Hi.

I am 65 years old and doing part time and probably fully retired next 2 years. My wife will be retired too in couple of years.

Currently staying in a 2 bedroom condo in Punggol (River Isle) with balanced mortgage loan of $350,000.

I had a rental income in my Sengkang executive flat which is fully paid.

We too had an terrace house fully paid in JB

That’s us for my weekend home or maybe retirement home.

1. One of my retirement planning is to retired in JB and come back to SG during the weekend. That will be reverse traffic way so it will not hinder traveling movement with the super jam at the causeway.

2. To continue to stay in my condo and renting out my Sengkang executive flat with rentals around $4k.

3. To sell by HDB and paid up my condo mortgages.

4. Selling off condo and move back to HDB

This will have more cash profit than selling my HDB as am using cash monthly mortgage to my condo.

5. Thought of buying the 2-room flexi but must sell of all my properties including overseas (JB) which I prefer not to do as I want to keep my Malaysia home.

6. We both combined total $200,000 cash and $20,000 in CPF.

What’s your advise and opinion of what best step to take and planning for my retirement.

(This is part of an ongoing series where we answer reader questions about the property market. If you have one of your own, send it to stories@stackedhomes.com.)

Hi there,

Thank you for reaching out.

Given the recent interest in the RTS link to Johor Bahru, you are certainly well-positioned to enjoy that should/when it comes to fruition in the future.

We will start by looking at the amount of sales proceeds you will receive if you were to sell your properties.

The challenge for many buyers today isn't access to information.

It's interpreting that information in a way that makes sense for their finances, goals, and stage of life.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

Selling

Let’s first look at the recent 2-bedroom transactions in River Isles.

| Date | Size | PSF | Price | Level |

| Mar 2023 | 753 | $1,354 | $1,020,000 | #11 |

| Jan 2023 | 753 | $1,229 | $925,888 | #05 |

From January till date, there were just 2 transactions done and they were sold at an average price of $972,944. Assuming this to be the selling price:

| Description | Amount |

| Selling price | $972,944 |

| Outstanding loan | $350,000 |

| Sales proceeds (CPF + Cash) | $622,944 |

Since we do not know what HDB you own, we will look at all the Executive Apartments and Maisonettes in Sengkang. These are some of the recent transactions:

| Date | Block | Street | Level | Size and unit type | Price |

| Nov 2023 | 306B | Anchorvale Link | 04 to 06 | 128.00 Apartment | $683,000 |

| Nov 2023 | 310A | Anchorvale Rd | 13 to 15 | 126.00 Premium Apartment | $735,000 |

| Nov 2023 | 250C | Compassvale St | 07 to 09 | 131.00 Apartment | $775,000 |

| Nov 2023 | 298A | Compassvale St | 07 to 09 | 134.00 Premium Apartment | $730,000 |

| Nov 2023 | 116B | Rivervale Dr | 04 to 06 | 130.00 Apartment | $700,000 |

| Nov 2023 | 189C | Rivervale Dr | 13 to 15 | 131.00 Apartment | $755,000 |

| Nov 2023 | 103 | Rivervale Walk | 10 to 12 | 145.00 Maisonette | $880,000 |

| Nov 2023 | 122B | Sengkang East Way | 04 to 06 | 131.00 Apartment | $730,000 |

From January till date, there have been 92 executive units that changed hands in Sengkang at an average price of $740,187.

Since you’ve mentioned that you wish to keep the property in JB, we will not touch on that.

Now let’s look at how the 2 properties are performing.

Performance of both properties

| Year | Avg PSF (resale) | YoY | Property Price Index of Residential Properties (PPI) | YoY |

| 2016 | $820 | – | 137.2 | – |

| 2017 | $915 | 11.59% | 138.7 | 1.09% |

| 2018 | $974 | 6.45% | 149.6 | 7.86% |

| 2019 | $973 | -0.10% | 153.6 | 2.67% |

| 2020 | $989 | 1.64% | 157 | 2.21% |

| 2021 | $1,043 | 5.46% | 173.6 | 10.57% |

| 2022 | $1,126 | 7.96% | 188.6 | 8.64% |

| Annualised | – | 5.43% | – | 5.45% |

Since River Isles only obtained its Temporary Occupation Permit (TOP) in 2015, resale units only started coming on the market in 2016. From the table, it is clear that over the last 6 years, prices at River Isles are more or less moving in line with the overall market and have a similar growth rate.

| Project | Property type | Lease start year | TOP | Avg PSF (2023) |

| The Terrace | EC | 2013 | 2017 | $1,282 |

| The Amore | EC | 2013 | 2016 | $1,237 |

| River Isles | Condominium | 2012 | 2015 | $1,246 |

| Flo Residence | Condominium | 2011 | 2016 | $1,240 |

| Riverparc Residence | EC | 2010 | 2014 | $1,276 |

Looking at the neighbouring developments, we can see that River Isles is one of the newer projects in the area, although they are all relatively close in age. Its average price PSF falls in the mid-range among the five projects.

