Are Home Prices Finally Cooling Again In 2021?

2021 has been a tough year for buyers; especially first-time home seekers. We’ve seen prices rise in almost every property segment, from resale flats to condos to landed homes. The end of Q2 2021, however, may give buyers a glimmer of hope – while prices are still far from low, at least the pick-up hasn’t been as dramatic as the past four quarters. Here’s what’s happening right now:

Prices rose again in Q2 2021, but at a much slower pace than in previous quarters

According to URA flash estimates, the Residential Property Price Index is at 163.7 points in Q2 2021, up 1.5 points last quarter. This is a 0.9 per cent increase, a significant slowdown from Q4 to 2020 to Q1 2021 (during this time we saw a 3.3 per cent jump).

For condos, OCR properties led the increase, rising 1.8 per cent, higher than the 1.1 per cent pick-up in Q1.

CCR condo prices only edged up slightly by 0.6 per cent, broadly in line with the last quarter. RCR condos accounted for most of the slowdown, with prices rising only 0.3 per cent (RCR condo prices rose 6.1 per cent in the previous quarter).

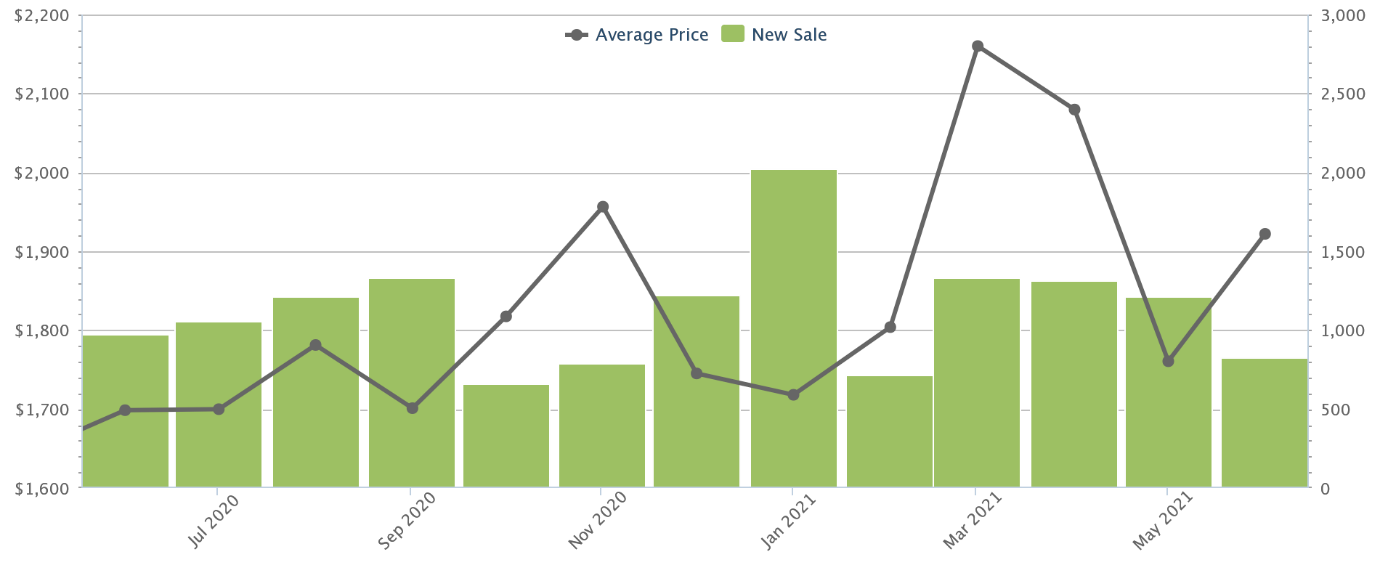

According to Square Foot Research, new launch condo prices now average $1,922 psf, island-wide.

In the resale condo market, average prices are $1,358 psf island-wide.

Note that the decrease in sale price and volumes, for the month of June specifically, was due to a reversion to Phase Two Covid measures. During this time, viewing restrictions and show flat closures caused a sharp temporary dip.

We note that year-on-year, however, prices are still up 7.3 per cent, and Q2 2021 marks the fifth consecutive quarter of rising prices. While momentum is slowing, home prices are still steadily climbing.

What are some advantages for homebuyers in Q2?

- Indications that new cooling measures may not happen after all

- Falling prices in the high-demand Holland V area

- More affordable, upcoming OCR launches

- Home loan rates likely to stay low till 2023

- More GLS sites planned for 2H 2021

1. Indications that new cooling measures may not happen after all

Given the five consecutive quarters of rising prices, there were strong expectations that MAS would announce new cooling measures. So it was a surprise when, on the first of July, MAS clarified that “we do not think the market is overheated right now”.

They’ve been clear that new cooling measures are not off the cards if the situation changes (but new cooling measures are never totally off the cards anyway).

Realtors told us this is both good and bad news for buyers:

“Those who are looking to close soon will not want any sudden restrictions to loan limits, increased ABSD, and so forth; so there’s some peace of mind. But at the same time, we have some buyers who were actually hoping for cooling measures, because there’s a potential knee jerk reaction where developers will cut prices.”

However, realtors noted that it’s an overall plus for buyers. One reason is that fear of new cooling measures can cause a rush to buy, and a sharp momentary spike in prices.

Also, higher stamp duties and loan curbs could more than compensate for discounts, even if new cooling measures did kick in.

