Buying property abroad can be riskier, not least because you’re entering a real estate market – and legal jurisdiction – you may not understand as well. But at the same time, there sometimes is a tendency to exaggerate or misunderstand the exact nature of those risks. So for those of you who are seriously considering a second property abroad, take note of the following:

Common misconceptions of buying overseas property:

Most of these misconceptions stem from oversimplification. While there may be a kernel of truth, generalising them is often a mistake, or misdirects you from where the real risk lies:

- Issues of instability or corruption

- Reliability of foreign developers

- Complicated buying process and taxes

- Financing difficulties

- Unpredictable yields and gains

- Exchange rate complications

- Only “golden postcodes” make any money

1. Issues of instability or corruption

Not every property investment overseas is going to be plagued by corruption, require bribes, involve unlicensed real estate sales, etc. Most mature states, like Japan or the UK, have well-enforced laws. Perhaps a useful reference here is the Corruption Perceptions Index, which is updated annually.

A loose rule of thumb is to stick to countries within the top half of the list (e.g., only countries that rank 89 or above), although some investors may have more stringent standards*.

As with buying property in Singapore, you can scrutinise the development team as an added safety measure. It’s a fairly safe bet that proven international developers, like Australia-based Lendlease, or the UK-based Berkeley Group, would not attempt to build properties in corrupt or unstable states. Some of these large developers have local projects that you can visit (Lendlease, for instance, is behind the development of Paya Lebar Quarter).

*For example, some investors will consider only the top 10 or 20 ranked countries; but this confines them to only the most expensive real estate markets. States that top the list tend to also have the highest standards of living and housing.

Beware knee-jerk reactions and cries of “instability”

For mature countries, it’s important to avoid having too much of an episodic view (e.g., predictions based on central bank policy, or whether there was a protest match recently).

For gatekeeper cities, property prices tend to be resilient even in the face of one-off events. Even with the Covid-19 pandemic, for example, close to half (45 per cent) of major capital cities in Knight Frank’s Prime Global Cities index have reported property sales back to pre-pandemic levels in Q3 2020.

We’re not saying you should ignore the potential risks, just that you should be wary of knee-jerk reactions and exaggerations stemming from current events.

Property investment is inherently long-term; so as with local investments, it’s better to analyse performance over long periods of 10 to 15 years, rather than make investment decisions (or decisions not to invest) just based on what’s happening this year.

Some countries are faced with serious, long-term instability; but this will then be reflected in the long-term performance of their properties as well (assuming records exist).

As with most investments there is a risk-return trade off here. In other words, the potential return rises with an increase in risk. “Riskier” countries do have a higher potential for growth, where as with stable countries such as Singapore, you don’t expect there to be as much room for growth as before.

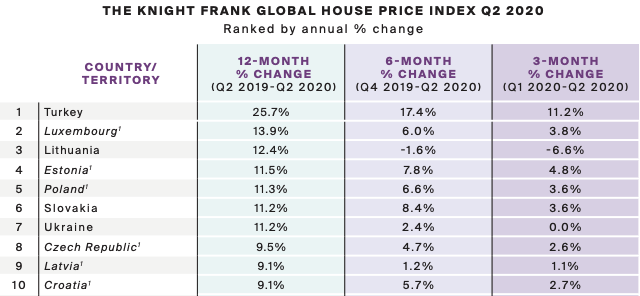

It is all the more obvious when you look at a recent Knight Frank global house price index in 2020. The top 10 growth in housing prices all come from countries that you’d typically associate with a “riskier” investment.

Contrast that to Singapore, which is all the way in the 48th place, with a 0.4% growth up till Q2 2020.

2. Reliability of foreign developers

Most of these worries circulate around small local developers, with no portfolio E.g., an investment company that suddenly wants to dabble in real estate. Admittedly, these types of developers like to engage foreign buyers, often because their local banks, property investors, etc. know better.