Notably, one advantage it holds is its condominium status, allowing unrestricted sales to any type of buyer. In contrast, The Terrace and The Amore which are not yet fully privatised, currently have limitations restricting sales to Singaporeans and Permanent Residents (PRs).

Considering this comparison and given the project’s relatively young age, coupled with the imminent commencement of operations at the Punggol Digital District scheduled for 2024, it’s probable that property prices at River Isles will hold up in the short to medium term.

Now let’s look at how executive flats in Sengkang have been performing.

| Year | Avg PSF (Resale) | YoY | HDB Resale Price Index (RPI) – Q1 of each year | YoY |

| 2012 | $430 | – | 138.5 | – |

| 2013 | $444 | 3.26% | 148.6 | 7.29% |

| 2014 | $420 | -5.41% | 143.5 | -3.43% |

| 2015 | $398 | -5.24% | 135.6 | -5.51% |

| 2016 | $389 | -2.26% | 134.7 | -0.66% |

| 2017 | $390 | 0.26% | 133.9 | -0.59% |

| 2018 | $395 | 1.28% | 131.6 | -1.72% |

| 2019 | $404 | 2.28% | 131 | -0.46% |

| 2020 | $399 | -1.24% | 131.5 | 0.38% |

| 2021 | $438 | 9.77% | 142.2 | 8.14% |

| 2022 | $489 | 11.64% | 159.5 | 12.17% |

| Annualised | – | 1.29% | – | 1.42% |

We can see here that prices of executive flats are also moving in line with the overall HDB market albeit slightly slower. Given that these executive units were completed from 1998 – 2003, they are some of the youngest executive flats available. Although 20 – 25 years isn’t exactly old, if you do hold on for an extended period of time, there may be lease decay concerns for potential buyers down the road.

Now that we have a better understanding of how your properties are performing, let’s run through the various options you’re contemplating.

Option 1. Retire in JB

Since you did not specify what you’d do with your local properties if you were to move to JB, there are three possible pathways you can consider: sell both, keep the HDB and sell the condo, or sell the HDB and keep the condo.

Let’s explore each of these in greater detail.

1a. Sell both properties

This option represents the most straightforward approach. Should you decide to sell both properties, the total sales proceeds would amount to approximately $1,363,131 ($622,944 from River Isles + $740,187 from the flat). These proceeds include both CPF funds (if utilised) and cash.

