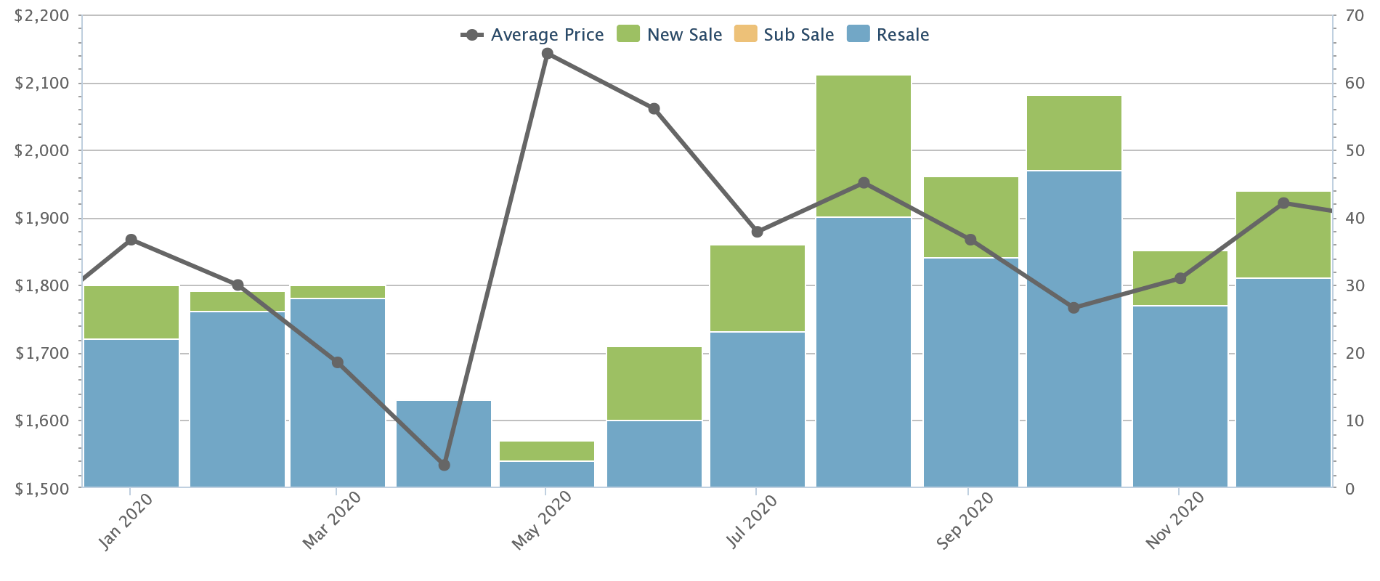

Following the results of Q4 2020, Core Central Region (CCR) condo sales and prices have been raising eyebrows. Prices appear to be up, despite expectations to the contrary: the rental market is still soft, and overall CCR condo prices had declined in the last quarter. As such, we may be seeing a surprise turnaround for prime region condos. Here’s what we can spot from the data, and word-on-the-ground:

CCR condos have reversed their price declines from earlier in 2020

Condo prices across the CCR saw a notable pick-up toward the end of 2020, especially coming from a weak third quarter. The following is according to Square Foot Research:

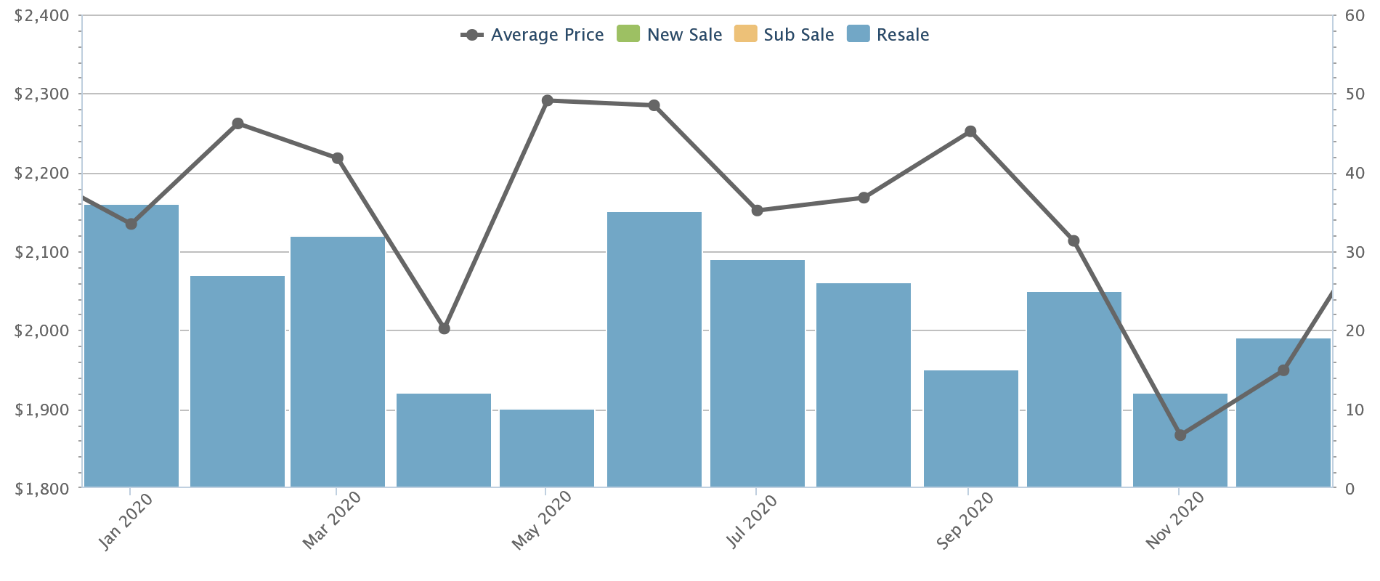

District 1 (Raffles Place, Boat Quay)

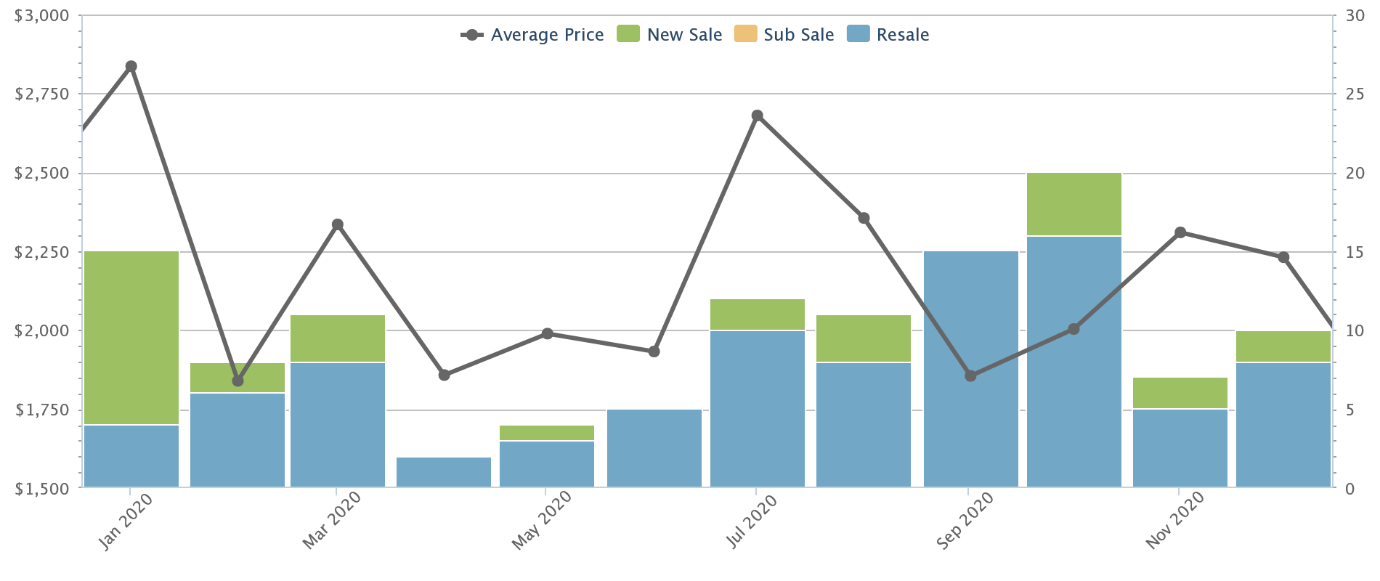

District 2 (Chinatown, Tanjong Pagar)