However, established real estate developers will invariably have a large portfolio; and these are quite easy to check up on. Listed developers will also publish their financial statements, so it’s easy to spot issues like high D/E ratios, or other liabilities (speak to a qualified wealth manager to review these statements, if you’re uncertain).

Finally, you can bypass the “unreliable developer” issue by just sticking to proven international names, as we mentioned in point 1.

Frankly, it really isn’t any much different from investing in Singapore. You’d always need to do the homework yourself (or have a trusted agent for it). Just like the KAP incident in 2019 – where the mall shop owners are suing the developer for misrepresentation through the agents (they were under the guise that there would be an anchor tenant) – you always have to do that due diligence.

3. Complicated buying process and taxes

It’s often believed that buying property abroad is a convoluted process, involving too many middlemen and too much paperwork. Likewise, buyers often worry about taxes, and the amount of accounting work they create.

In mature countries, these issues are no longer as prevalent as before. Thanks to the advent of digital real estate, it’s quite easy to compare prices, contact professionals abroad, or even directly contact the relevant government bodies. Sites like Zillow (US) and Rightmove (UK) provide most of the resources needed. It’s even possible to handle all the paperwork digitally, in some jurisdictions.

In addition, most mature countries – like Singapore – require a conveyancing firm to be engaged. There will be legal professionals to walk you through the process.

Regarding taxation, we’re lucky that Singapore is a global financial hub. Licensed tax agents (which we know are regulated by IRAS) can help you crunch the numbers, and understand the full range of tax implications. The availability of these professional services can help to give you a truer sense of the costs.

Do bear in mind that, even if Singapore doesn’t charge certain taxes, you may be subject to taxation in the other country you buy in – so be sure to weigh these costs against local taxes like the Additional Buyers Stamp Duty (ABSD).

4. Financing difficulties

Singapore banks often give home loans for gatekeeper cities; but the same may not extend to other areas of the country. For example, some Singapore banks will give you a home loan for a property in London, but Bristol is probably out of the question. As such, you may not have to worry too much about meeting credit scores or other loan qualifications from foreign banks.

As an aside, there are some loan types offered by foreign banks that you can never find in Singapore. Examples include perpetual fixed rate loans (all home loans in Singapore eventually revert to floating rates), and interest-only loans (you never pay down the principal, only the interest – this makes cash-flow positive properties more likely).

Regarding the down payment, the Loan to Value (LTV) ratio in many key countries is comparable to Singapore. The LTV limit is 70 per cent in the UK and Australia, for instance, which is close to Singapore’s 75 per cent limit.

The main problem for most buyers won’t be qualifying for a loan. The main challenge is having enough cash, as you can’t use your CPF for overseas property purchases. You should also remember that the home loans have to be serviced in cash.

5. Unpredictable yields and gains

There is no guarantee regarding yields and gains, be it for local or overseas property. In fact, it’s probably not good to take the bias that Singapore’s property market is always more reliable.

For 2021, for example, Knight Frank predicts steady growth in 17 of 22 key markets, ranging from Hong Kong to Sydney. This is regardless – and in some cases even ironically caused – by Covid-19. Low interest rates from US central bank policies are helping to create more cash-flow positive or higher yielding properties in multiple regions; and some of these don’t have stamp duties like Singapore’s ABSD.

Mature countries and gatekeeper cities tend to have extensive real estate data, which makes it quite easy to monitor long term performance. As such, cities like London, New York, Sydney, etc. may not be as volatile as is often assumed. This can be provided by sites like Property Data, which show average costs and yields based on postcode – but these data sources may require paid subscription (you might try asking a relevant realtor for access).

Statista also provides sorted data, such as from lowest or highest yields; but more detailed information requires a premium (paid) account).

When given information by an overseas realtor, be sure to check their statements against as many data sources as you can find; there should be some general corroboration between the two.

6. Exchange rate complications

A common fear is losses due to currency exchange rates. This is a risk, and has to be managed by selling your overseas property at the right time – investors should be well capitalised, so they’re not forced to sell at a time when exchange rates are bad.