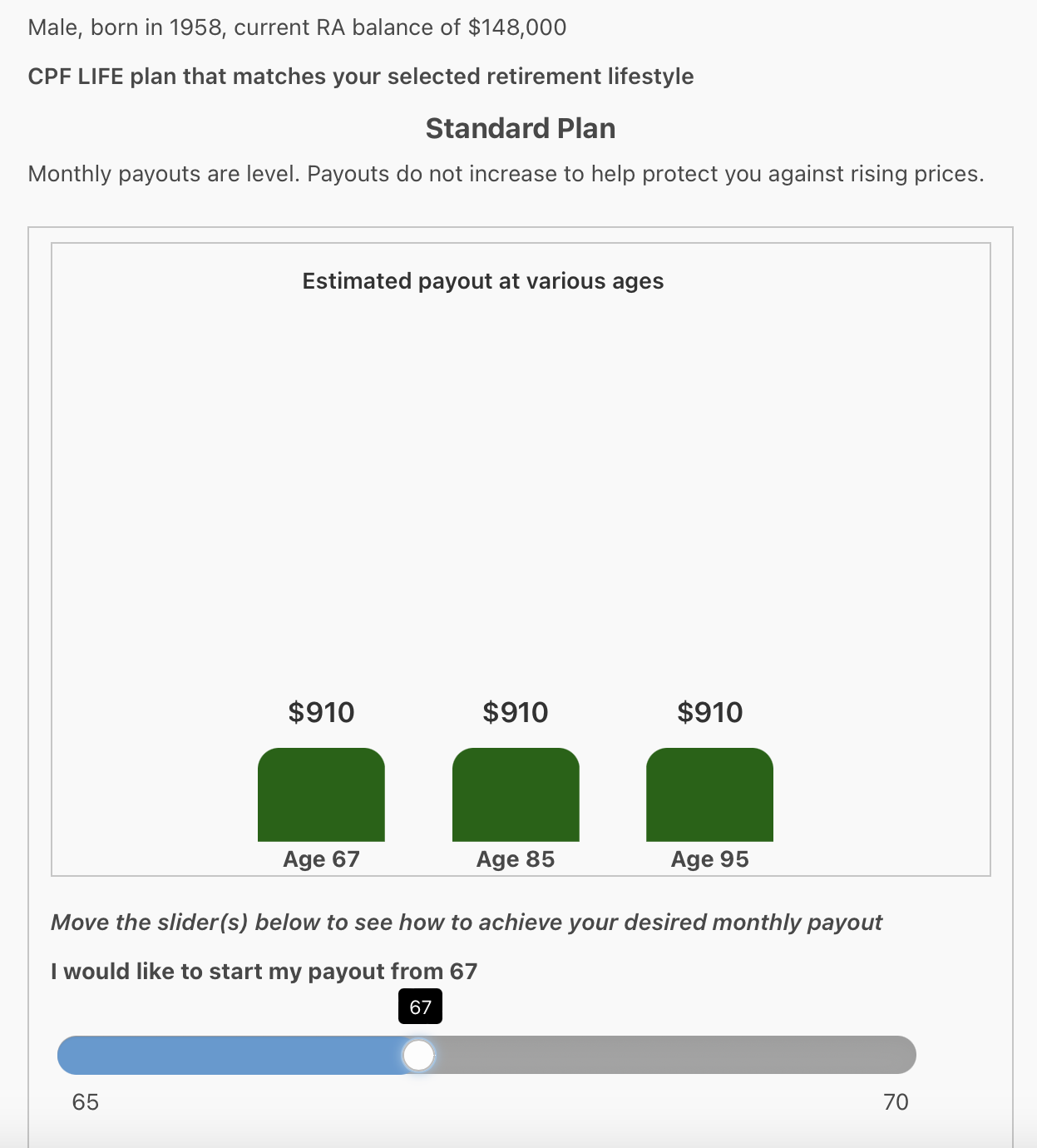

Assuming both you and your wife are aged 65, the required CPF Full Retirement Sum (FRS) stands at $148,000. If this has been met, any excess funds can be withdrawn as cash.

As a couple, you’ll need to allocate $296,000 towards your FRS. Considering your combined CPF funds currently stand at $200,000, we’ll subtract an additional $96,000 from the sales proceeds. Consequently, this leaves you with $1,267,131 in cash.

By adding your existing cash savings of $200,000, the total sums up to $1,467,131.

This is a substantial amount of retirement funds, especially if you plan to reside in JB, considering the advantageous current exchange rate favouring the SGD as well as the lower cost of living compared to Singapore.

Moreover, as you are presently 65, you will be eligible for CPF Life payouts. Considering your anticipated full retirement in about 2 years, assuming you commence payouts at 67 years old, the following represents the monthly payout based on the FRS of $148,000, under the Standard Plan:

Since you are planning for your retirement, we will look at the amount of retirement funds each option will provide you with.

Retirement funds:

| Description | Amount |

| Total cash on hand | $1,467,131 (Sales proceeds from both properties + Existing cash savings – RA top up) |

| Monthly funds | $1,820 ($910 CPF payout x2) |

1b. Sell just one and rent out the other for passive income

The property you choose to retain is likely to be held for the long haul with no intention of selling it. In such a scenario, and if there’s no specific legacy planning in consideration, concerns regarding lease decay won’t be a priority. Thus, retaining the HDB might present a preferable option, given that HDB rental yields commonly surpass those of private properties. Additionally, since the property has been fully paid off, there is no need to utilise rental income to offset monthly mortgage expenses.

