I like to think of property valuation as a sort of fortune telling.

Sometimes, I think property valuation is less like a science, and more like throwing a deck of tarot cards at a ceiling fan, and then reading whatever meaning you can into the pieces that fall closest to you.

Consider, for instance, the process of shopping for a mortgage. You’ll notice that some banks value your property more, and others less. Some seem to do the process in-house, whereas others take the advice of third-party valuation firms (I know this because, the last time I tried to refinance, I was asked to pay the $700 fee to such a firm).

Property valuation isn’t like physics, where there’s consistency in the rules. There is, for instance, no reliable formula on how much more a unit is worth as you go up or down a floor; and there’s no way to quantify, say, the value of a 3.2 metre ceiling height instead of the normal 2.6 metres.

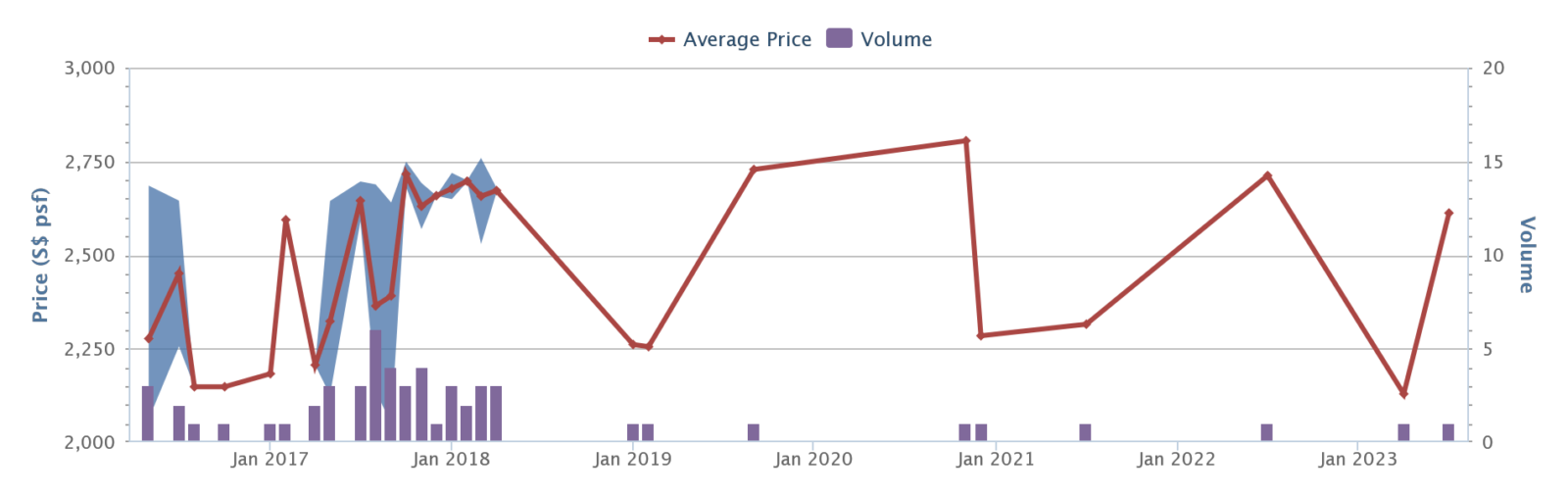

Then there are projects where transactions are few and far between, like this one:

That’s The Asana’s price movement, according to Square Foot Research. There are individual transactions once every few years, so the price is more volatile than an Orchard Towers bar on Friday night.

Is that last price spike to be an accurate representation of value? Who knows?

Maybe the transaction just before it was some parent selling cheap to their own children, so it was sharply undervalued. Or maybe the most recent buyer is the sort who gargles with Bird’s Nest in the morning, and is happy to overpay.

But the real mystery is: who did the valuation, and how did they come up with that figure?

In lieu of a price history (which some might already consider a shaky approach), valuation comes down to some highly subjective elements. Even the companies who try to quantify everything (e.g., they have some sort of proprietary algorithm to figure it out) may not be able to explain why a certain number gets cranked out.

Still, I get why everyone’s reluctant to be too open about it. No one pays for a valuation if the report starts with: “We sort of guess maybe $X,” and no bank wants to say “We based the loan quantum on someone’s guess, more or less.”

