Hi team at stackedhomes,

Help! We need advise!

My husband and I just got married early this year and are looking to buy either a HDB or condo.

Some things to note here would be.

- I just sold my condo in August 2023 and we understand to buy a resale HDB we would need to wait 15 months.

- We both have a combined income of 15,700 sgd.

- Total savings combined cash would be 350k, combined cpf 220k.

- My husband likes freehold and east side condos but we are not sure if it is worth spending at least 1.8m on a 3 bedder unit.

- We hope to have kids in the future. We are looking at capital appreciation and proximity to amenities, especially MRT.

With the rising interest rate, would it be best to

- purchase a resale HDB with minimum 3 bedrooms?

- appeal for an HDB BTO or sale of balance flat?

- or resale condo with minimum 3 bedrooms?

- do freehold condos actually make a difference?

Condos/HDBs in the East, Bidadari or Central would be ideal.

Thank you for reading and hope to gain some advise!

Kind regards

Both 35 years old

Just to add on we saw a unit in sunhaven and there is an ideal 3 bedroom unit. This is a freehold unit. MCST is about 432.

But we aren’t sure if sunhaven is a place to commit too.

(This is part of an ongoing series where we answer reader questions about the property market. If you have one of your own, send it to stories@stackedhomes.com.)

Hello,

As you have correctly noted, opting for an HDB purchase at this point would impose a 15-month wait-out period, which might pose challenges if you don’t have alternative accommodation available.

Conversely, purchasing a private property doesn’t involve any waiting period. Whether the tenure of a property makes a difference also hinges on your intended holding period, which we will delve into further in our reply.

Let’s begin by examining your affordability.

The challenge for many buyers today isn't access to information.

It's interpreting that information in a way that makes sense for their finances, goals, and stage of life.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

Affordability

Combined affordability (HDB purchase)

| Description | Amount |

| Maximum loan based on ages of 35 with a combined monthly income of $15,700, at 4.6% interest* | $838,789 (25-year tenure) |

| CPF funds | $220,000 |

| Cash | $350,000 |

| Total loan + CPF + cash | $1,408,789 |

| BSD based on $1,408,789 | $40,951 |

| Estimated affordability | $1,367,838 |

*As your combined income is above $14,000, you will not be eligible to take up an HDB loan

Combined affordability (Private property purchase)

| Description | Amount |

| Maximum loan based on ages of 35 with a combined monthly income of $15,700, at 4.6% interest | $1,684,404 (30-year tenure) |

| CPF funds | $220,000 |

| Cash | $350,000 |

| Total loan + CPF + cash | $2,254,404 |

| BSD based on $2,254,404 | $82,320 |

| Estimated affordability | $2,172,084 |

While the notion of purchasing two properties wasn’t raised, let’s evaluate your individual affordability to explore this prospect. Our assumption will involve the partner with the higher income buying the private property and allocating a greater portion of cash toward this purchase.

Partner 1 (HDB purchase)

| Description | Amount |

| Maximum loan based on age of 35 with a monthly income of $5,700, at 4.6% interest | $304,529 (25-year tenure) |

| CPF funds | $170,000 |

| Cash | $50,000 |

| Total loan + CPF + cash | $524,529 |

| BSD based on $524,529 | $10,335 |

| Estimated affordability | $514,194 |

*As your combined income is above $14,000, you will not be eligible to take up an HDB loan

Partner 2 (Private property purchase – 5 years later)

| Description | Amount |

| Maximum loan based on age of 40 with a monthly income of $10,000, at 4.6% interest | $979,478 (25-year tenure) |

| CPF funds | $50,000 |

| Cash | $300,000 |

| Total loan + CPF + cash | $1,329,478 |

| BSD based on $1,329,478 | $37,779 |

| Estimated affordability | $1,291,699 |

Let’s now look at the options you’re considering.

Potential pathways

Option 1. Buy a resale HDB

As you’ve mentioned, since you’ve just sold your condo, buying an HDB would entail a 15-month wait out period which could be costly if you do not have an alternative accommodation.

So while the capital appreciation of a resale HDB might not match that of a BTO, the potential CPF Housing Grants can partially compensate for this shortfall. Unfortunately, your combined income surpasses the $14,000 threshold, rendering you eligible only for the Proximity Housing Grant (PHG) if you buy a place within 4km of either of your parents’ residences. Additionally, in the current high-interest rate environment, an HDB loan which has a lower interest rate compared to the banks is not feasible due to your income exceeding the stipulated limit.

Hence, it seems that you may not fully maximise the benefits associated with purchasing an HDB flat.