You can also make it a point to sell in the currency of the relevant country (e.g., sell in GBP when the property is in the UK), to prevent any losses from an untimely shift in exchange rates.

At any rate, these days it’s easier to open a multi-currency account, so you don’t need to convert the money until rates become favourable to you.

Exchange rates are a serious problem, however, in politically unstable countries (see point 1); investments in these areas are best avoided by the inexperienced.

7. Only “golden postcodes” make any money

This is akin to saying only District 9 or 10 properties in Singapore will make money; it’s over-generalising.

Every city does have its “golden postcodes’, but these areas are not the sole money makers. In fact, prime areas tend to be more defensive as property investments – you are already buying at a high price, which provides less room for appreciation. It’s often the suburban areas where you can spot undervalued properties, or where there’s room for growth.

Where golden postcodes excel, however, is that their demand and property value rarely fall. No matter how much the supply of housing increases, there’s no replacement for a property near the best and most convenient parts of the city. To use a local analogy, another 30 launches in the fringe regions may not cause the price of an Orchard Road condo to budge.

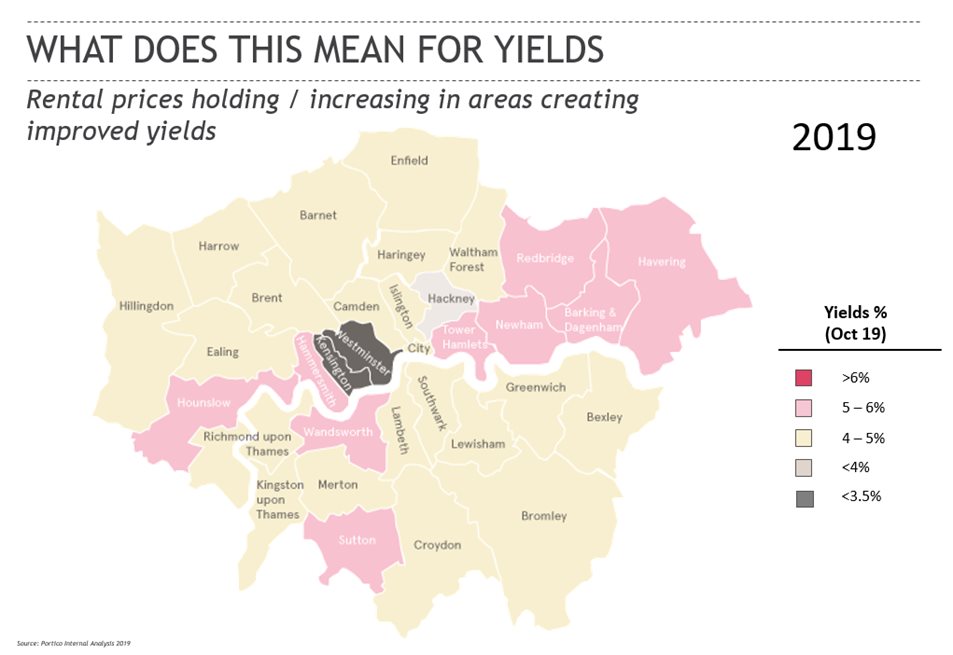

For more developed countries, there will be property sites that help you identify yields and costs – Portico, for instance, provides rental yield information and valuation. However, remember that you should check the movement of yields and gains over a five to 10-year period, rather than just looking at existing rates.

For investors at the right income level, buying overseas property can be a smart move

The ABSD is far from cheap, even if Singapore has no capital gains tax. Furthermore, Singapore doesn’t provide an opportunity for shorter-term property investments, with taxes like Sellers Stamp Duty (SSD) in place to prevent it. As such, overseas properties may simply be better for your bottom line.

However, the need for more cash-in-hand (as you can’t use CPF), and the amount of capital tied up, means it’s not for most first-time investors.

In our next article on overseas property investing, we’ll examine the considerations and purchase decisions of a typical buyer. This will give us a more ground-level look at the challenges involved.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

2 Comments

Looking forward to the next part on overseas property investment!