Let’s take a look at how much passive income renting out the HDB can give you. For calculation purposes, we will use a 10-year timeframe.

| Description | Amount |

| Rental income (Assuming $3,450/month) | $414,000 |

| Property tax | $58,880 |

| Town council service & conservancy fees (Assuming $99/month) | $11,880 |

| Agency fees (Payable once every 2 years) | $18,630 |

| Total gains | $324,690 |

* To be more conservative, we have used the Q3 2023 average rent for executive flats in Sengkang

Retirement funds:

| Description | Amount |

| Total cash on hand | $726,944 (Sales proceeds from River Isles + Existing cash savings – RA top up) |

| Monthly funds | $5,270 ($3,450 rent + $910 CPF payout x2) |

We can see here that although the amount of cash on hand is lower than if you were to sell both properties, you would have a higher amount of monthly funds.

1c. Sell HDB and rent out River Isles

Finally, we’ll also look at the alternative of selling your HDB and keeping River Isles.

Since the specifics regarding your remaining loan tenure are undisclosed, and considering you’ve already reached 65 years of age, it indicates that either your wife is younger than you are or you secured a loan structured with a lower Loan-to-Value (LTV) ratio that permits borrowing beyond the age of 65. For calculation purposes, we’ll presume a remaining loan tenure of 5 years at a 4% interest rate.

Based on rental transactions from Q3 this year, the average rent for a 2-bedder In River Isles is $3,400 per month.

| Description | Amount |

| Interest expense | $36,747 |

| Rental income (Assuming $3,400/month) | $408,000 |

| Property tax | $57,600 |

| Maintenance fees (Assuming $250/month) | $30,000 |

| Agency fees (Payable once every 2 years) | $18,360 |

| Total gains | $265,293 |

Retirement funds:

| Description | Amount |

| Total cash on hand | $844,187 (Sales proceeds from HDB + Existing cash savings – RA top up) |

| Monthly funds (For 5 years until the loan is fully paid) | -$1,547 ($910 CPF payout x2 + $3,400 rent – $6,767 River Isles monthly cost) |

| Monthly funds (After the loan is fully paid) | $5,220 ($3,400 rent + $910 CPF payout x2) |

We can see here that this pathway offers more cash on hand but in the 5 years before the loan is paid up, your monthly funds will be negative (in 5 years this amounts to -$92,820). If we were to deduct this from your cash on hand of $844,187, the cash remaining would be $751,367 which is slightly more than if you were to sell River Isles and keep the HDB.

Given that River Isles is still a relatively young development, there could still be potential for growth. With this option, there is the potential of warning from both the rental income as well as capital appreciation if you do decide to sell River Isles down the road.

Option 2. Remain status quo

Let’s take a look at the costs incurred over a 10-year period.

Costs incurred from holding River Isles:

| Description | Amount |

| Interest expense | $36,747 |

| Property tax | $8,480 |

| Maintenance fees (Assuming $250/month) | $30,000 |

| Total costs | $75,227 |

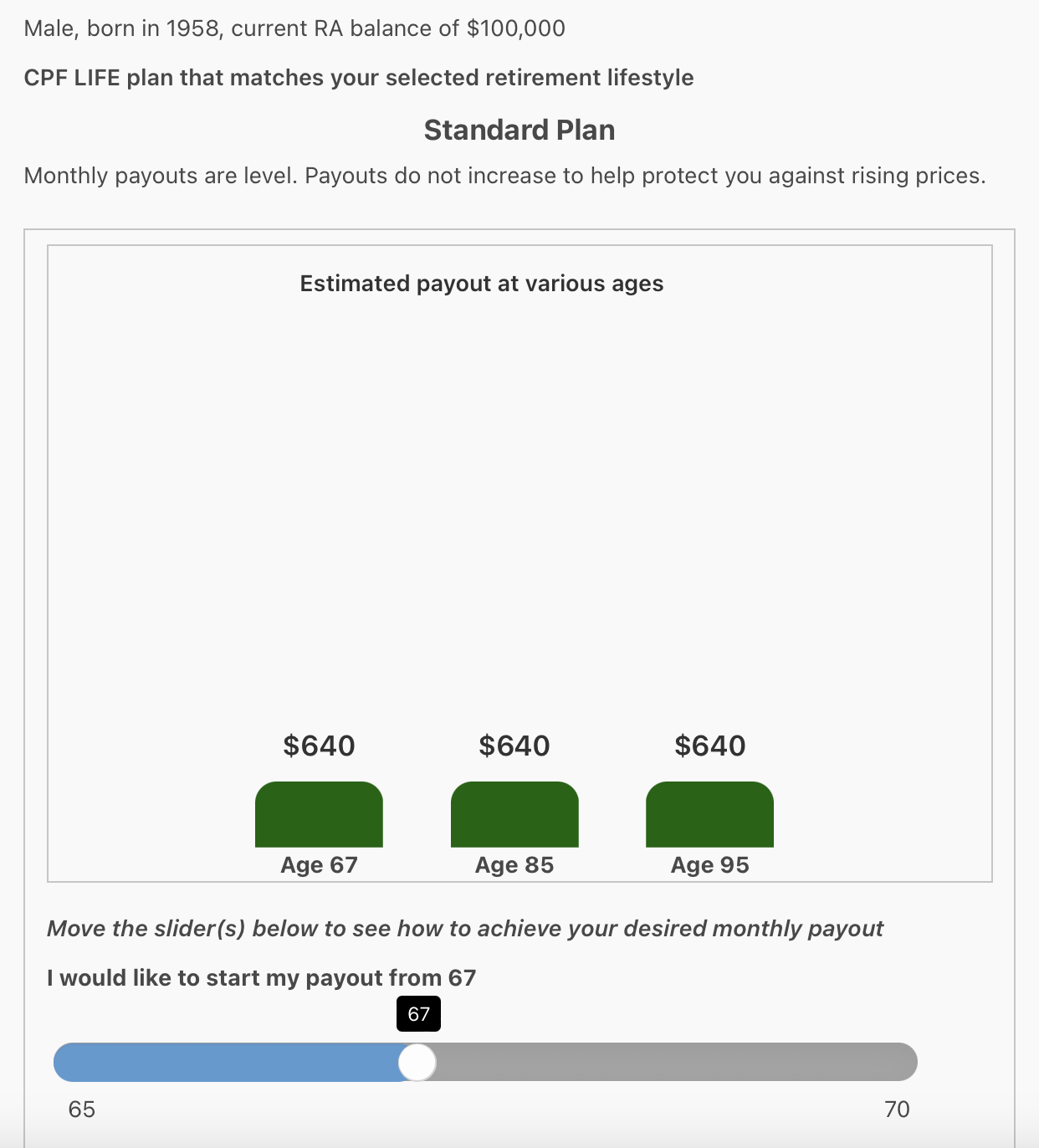

As you won’t be liquidating either of your properties with this option, you will not have additional funds to top up your CPF RA and it’s uncertain whether you’ve reached the FRS. Assuming an equal split of the current $200,000 in your CPF accounts between you and your wife, at age 67, this represents the projected payout you’ll receive:

Retirement funds:

| Description | Amount |

| Total cash on hand | $200,000 (Existing cash savings) |

| Monthly funds (For 5 years until the loan is fully paid) | -$2,037 ($640 CPF payout x2 + $3,450 rent – $6,767 River Isles monthly cost) |

| Monthly funds (After the loan is fully paid) | $4,409 ($640 CPF payout x2 + $3,450 rent – $321 River Isles monthly cost) |

Option 3. Sell HDB and pay off condo mortgage

Considering the prevailing elevated interest rates and your cash-based monthly mortgage payments, this could cause financial strain if you aim to retire completely in two years. Thus, settling the mortgage might be a wise decision, but let’s delve into the figures.

As before, let’s look at the costs incurred over a 10-year period should you take this pathway.

| Description | Amount |

| Sales proceeds from HDB | $740,187 |

| Outstanding loan for River Isles | $350,000 |

| Top up for RAs to meet FRS | $96,000 |

| Sales proceeds remaining | $294,187 |

Costs incurred from holding River Isles:

| Description | Amount |

| Property tax | $8,480 |

| Maintenance fees (Assuming $250/month) | $30,000 |

| Total costs | $38,480 |

Since you will top up your RAs to meet the FRS, the monthly CPF Life payout will be at $730.

Retirement funds:

| Description | Amount |

| Total cash on hand | $494,187 (Sales proceeds from HDB + Existing cash savings – RA top up) |

| Monthly funds | $1,499 ($910 CPF payout x2 – $321 River Isles monthly cost) |

Option 4. Sell condo and move into HDB

As previously noted in Option 1, if you have no plans to liquidate the property down the road or if you haven’t outlined any legacy plans, retaining the HDB might be a more favourable choice due to reduced expenses given it has been fully paid.