That said, we all know that most of the time for the valuation it really comes down to the last few transacted prices at the development. If you get a few previous buyers who just so happened to pay higher cash amounts (so they never cared about the bank valuation anyway), it would mean that you suddenly get a higher valuation.

This can feel like a lot of nonsense, when you shop around for a home loan.

The part that I despise most, when it comes to getting a bank loan, is the valuation. You can try and argue for a higher valuation (so you can borrow more). You can also have your mortgage broker look for banks that will give you/accept a higher valuation.

This is a problem, as it means that these valuations have an indirect effect on property prices. If certain banks are looking to push for higher mortgage targets for the month, you get higher property prices.

And sometimes, it puts you in a bad spot. E.g., Bank A offers a package that’s 3M SORA + 0.7%, whereas Bank B offers a package that’s 3M SORA + 0.9%. But because Bank B is willing to accept a valuation that’s $50,000 higher, you might just accept the higher rate and go with Bank B.

Given that home loans aren’t well-differentiated (there’s little difference besides the interest rate), accepting higher valuations is one of the few ways to attract borrowers, when a loan package is pricey. Quite often, I come across homeowners with terrible loan packages, whose reasoning is just: “they offered the highest valuation.”

If you’re looking for a mortgage, I’d seriously consider the extra interest you’re paying, and your higher stamp duty rates*, before choosing based on the highest valuation.

*Remember that stamp duties like BSD and ABSD are based on the higher of the selling price or valuation.

Elsewhere in Singapore’s real estate scene, we’re starting to see some collaborations.

UOL just teamed up with SingLand and CapitaLand to bid for a site in Tampines Avenue 11. This is for a mixed-use site, with a hefty $1.2 billion price tag. This is something we’re likely to see more of, as rising land prices and development costs are making it harder for developers (even big ones) to go it solo.

This also mitigates some of the risk to developers, such as paying the ABSD if they can’t make the five-year time limit. If they didn’t work together, we’d end up with much smaller – and likely pricier – condo projects.

This does cause one complication though: the new banding system by BCA rates developer quality, and we’ve yet to see what happens if, say, a lower-tier developer teams up with better-rated ones. Can a buyer make a reasonable assessment, without knowing how much involvement the lower-ranked developer has?

Alternatively, it may increase the significance of BCA’s banding to developers.

This might happen if, for instance, better-ranked developers only team up with each other, and refuse to work with lower-tier firms. This could lock out some of the weaker developers from larger, prominent GLS sites. It would, however, incentivise developers to be serious about maintaining their rankings.

Regardless, consortiums are going to happen, given the state of the market today – and we suspect it won’t be long before most new condos bear the names of more than one developer.

Meanwhile in other property news…

- Check out where to find the cheapest three-bedder condo units (starting from $999,000), as of 2023.

- We looked at the 31 most profitable condos over the past 10 years; and you may be surprised at how old some of them are. So much for fears of lease decay.

- For those of you who want dual-key units for rental or extended families, some new launches still have them. There’s not many left though.

- We looked at some unprofitable condo transactions for a change, and found some interesting lessons there too.

Weekly Sales Roundup (14 August – 20 August)

Top 5 Most Expensive New Sales (By Project)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| PARK NOVA | $6,646,000 | 1432 | $4,642 | FH |

| BOULEVARD 88 | $5,266,000 | 1313 | $4,010 | FH |

| MIDTOWN MODERN | $4,093,000 | 1464 | $2,796 | 99 yrs (2019) |

| MEYER MANSION | $3,900,000 | 1389 | $2,809 | FH |

| PULLMAN RESIDENCES NEWTON | $3,820,000 | 1163 | $3,286 | FH |

Top 5 Cheapest New Sales (By Project)

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| THE MYST | $998,000 | 517 | $1,932 | 99 yrs (2023) |

| LENTOR HILLS RESIDENCES | $1,139,000 | 484 | $2,351 | 99 yrs (2022) |

| NORTH GAIA | $1,233,000 | 980 | $1,259 | 99 yrs (2022) |

| PINETREE HILL | $1,285,000 | 538 | $2,388 | 99 yrs (2022) |

| ORCHARD SOPHIA | $1,320,000 | 463 | $2,852 | FH |

Top 5 Most Expensive Resale

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| SEASCAPE | $4,461,000 | 2174 | $2,052 | 99 yrs (2007) |

