2021 is shaping up to be as volatile as the year before. Covid-19 is still not a forgone conclusion, there’s talk of major construction delays, and prices are rising across the board (enough to perhaps justify new cooling measures). Whether you’re upgrading from your HDB flat, or just the opposite, it’s hard to guess if now’s the right time to sell. Here’s what to consider in the present day:

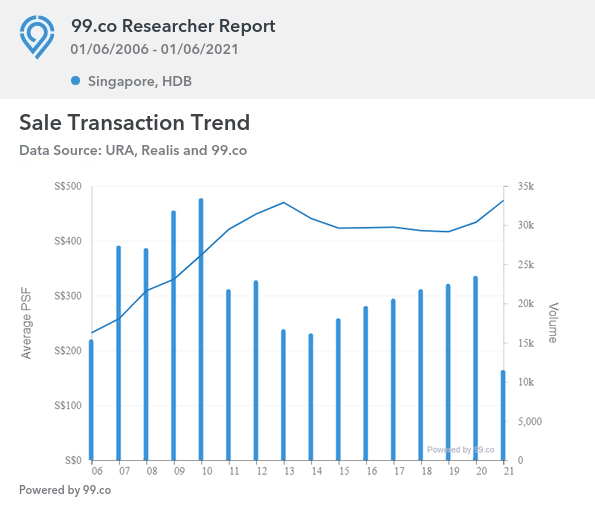

Resale flat prices have hit new heights in 2021

As of 1st June, resale flat prices across Singapore averaged $473 psf. Even during the last property peak, in 2013, we didn’t see the average go beyond $470.

In terms of quantum, the average resale flat price at the start of June was $497,152, or about 4.6 per cent higher than in 2013.

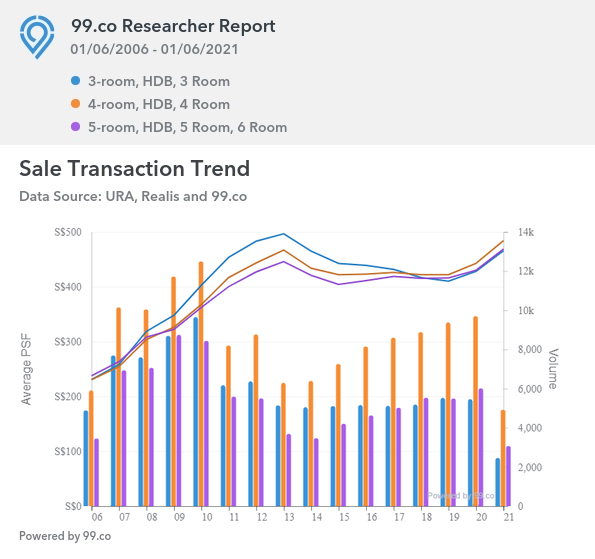

3-room, 4-room, and 5-room flats have all shown similar performance:

The average price for a 3-room flat was $465 psf, while 4-room flats averaged $484 psf. 5-room flats averaged $469 psf.

On top of this, we’ve seen a record-breaking number of flat transactions reach $1 million. There have already been 87 such transactions in the first five months of 2021, the most recent being a 5-room flat at Buona Vista Court for $1.2 million (May 2021).

As such, it’s no surprise that flat owners are being encouraged to “cash out” while the tide is high.

Sellers have an undeniable advantage right now. Covid-19 has caused labour and supply shortages, which have seen buyers turn to resale flats for fear of delays. Furthermore, Cash Over Valuation (COV) has been creeping back in since mid-2020. This is especially appealing to sellers since zero or negative COV had become the norm following policy tweaks in 2013 (At the time, HDB stopped publishing COV rates to keep resale prices manageable).

So in a broad sense, realtors are telling the truth, when they claim 2021 is a good year to sell and upgrade (or downgrade, if you want more for retirement). However, we’d encourage you to consider a few specifics before you sell:

- Private property prices have also risen

- If you’re downgrading, your replacement flat may cost more than you think

- You’re competing with quite a number of sellers

- Low interest rates don’t last forever

1. Private property prices have also risen

The ideal time to upgrade is not just when resale flat prices are rising; the ideal time would be when resale flat prices are rising, while private home prices are falling. But of course we know that isn’t going to happen in Singapore. Perhaps the best case scenario would just be a stagnant private residential market instead. Either way, this is not the situation in 2021.