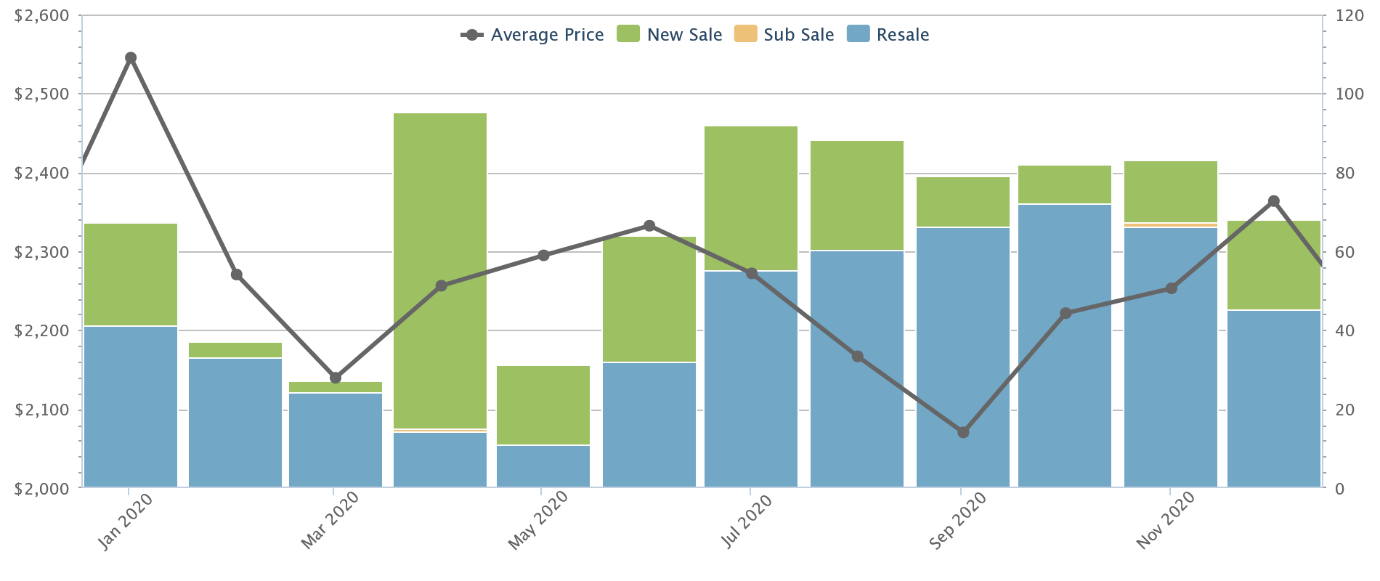

District 9 (Orchard, River Valley)