That said with a budget of $1.3M, securing a flat in your preferred location is certainly feasible. Let’s jump into the potential costs and gains considering this option, presuming a 10-year timeframe since you’ve mentioned wanting to start a family, and also the availability of an existing accommodation during the 15-month wait out period.

These are the average HDB resale prices for 4 and 5-room flats in the various towns in the Central and Eastern parts of Singapore:

| Towns | 4-Room | 5-Room |

| Ang Mo Kio | $538,000 | $725,500 |

| Bedok | $523,000 | $684,000 |

| Bishan | $715,000 | $929,000 |

| Bukit Merah | $860,000 | $928,000 |

| Kallang/Whampoa | $790,400 | $907,900 |

| Pasir Ris | $554,000 | $658,000 |

| Queenstown | $928,000 | * |

| Tampines | $569,000 | $678,000 |

| Toa Payoh | $780,000 | $900,000 |

For the sake of discussion, let’s use the highest price of $929,000 as the purchase price.

| Description | Amount |

| Purchase price | $929,000 |

| BSD | $22,470 |

| CPF + cash | $570,000 |

| Loan required | $381,470 |

Cost incurred

| Description | Amount |

| BSD | $22,470 |

| Interest expenses (Assuming 3% interest) | $97,556 |

| Property tax | $7,950 |

| Town council service & conservancy fees (Assuming $90/month) | $10,800 |

| Total costs | $138,776 |

Potential gains

We will do a simple projection based on the growth rate of HDBs over the past decade at 1.42%.

| Time period | Price | Gains |

| Starting point | $929,000 | $0 |

| Year 1 | $942,192 | $13,192 |

| Year 2 | $955,571 | $26,571 |

| Year 3 | $969,140 | $40,140 |

| Year 4 | $982,902 | $53,902 |

| Year 5 | $996,859 | $67,859 |

| Year 6 | $1,011,014 | $82,014 |

| Year 7 | $1,025,371 | $96,371 |

| Year 8 | $1,039,931 | $110,931 |

| Year 9 | $1,054,698 | $125,698 |

| Year 10 | $1,069,675 | $140,675 |

Potential gains if you were to take this pathway: $140,675 – $138,776 = $1,899

Option 2. Appeal for BTO or SBF

Assessment for appeals typically occurs on a case-by-case basis, making it challenging to predict the likelihood of success. However, if approval is granted, BTOs entail a lengthier waiting period of 30 months.

Considering your emphasis on capital appreciation, opting for a BTO may involve a trade-off in terms of opportunity costs due to the extensive waiting period: a 30-month wait out coupled with 3-4 years of construction time. Without alternative accommodation, rental expenses during this period could outweigh any potential gains.

Additionally, if you choose a flat under the Prime Location Public Housing (PLH) scheme, the Minimum Occupation Period (MOP) will extend to 10 years (which is double the standard). Furthermore, there is a clause for subsidy recovery upon selling these PLH flats which involves returning a portion of the resale price to HDB.

Looking at the latest BTO launch in October, the prices for 4-room flats in the Central and Eastern regions commenced from $480,000 to $537,000.

For our calculations, let’s consider a unit priced at $580,000, presuming you have temporary accommodation during the interim period.

| Description | Amount |

| Purchase price | $580,000 |

| BSD | $12,000 |

| CPF + cash | $570,000 |

| Loan required | $22,000 |

Depending on the price of the property, you may not even have to take up a loan. Most major banks in Singapore have a minimum loan amount of $100,000 – $200,000. Since you will only have to pay the balance of the purchase price (minus the option fee) when you collect your keys, you will likely have sufficient time to save up the $22,000. So for this calculation, let’sl assume that no loan is taken.

Cost incurred

| Description | Amount |

| BSD | $12,000 |

| Property tax | $3,760 |

| Town council service & conservancy fees (Assuming $90/month) | $10,800 |

| Total costs | $26,560 |

We previously wrote an article discussing BTO profits and found that the majority of BTOs made at least 50% gains when they sell within 2 years from meeting the MOP. Let’s assume this to be the case here.

| Time period | Price | Gains |

| Starting point | $580,000 | $0 |

| Year 10 | $870,000 | $290,000 |

Potential gains if you were to take this pathway: $290,000 – $26,560 = $263,440

Option 3. Buy a resale condo

Let’s first address your question about the distinction between purchasing freehold or leasehold property. It’s hard to say which is better if you are looking at a capital appreciation perspective, as it really depends on the property in question.