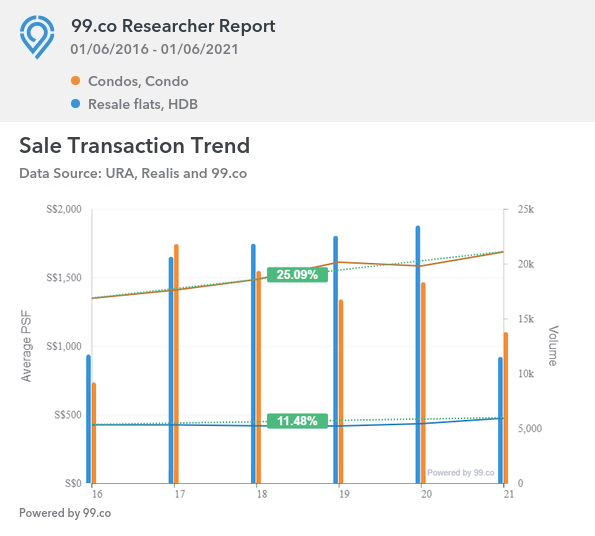

Despite the recent recovery in resale flat prices, private home prices still have them beat:

If we compare 1st June 2016 to 1st June this year, for example, we can see private (non-landed) home prices rose from $1,348 to $1,686 psf. This is up around 25 per cent, compared to an 11.5 per cent increase in resale flat prices over the same period.

So simply put, you may sell your flat for a lot more in 2021…but your new condo will cost more as well.

As such, upgraders should be careful that they can cover the price gap. Bear in mind that, when you sell your flat, you still need to refund the money used from CPF; this is with the accrued interest of 2.5 percent.

The minimum cash down for a private property is five percent of the purchase price. Assuming a typical quantum of $1.6 million today, you will need about $80,000 left in cash, after refunding your CPF.

From here, there are two arguments that can be made:

A salesperson will tell you this is even more reason to buy now, before the situation gets worse (the longer you wait, the higher private home prices might go; and the wider the price gap). This is possibly true.

A second argument is in favour of prudence. You could end up spending more than you expect for a condo; even after selling your flat. This isn’t a move that’s easy to undo (remember you need to hold the condo for at least three years, to be out of the Sellers Stamp Duty period). You also have to consider that, given how high private home prices have gone, you may be buying at a peak.

2. If you’re downgrading, your replacement flat may cost more than you think

Because resale flat prices are up, your next flat will also cost more; and you need to ensure the difference is still sufficient to meet retirement targets. For example, if you were to downgrade from a 4-room to a 3-room flat in Sengkang right now, the price difference between the two is just around $82,000.

(The average price of a 4-room flat in Sengkang is $450,000, while a 3-room averages $368,000. You can check out the current average prices by town on the HDB website).

Remember this difference is before you factor in costs such as renovating your new home and paying off your outstanding home loan. So if the cost of your smaller flat won’t ultimately meet your financial targets, you may want to question if it’s still worth downgrading right now – do you really want to be in a smaller home, while still falling short of your retirement goals?

Alternatively, you can drop us a message with your budget, and we’ll try help you find a unit at the right price.

3. You’re competing with quite a number of sellers

A record-number of flats reached MOP in 2020, and we’ll see a similar situation in 2021 (about 50,000 flats in total across both years). Demand has matched supply in the wider market, but the key term there is “wider”.

In specific neighbourhoods, sellers need to be wary of dozens of listings in their block or near it. Prices rises tend to be capped by the number of competing sellers nearby.

Realtors we spoke to also mentioned that, due to the number of “young” resale flats (i.e., flats that have just reached five-years old), older resale units may lose their lustre. One realtor, speaking on condition of anonymity, warned that:

“Buyers haven’t become less conscious of lease decay. They want to be able to move in quick; but they also don’t want a flat that’s too old, too difficult to resell later – because many are aiming to upgrade after MOP. So, when there are so many newer resale flats around, they tend to be shortlisted before the older ones. The only advantage is that the older flats are bigger.”

We have a list of 50 flats that will MOP in 2020 or 2021. If you have an older flat near these areas, you could have a tougher time getting your desired price.

Rarer HDB units however, such as maisonettes, may not be affected by this. Buyers of such units tend to be owner-occupiers rather than investors; and many of them intend to “live out” the rest of the lease.

4. Low interest rates don’t last forever

Current low interest rates (around 1.3 per cent per annum) make selling and upgrading seem like an attractive option. When the interest rate is around half your CPF interest rate, it can feel as if you’re “borrowing for free”.

However, it should be noted that the low interest rate is due to United Stated Federal Reserve’s stimulus measures; it’s meant to tide over Covid-19 troubles, until their economy recovers. After that, the interest rate will normalise again.

To be fair, we’ve seen that interest rates can remain low for a long time – the same move was made during the Global Financial Crisis in 2008/9; and home loan rates still hadn’t risen past an average of two per cent in 2019, preceding the pandemic.

Nonetheless, property is a long-term investment, and home owners need to focus on affordability further down the road. There’s also a risk, however small, of interest rates spiking on the back of a strong US recovery.

Overall, 2021 is a good time to sell and upgrade / downgrade for most flat owners; but not all.

It’s best not to be motivated purely by chasing profits. The Singapore property market is dynamic and difficult to time, and our government is interventionist – new policies can change the market literally overnight. Sellers should base their timing on their personal financial situation, more than the wider market. Any decision to sell should involve a financial professional (whoever you trust), using the property numbers provided by an experienced agent. You can contact us for that, and find out more news and updates on Stacked.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

0 Comments