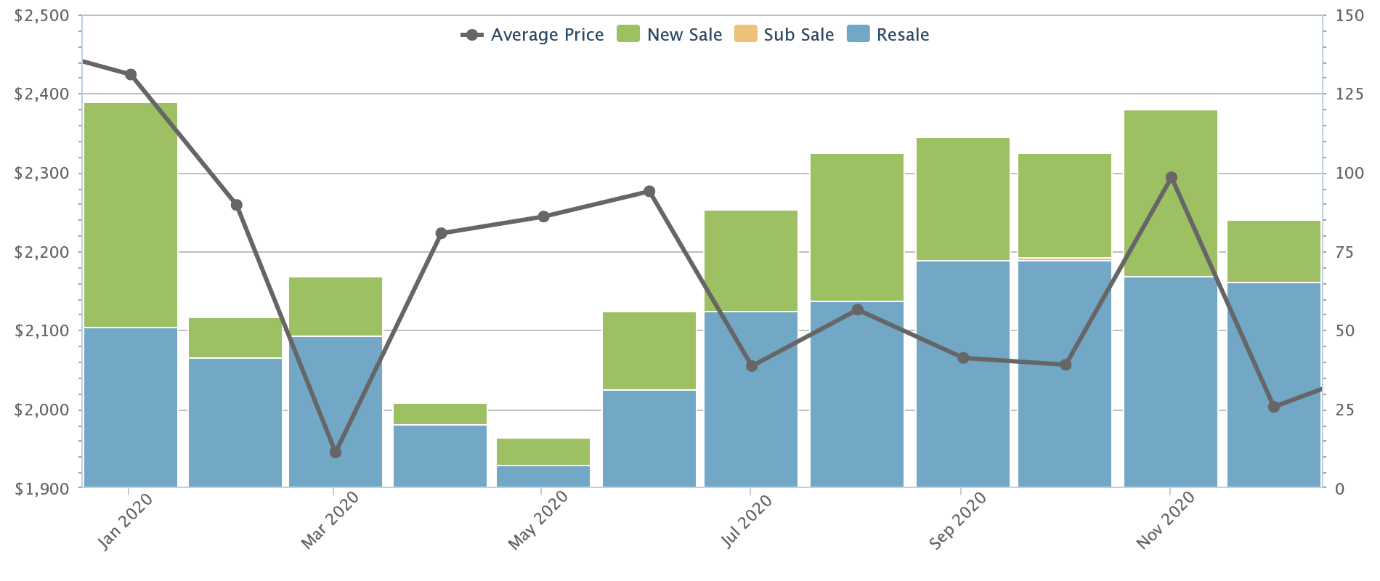

District 10 (Timah, Holland Village, Tanglin)

District 11 (Newton, Thomson)

(District 6 is excluded as there was only one transaction for all of 2020)

URA reports that, as a whole, non-landed private home prices rose 3.2 per cent in the CCR for Q4 2020. This is a near-complete reversal from the previous quarter, when CCR prices dipped 3.8 per cent.

By comparison, the overall private home market only saw prices rise about 2.1 per cent for Q4. This would make CCR and RCR condos (where prices rose 4.4 per cent) the main drivers of price increases for end-2020. An unexpected development, given that the Covid-19 economy was expected to drive buyers to lower-quantum OCR properties.

(This is also stoking fears of another round of cooling measures, to compensate. We have more on this in an earlier article).

Rental rates also improved in the CCR for Q4 2020, although the region is still the worst-hit

The downward momentum slowed for rentals of CCR condos in Q4, dropping by 1.2 per cent. In Q3, URA had recorded a fall of 2.1 per cent.

While this is a good sign, we note that CCR properties continue to bear the brunt of the soft rental market. For the whole of 2020, CCR condos have seen rentals fall by three per cent, whereas the RCR has seen rentals fall by 2.1 per cent, and the OCR has barely dipped 0.1 per cent.

For the CCR, this is likely due to a shift to remote working, which makes renting near the CBD unnecessary, and a lower number of expatriate workers as companies cut costs (notice that office rentals in the CBD have also been falling).

In addition, tenants tend to seek out cheaper alternatives during a downturn, especially if their jobs are affected. As such, it’s likely that mass-market properties in the OCR will stay at the top for the mid to near-term.

So what are some possible reasons for a turnaround in the CCR?

- Lower interest rates motivate investors

- Within a wider context, CCR prices are looking more attractive

- Increased demand for the luxury segment

- The belief of price resilience

1. Lower interest rates motivate investors

CCR properties have a higher proportion of pure investors, as opposed to owner-occupiers. At first glance, we would thus assume a weak rental market would push investors away from the CCR.

However, developments (both literal and metaphorical) have managed to defy this.