But if you really had to narrow it down, this distinction often hinges on your holding period. As a general rule of thumb, if you’re considering a property for long-term ownership, opting for a freehold property typically presents a more favourable choice due to the absence of lease decay, contributing to better potential value retention.

Let’s take a look at how freehold and leasehold projects that were completed in 2000 have performed to date.

| Year | Freehold Avg PSF (Resale) | YoY | Leasehold Avg PSF (Resale) | YoY |

| 2000 | $458.9 | |||

| 2001 | $673.9 | 46.86% | $633.2 | |

| 2002 | $690.8 | 2.50% | $511.7 | -19.19% |

| 2003 | $584.9 | -15.34% | $490.6 | -4.13% |

| 2004 | $574.6 | -1.76% | $441.1 | -10.08% |

| 2005 | $618.1 | 7.57% | $424.4 | -3.80% |

| 2006 | $756.1 | 22.33% | $470.4 | 10.84% |

| 2007 | $960.6 | 27.05% | $589.1 | 25.25% |

| 2008 | $840.5 | -12.51% | $612.5 | 3.97% |

| 2009 | $810.0 | -3.63% | $638.5 | 4.25% |

| 2010 | $974.6 | 20.32% | $714.1 | 11.83% |

| 2011 | $1,119.8 | 14.90% | $839.4 | 17.55% |

| 2012 | $1,096.9 | -2.04% | $905.7 | 7.90% |

| 2013 | $1,241.1 | 13.15% | $966.2 | 6.69% |

| 2014 | $1,180.6 | -4.88% | $898.6 | -7.00% |

| 2015 | $1,133.9 | -3.96% | $873.4 | -2.81% |

| 2016 | $1,119.5 | -1.27% | $880.5 | 0.81% |

| 2017 | $1,148.5 | 2.59% | $873.2 | -0.83% |

| 2018 | $1,234.1 | 7.45% | $898.9 | 2.95% |

| 2019 | $1,236.3 | 0.18% | $932.6 | 3.74% |

| 2020 | $1,258.1 | 1.76% | $895.5 | -3.98% |

| 2021 | $1,343.2 | 6.76% | $965.1 | 7.77% |

| 2022 | $1,526.8 | 13.67% | $1,136.6 | 17.77% |

| Freehold | Leasehold | |

| Annualised growth rate at 5th year (we used 2001 – 2006 since there were no leasehold transactions in 2000) | 2.33% | -5.77% |

| Annualised growth rate at 10th year (2001 – 2011) | 5.21% | 2.86% |

| Annualised growth rate at 20th year (2001 – 2021) | 3.51% | 2.13% |

The disparity in growth rates may fluctuate based on the specific years reviewed and the distinct developments. Ironically, the longer the duration, the lesser the disparity which goes in contrast with what we assumed.

However, based on the data provided, it’s evident that freehold properties generally outperform leasehold properties over a prolonged duration. Therefore, the choice between buying a freehold or leasehold property can be contingent on your intended holding period.

With a budget of $2.17M, these are some available freehold 3-bedders in the Central and Eastern regions that are currently on the market:

| Project | District | Tenure | TOP | Size (sqft) | Asking price |

| Beacon Heights | 12 | 999-years | 2012 | 1,109 | $1,880,000 |

| Edelweiss Park Condo | 17 | Freehold | 2006 | 1,270 | $1,350,000 |

| Ava Towers | 12 | Freehold | 1993 | 1,227 | $1,900,000 |

Do note that these developments are picked out purely because they fall within your affordability and match your requirements. They may or may not be suitable for you so we strongly advise that you consult a property agent for further analysis.

Assuming you were to purchase the unit at Beacon Heights, let’s take a look at the potential costs and gains. From January till date, there has only been one transaction for a unit with a similar size and it was sold in July at $1,680,000. We will use this as the purchase price for our calculation.

| Description | Amount |

| Purchase price | $1,680,000 |

| BSD | $53,600 |

| CPF + cash | $570,000 |

| Loan required | $1,163,600 |

Cost incurred

| Description | Amount |

| BSD | $53,600 |

| Interest expenses (Assuming an interest rate of 4%) | $403,767 |

| Property tax | $25,200 |

| Maintenance fees (Assuming $400/month) | $48,000 |

| Total costs | $530,567 |

Potential gains

We will do a simple projection based on the growth rate of private properties over the past decade at 2.21%.

