In this Stacked Pro breakdown:

- We uncover why most CCR shoebox units are underperforming in capital gains—even after holding periods of over eight years.

- See how ABSD can completely wipe out any meaningful returns, unless you structure your investment with care.

- Discover the few CCR projects where investors saw 2.5 per cent annualised gains—and why these are the rare exceptions.

Already a subscriber? Log in here.

The shoebox craze ended many years ago, but elements of it still linger. One of the common sayings from that period – that “shoeboxes in the CCR are good investments” – still lingers.

However, our examination of the numbers suggests otherwise: several signs point to CCR-showboxes showing lacklustre gains, and perhaps being hampered by higher initial price points. Here’s what to know before you buy or invest:

The challenge for many buyers today isn't access to information.

It's interpreting that information in a way that makes sense for their finances, goals, and stage of life.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

Examining shoebox units for rental and resale gains

For the following, we will look at shoebox transactions from 4th January 2011 through to the end of 2024.

This is because the Sellers Stamp Duty (SSD) was introduced on 4th January 2011. Transactions before the SSD were more profitable over a much shorter period, and that would be misleading considering the regulatory environment today.

Let’s look at how they performed in general for resale gains:

| Type of sale | Average of % | Average of annualised | Average of holding period | Volume |

| New Sale to Resale | -0.7% | -0.1% | 8.4 | 299 |

| Resale to Resale | 1.5% | 0.4% | 6.2 | 194 |

This generally isn’t great. On average, we see a slight capital loss for new sale to resale. This is even with a more substantial number of units transacting in this category (299 to 194). Also note the long holding period (8.4 years), which shows that gains are not materialising even after fairly long periods.

This is partly because shoebox units miss out on a big chunk of prospective resale buyers: HDB upgraders make up a large percentage of condo buyers, but upgraders are families. They have no use for a shoebox unit, hence the weaker performance in new-to-resale transactions.

An experienced realtor, however, gave us another reason why this makes sense:

When CCR shoebox units are sold by the developer, they tend to have a higher price per square foot (this has been true since before COVID). The secondary market is unwilling to accept that price, hence many of the initial buyers incur a small capital loss.

But subsequently, in resale-to-resale transactions, sellers are able to resell the unit with marginally better results. This explains the small gain of 1.5 per cent in resale-to-resale transactions.