First, many new CCR condos in 2020, such as The M and Midtown Bay, sport a remarkably low quantum. The M condo, for instance, had units below $1 million at launch, despite a high price per square foot (sometimes touching $3,000 psf).

| Date | Size | Price (PSF) | Quantum |

| 21 Feb 2020 | 409 | $2,352 | $962,000 |

| 22 Feb 2020 | 409 | $2,400 | $981,600 |

| 22 Feb 2020 | 409 | $2,400 | $981,600 |

| 22 Feb 2020 | 409 | $2,400 | $981,600 |

| 22 Feb 2020 | 409 | $2,400 | $981,600 |

| 22 Feb 2020 | 409 | $2,400 | $981,600 |

| 22 Feb 2020 | 409 | $2,400 | $981,600 |

| 22 Feb 2020 | 409 | $2,400 | $981,600 |

| 22 Feb 2020 | 409 | $2,420 | $989,700 |

| 16 Jul 2020 | 409 | $2,426 | $992,200 |

| 22 Feb 2020 | 431 | $2,309 | $994,000 |

| 22 Feb 2020 | 431 | $2,319 | $998,300 |

Midtown Modern had units starting at just $1.3 million. This low quantum will help support rental yields, despite the soft rental market.

Second, interest rates are at a historic low following Covid-19, and will likely remain so till 2022 due to the United States Federal Reserve (low rates are a stimulus measure to support the US economy, which indirectly benefits SIBOR-linked home loans).

At present, home loan rates average 1.3 per cent; and at some points in the year, we spotted loan packages that were even at below one per cent. A low interest rate, coupled with a low quantum, can push up or sustain rental yields even in a weak market.

Investors are likely looking at the long term, and seeing the pandemic as a chance to seize CCR properties at a more reasonable price; which leads us to our next point:

2. Within a wider context, CCR prices are looking more attractive

While CCR prices saw a strong uptick in Q4, it’s worth noting their prices are quite muted over the whole of 2020.

In the report linked above, URA states that prices of non-landed properties in the CCR decreased by 0.4 per cent for the entire year, while prices in the RCR rose 4.7 per cent, and prices in the OCR rose 3.2 per cent.

In addition, the early part of 2020 saw multiple media outlets announcing the decline of CCR properties; in April 2020, for instance, it was noted that CCR condos were 7.2 per cent down from their last peak in 2013.

Coupled with the lack of price increases for the whole of 2020, investors may now hold the perception that CCR properties are at the bottom – and worth buying despite the Additional Buyers Stamp Duty (ABSD).

