5 years:

| Description | Amount |

| Rental income (Assuming $2,075/month for 11 months a year) | $114,125 |

| MCST (Assuming $250/month) | $15,000 |

| Agency fees ($1,037/year) | $5,185 |

| Estimated gains | $93,940 |

Just like with Option 3, as you’re planning to keep this property as your retirement home, you won’t be able to cash out from it but we will still do a 20-year projection until your presumed retirement at 65 years old:

We will use the Property Price Index (20-year horizon) for the projection. As of 2022Q3, the PPI stands at 187.8. Compared to 2002Q4 (82.3), this is a 128% increase in 20 years.

| Description | Amount |

| Assuming 128% growth over 20 years | $1,425,000 |

| Current valuation | $625,000 |

| Interest costs (House is fully paid) | $0 |

| MCST fees (Assuming $250/month) | $60,000 |

| Estimated gains | $740,000 |

For this option, it gives you an alternative route should you decide later down the road that you’d like to cash out and downgrade to an HDB instead.

Having said that, how you choose the property matters a lot if you’re looking out for capital gains – and it’s not always the ‘obvious’ things that determine this such as the freehold status.

For example, we knew someone with a $1.3 million budget looking to invest in a small unit, ultimately shortlisting two properties – The Sound (freehold) and Stirling Residences (99-year leasehold).

Between the two, The Sound seemed like a better choice given its freehold status, lower $PSF and upcoming MRT station along the Thomson-East Coast line.

It was also smaller so the overall cost was lesser than the new Stirling Residences.

Fast forward 4 years later, and you can see that the unlikely winner Stirling Residences had a much larger profit:

If you account for cost such as agent fees, taxes and maintenance fees, you’ll also see that the $30,000 profit from The Sound would more or less disappear.

Purchased in the same year for around the same $PSF and size – yet about a $200,000 profit difference!

From here, it’s easy to see how doing a projection table can only serve as a guide. Ultimately, it’s down to whether or not you’re able to pick out a fundamentally sound property that suits your objectives.

Conclusion

Seeing that your current property has appreciated pretty well, it may be a good time to cash out while the development is still relatively young.

Option 1 would definitely be ideal provided the new launch you purchase becomes profitable upon TOP or soon after. With this option your monthly repayment is lower, reducing your financial stress but the potential gains are not guaranteed.

For Option 2, a rental yield of 3.65% is decent and still comparable with newer projects in the vicinity. In the current climate, it is a lot easier to start collecting rental income and ride on the potential capital gains of the development in the next 5 years as compared to banking on a new launch to become profitable upon TOP. Selling and buying would also incur more fees than if you were to just hold on to the property to rent it out.

Option 3 will be the least financially taxing given that the property will be fully paid with your CPF and you will have cash on hand which you can put into other investments or just keep it if you so wish. Although again do note, you will have a 15-month wait-out period so you will need a place to stay in the meantime or at least account for the cost of rent.

As for Option 4, buying a new launch to rent out and eventually move into could be quite a heavy financial burden especially when age catches up. This, of course, will depend on the individual, but most people would prefer to have more financial freedom by then. Perhaps buying a more affordable resale unit which you can rent out immediately would be a better choice. This option will also allow you one more opportunity to cash out and downgrade if the right property is chosen.

Another option you can also consider is to purchase a dual key unit as a retirement home so even when you are staying in the unit, you will still be able to earn passive income that can partially cover the mortgage and eventually support your retirement.

Perhaps instead of choosing just one option, you can do a combination of 2 of these options. Since you’re only 45 years old now and you have an alternative accommodation, you could go with Option 2 to take advantage of the hot rental market and look toward Option 3 or 4 depending on the retirement home you eventually want to live in.

Have a question to ask? Shoot us an email at stories@stackedhomes.com – and don’t worry, we will keep your details anonymous.

For more news and information on the Singapore private property market or an in-depth look at new and resale properties, follow us on Stacked.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

0 Comments