Costs incurred from holding the HDB:

| Description | Amount |

| Property tax | $5,680 |

| Town council service & conservancy fees (Assuming $99/month) | $11,880 |

| Total costs | $17,560 |

As before, since you will top up your RAs to meet the FRS, the monthly CPF Life payout will be at $730.

Retirement funds:

| Description | Amount |

| Total cash on hand | $726,944 (Sales proceeds from HDB + Existing cash savings – RA top up) |

| Monthly funds | $1,674 ($910 CPF payout x2 – $146 HDB monthly cost) |

As you’ve mentioned that your preference is to keep the property in JB, we will not touch on the purchase of a 2-room Flexi unit since that would mean having to dispose of the property.

What should you do?

Let’s do a quick summary of the retirement funds you’ll have for the various options:

| Option 1a. Retire in JB (Sell both properties) | Option 1b. Retire in JB (Sell River Isles and keep HDB to rent out) | Option 1c. Retire in JB (Sell HDB and keep River Isles to rent out) | Option 2. Remain status quo | Option 3. Sell HDB and pay off condo mortgage | Option 4. Sell condo and move into HDB | |

| Total cash on hand | $1,467,131 | $726,944 | $844,187 | $200,000 | $494,187 | $726,944 |

| Properties owned | 1 | 2 | 2 | 3 | 2 | 2 |

| Monthly funds | $1,820 | $5,270 | -$1,547 (Before loan is paid up) $5,220 (After loan is paid up) | -$2,037 (Before loan is paid up) $4,409 (After loan is paid up) | $1,499 | $1,674 |

Upon reviewing the options, it’s apparent that Option 1a, involving the sale of both properties and relocating to JB, offers the highest amount of cash on hand, while Option 2, maintaining the status quo, results in the least amount of cash on hand.

Among the four options, only Option 1 fully optimises all three properties by residing in the JB property and either liquidating the other two or keeping one for rental income. The remaining three options retain the JB property solely as a holiday home, lacking any income generation or profit prospects.

The advantage of owning multiple properties lies in the potential to either cash out or generate passive income during retirement.

Considering these factors, Option 1 seems to be the most ideal if frequent travel between JB and Singapore is feasible. This option additionally benefits from the SGD-MYR exchange rate, prolonging your retirement funds.

However, it’s important to note that retaining one property allows the flexibility of returning to Singapore if desired and may offer a sense of security, which we believe would be a more prudent choice.

We’ve heard of cases where Malaysia’s immigration could become aware that you’re border hopping often, and at some point, you may even face a ban from entering the country. While we don’t know if this would happen, there’s always a chance – so unless you have some sort of visa to stay, relying on the JB home as your sole residence is risky.

However, if you can secure a future staying in JB, then you can explore alternative investment avenues for your cash surplus which could further extend the longevity of these funds or increase your monthly cash flow.

Assuming you invest at a 5% ROI annually based on DBS’s historical average yields of Singapore REITs, here’s the monthly cash payout, on average, that you’ll see:

| Option 1a. Retire in JB (Sell both properties) | Option 1b. Retire in JB (Sell River Isles and keep HDB to rent out) | Option 1c. Retire in JB (Sell HDB and keep River Isles to rent out) | Option 2. Remain status quo | Option 3. Sell HDB and pay off condo mortgage | Option 4. Sell condo and move into HDB | |

| Total cash on hand | $1,467,131 | $726,944 | $844,187 | $200,000 | $494,187 | $726,944 |

| Cash to invest | $1,367,131 | $626,944 | $744,187 | $100,000 | $394,187 | $626,944 |

| 5% ROI annually | $68,357 ($5,696/month) | $31,547 ($2,629/month) | $37,209 ($3,101/month) | $5,000 ($417/month) | $19,709 ($1,642/month) | $31,347 ($2,612/month) |

| Investment Returns + Monthly Funds | $7,516 | $7,899 | $1,554 (Before loan is paid up) $8,321 (After loan is paid up) | -$1,620 (Before loan is paid up) $4,826 (After loan is paid up) | $3,141 | $4,286 |

Of course, you won’t be able to invest everything, so this is really a ceiling on what you can get. You should adjust the amount of cash you wish to set aside based on your needs and expectations.

The decision of whether to sell both properties or retain one for rental purposes hinges on your preferences. Undoubtedly, selling both properties would increase your available cash and payout.

After all, your tastes and preferences may change in the future.

Featured Image by Ven Jiun (Greg) Chee

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

0 Comments