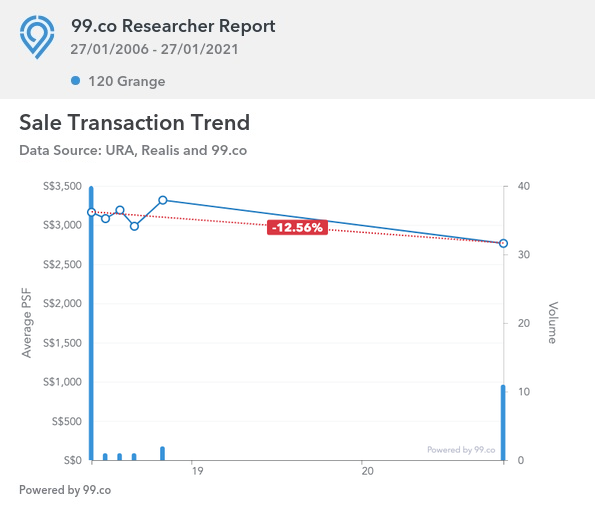

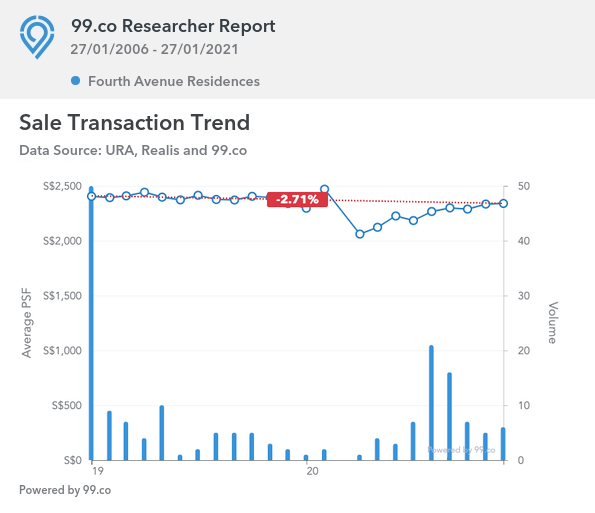

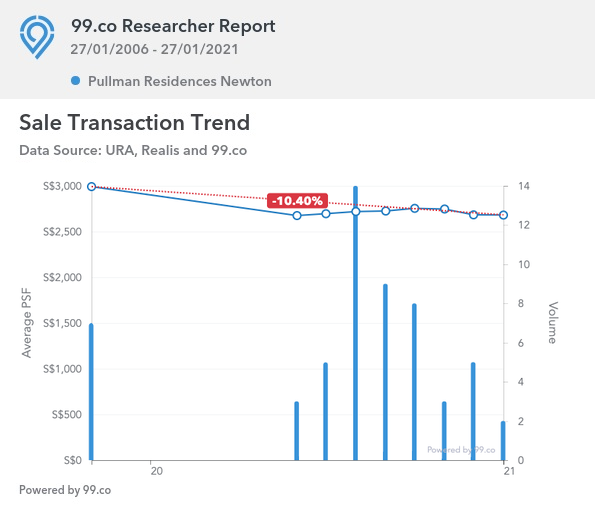

This can actually be seen as some CCR new launch condos have been dropping their prices to push for more sales (just to give you a few examples):

120 Grange

Prices at launch in June 2018 were at an average of $3,164 psf. This has dropped to an average of $2,766 psf in November 2020 to achieve a 100% sold status for 120 Grange.

Fourth Avenue Residences

At its launch in January 2019, 60 units were sold at an average of $2,414 psf at Fourth Avenue Residences. Currently in the past 2 months, this has dropped to an average of $2,317 psf.

Pullman Residences

When Pullman Residences was first launched in November 2019, it sold 7 units at an average price of $2,992 psf. Now in the past 2 months it has moved 9 units at an average price of $2,682 psf.

3. Increased demand for the luxury segment

2020 saw a spike in demand for luxury properties, most of which are located in the CCR.

In the first three quarters of 2020, for instance, there were 163 non-landed homes in the CCR that transacted at $5 million or above. 33 of these units were transacted at more than $10 million.

There are a number of reasons why this is happening, such as:

- Foreign buyers who are driven by external reasons (such as the weakening yuan, or Singapore looking more attractive due to political unrest in Hong Kong and tensions with Australia)

- Investors fleeing the stock market or low bond yields, and seeing high-end real estate as a safe haven

- The rising prominence of the Bugis area and Marina Bay, which are seen as the “new Orchard” by some investors, who want to get in early

For foreign buyers, the volatile global economy may be a stronger incentive than even our 20 per cent ABSD.

This is related to our next point:

4. The belief of price resilience

CCR properties have been marketed as “resilient” for time out of mind; among seasoned investors and long-time market watchers, this is grounds for a drawn-out debate (on par with the subject of freehold versus leasehold).

We won’t go into the pros and cons of that old argument here; suffice it to say that this belief has been ingrained into the Singapore private property market – and even into some foreign investors – over the course of decades.

Some of the key beliefs include:

- The demand for CCR properties is almost perpetual, as there’s no equal alternative to a location like Orchard or Anson Road

- CCR condos tend to be freehold as well as centrally located, and historically fetch better en-bloc prices

- Gains and yields are higher in the CCR in the long term (although the definition of “long term” has been quite varied in many of these arguments)

As such, it’s not surprising that the CCR continues to draw high-net worth individuals looking for the proverbial safe port; especially with Covid-19 being the defining crisis of the era.

Speaking to agents on the ground, the general impression is that interest in these properties are healthy – but we didn’t see a pick-up earlier in 2020, due to the Circuit Breaker and then worries about the wider economy. In addition, many buyers at the time were expecting sellers to lower prices, in a weak economy.

We do think that, barring new cooling measures, CCR condos will continue to push on in 2021; this is despite the soft rental market. Whether or not CCR condos are a good buy, at this time, is an altogether more complicated issue.

Do follow us on Stacked, so we can provide you with more individual analyses of the upcoming launches (CCR or otherwise).

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

0 Comments