| COSTA RHU | $3,900,000 | 2239 | $1,742 | 99 yrs (1994) |

| MARINE VIEW MANSIONS | $3,825,000 | 2077 | $1,841 | FH |

| THE SEAFRONT ON MEYER | $3,780,000 | 1615 | $2,341 | FH |

| THE WINDSOR | $3,410,000 | 2454 | $1,389 | FH |

Top 5 Cheapest Resale

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | TENURE |

| PARC ELEGANCE | $650,000 | 398 | $1,632 | FH |

| THE ALPS RESIDENCES | $685,000 | 463 | $1,480 | 99 yrs (2015) |

| SOL ACRES | $700,000 | 495 | $1,414 | 99 yrs (2014) |

| NOTTINGHILL SUITES | $705,000 | 398 | $1,770 | FH |

| NATURA@HILLVIEW | $710,000 | 452 | $1,570 | FH |

Top 5 Biggest Winners

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | RETURNS | HOLDING PERIOD |

| THE WINDSOR | $3,410,000 | 2454 | $1,389 | $2,660,000 | 18 Years |

| MELROSE PARK | $3,300,000 | 1292 | $2,555 | $2,094,000 | 25 Years |

| MERA SPRINGS | $2,840,000 | 1550 | $1,832 | $1,783,000 | 17 Years |

| CENTRAL GREEN CONDOMINIUM | $2,380,000 | 1442 | $1,650 | $1,730,000 | 18 Years |

| SANCTUARY GREEN | $2,870,000 | 1711 | $1,677 | $1,570,000 | 23 Years |

Top 5 Biggest Losers

| PROJECT NAME | PRICE S$ | AREA (SQFT) | $PSF | RETURNS | HOLDING PERIOD |

| THE OCEANFRONT @ SENTOSA COVE | $3,000,000 | 1733 | $1,731 | -$730,000 | 16 Years |

| ROCHELLE AT NEWTON | $3,080,000 | 2164 | $1,424 | -$220,000 | 9 Years |

| THE ASANA | $1,500,000 | 635 | $2,362 | -$190,920 | 6 Years |

| DORSETT RESIDENCES | $1,430,000 | 689 | $2,076 | $44,000 | 13 Years |

| LINCOLN SUITES | $990,000 | 463 | $2,139 | $45,000 | 14 Years |

Transaction Breakdown

Some interesting reads I came across this week:

- Real estate agency shut down for selling a house to a dog

Talk about a ridiculous headline. In this week’s edition of bizarre real estate news, an Iranian couple decided their fur baby, Chester, deserved more than just treats and belly rubs – he got his own apartment!

Yup, they inked the deal with his paw print (because why not?). The reason? No heirs for the couple.

This may sound fine in Singapore, but in Iranian culture, a dog is not seen as a desirable pet. In the end, the head of the property agency was arrested and the firm temporarily shut down.

Chester’s take? Probably chasing his tail in his spacious new living room. Who’s a good homeowner?

- Realtors in Lahaina contacting owners to sell

It’s sad that even in such troubling times, the Maui wildfire victims still have to deal with opportunistic investors and realtors.

That’s right, amidst the devastation, these folks are getting cold calls about selling their land. If you think this is the first time this has happened after such a disaster, this happened to residents of the Florida hurricane situation last year too.

In a bid to stop this, Kāko’o Haleakalā, an organisation focused on preserving lands and native species in Hawaii, took to Instagram to expose these unsolicited pitches. The organisation’s response? If you’re a victim of both the fires and these brazen calls, jot down names. It’s time for a little exposure.

Follow us on Stacked Homes for updates and news on the Singapore property market.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

3 Comments

On Top 5 Biggest Winners, how can One Pearl Bank’s holding period be 23 years when it’s a new launch condo?

You’re making valuation sound like some form of witchcraft. Not all valuers throw a dart on the wall and see what number their dart lands at, there are valuation methods like DCF, T&R, replacement cost etc. that are in line with RICS standards. It’s a bit surprising to see such sweeping statements when your articles have usually been measured and in favour of presenting a fair view.

If anything, based on your article above, it should be buyers looking to maximize their loan amount at the expense of a higher loan cost and SD or the banks looking to maximize their loan books that should be responsible. A transaction is only possible when there is a willing buyer and willing seller, saying valuers are responsible for irrational pricing is like saying an interior designer is responsible for higher construction prices.

P.S. I am not a valuer.