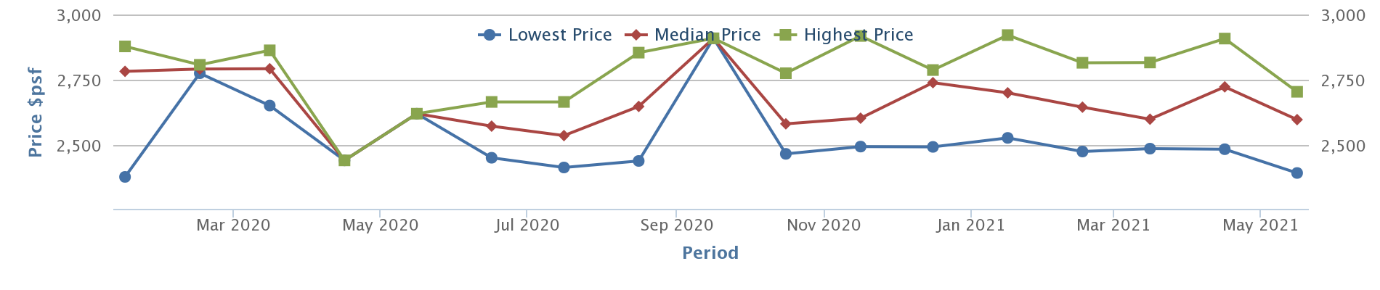

2. Falling prices in the high-demand Holland V area

In our previous article, we mentioned there are seven new condo developments in the Holland V area. Prices have seen steep drops here. For example, Leedon Green, which we pegged for one of the better family condos today, has seen median prices fall from $2,782 psf to $2.597 psf today:

Another example is Hyll on Holland (just located across the road) – where a significant price reduction was enough to move more than 85 units in one weekend.

We’re expecting similar dips in price over the next few months, as developers come close to ABSD deadlines, and competition in Holland V remains as intense as ever.

While pure investors may want to sidestep the fray, this is a chance for genuine homeowners to get a prime area property at lower than expected prices.

3. More affordable, upcoming OCR launches

The OCR saw limited new launches in the past few months, and what’s there has mostly been dominated by Treasure at Tampines. Meanwhile, developments like The Atelier and upcoming Canninghill Piers have been out of reach for the average Singaporean.

In the near term, however, we note a number of more reasonably priced OCR projects coming up. Parc Greenwich EC (next to Greenwich V mall in Yio Chu Kang) and Pasir Ris 8 are all on the horizon. Provence Residence (another EC near Canberra MRT) has also just launched recently in May.

This might help to slow the surge in OCR prices we saw this quarter; as well as provide a more varied mix for new home buyers.

4. Home loan rates likely to stay low till 2023

Home loan rates from banks have averaged 1.3 per cent since 2020. This is due to the Federal Reserve in the United States maintaining a policy of near-zero interest, to stimulate Covid-19 recovery.

At the time when rates dropped, we were warned that it was only temporary; and in fact the Fed did move up its timeline for a rate hike. However, the current expectation is to hit a two per cent goal sometime in 2023, through gradually raising rates. This is generally a relief to home buyers, as the rate hike is still some way off (and is likely to still fall below the CPF and HDB loan rates of 2.5 per cent and 2.6 per cent respectively).

Homebuyers who switched to bank loans in 2008/9 have benefited significantly now, with bank loan rates having been lower than HDB rates for over a decade. However, do note that prior to the Global Financial Crisis, private bank mortgages averaged between three to four per cent.

5. More GLS sites planned for 2H 2021

For those eyeing the resale market, you’ll be glad to know the Government is raising land supply for the second half of 2021.

Supply is being raised by 24.6 per cent, from an estimated 1,605 new homes in 1H 2021, to 2,000 new homes in 2H 2021. At present, the confirmed GLS site list includes four residential sites, including an EC site:

| Location | Gross Plot Ratio | Site Area | Est. Number of New Homes |

| Jalan Tembusu | 2.8 | 1.96 | 645 |

| Lentor Hills Road (Parcel A) | 3.0 | 1.71 | 595 |

| Dairy Farm Walk | 2.1 | 1.56 | 385 |

| Bukit Batok West Ave. 8 (Executive Condominium) | 3.0 | 1.25 | 375 |

The estimated launch dates are from September of this year (October and December for the Dairy Farm and EC sites, respectively).

There are another six residential sites on the reserve list (these sites are only triggered if sufficient interest is shown by developers; which is quite likely in the given market).

The increased supply somewhat alleviates fears of another en-bloc fever in 2021. This was a looming issue, as most of the en-bloc properties from 2017 have already been developed and sold. Coupled with lower GLS supply in 2020, this was expected to set off a rush for collective sales, among land-starved developers.

Such an event would push up resale property prices, and ultimately have a knock-on effect on new launches too (because homeowners displaced by an en-bloc sale are cash-rich, and may seek a new launch condo as a replacement).

Stay calm and don’t rush to buy, just because prices are rising

While prices are going up, MAS has been clear that they’re monitoring the situation; it’s unlikely to overheat to the point where, if you can’t buy now, you’ll be priced out by the end of the year.

So be deliberate and make proper comparisons. If everything still seems too expensive right now, you may want to wait for the upcoming slew of more reasonably priced OCR projects; or focus your attention on further located resale properties (especially if you’re looking for larger homes).

Do follow us on Stacked so we can keep you updated, as the situation progresses. You can also check out our in-depth reviews on new and resale properties alike.

If you’d like to get in touch for a more in-depth consultation, you can do so here.