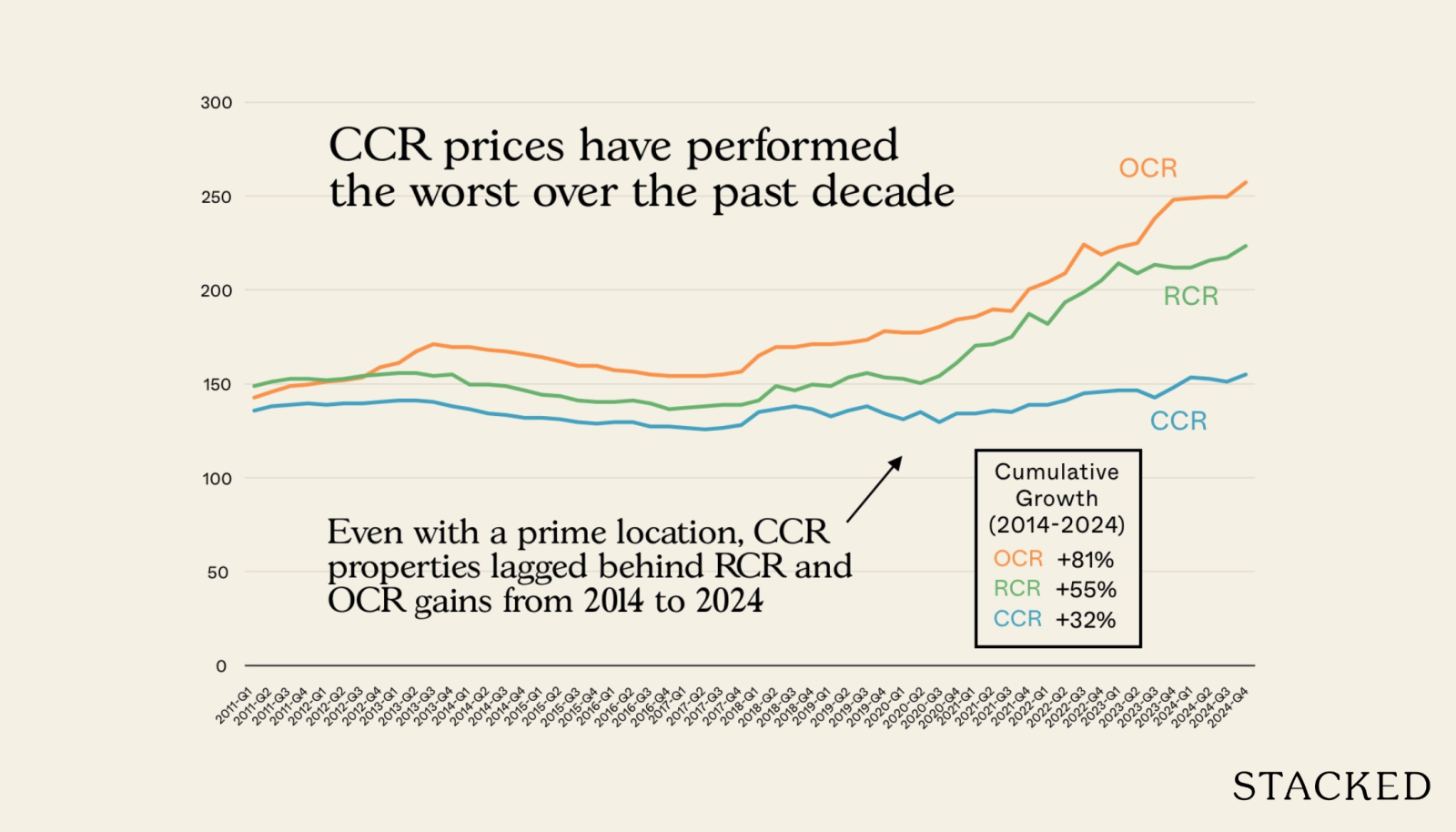

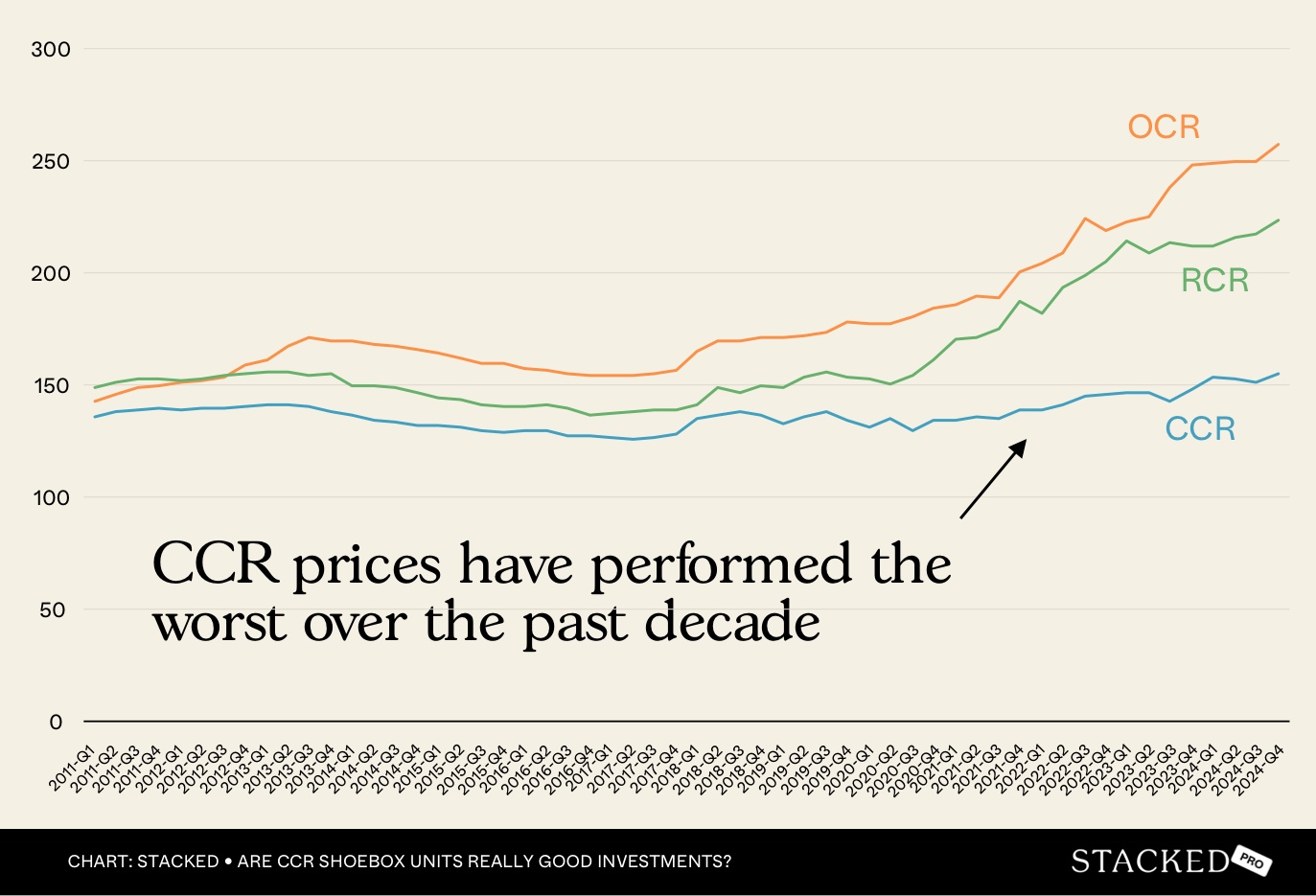

Next, let’s look at region-specific performance:

The gains specific to the CCR are the worst among the three regions. Why?

0 Comments