| Time period | Price | Gains |

| Starting point | $1,680,000 | $0 |

| Year 1 | $1,717,128 | $37,128 |

| Year 2 | $1,755,077 | $75,077 |

| Year 3 | $1,793,864 | $113,864 |

| Year 4 | $1,833,508 | $153,508 |

| Year 5 | $1,874,029 | $194,029 |

| Year 6 | $1,915,445 | $235,445 |

| Year 7 | $1,957,776 | $277,776 |

| Year 8 | $2,001,043 | $321,043 |

| Year 9 | $2,045,266 | $365,266 |

| Year 10 | $2,090,466 | $410,466 |

Potential gains if you were to take this pathway: $410,466 – $530,567 = -$120,101

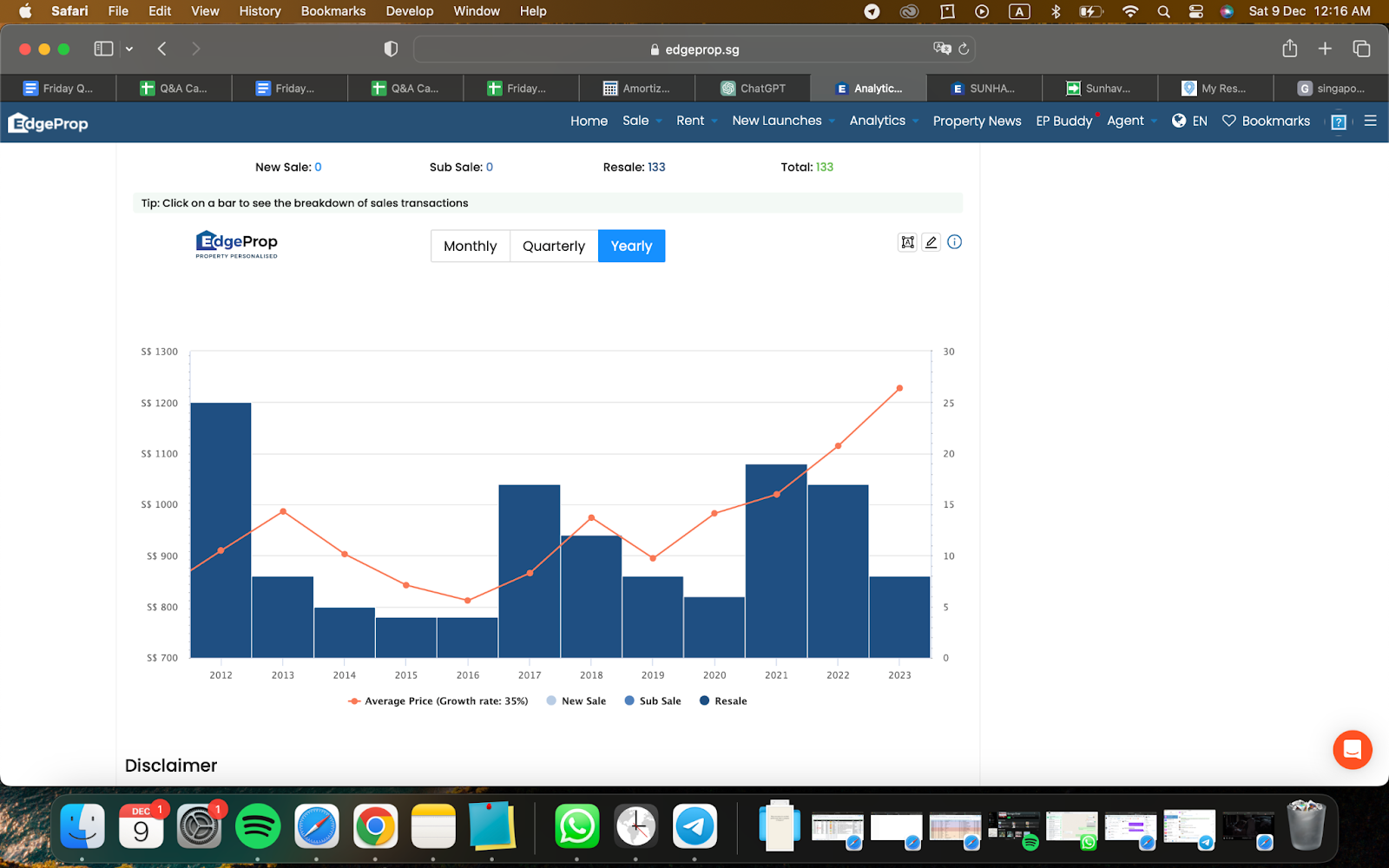

Since you’ve highlighted your interest in a unit at Sunhaven, let’s take a quick look at how the project has been doing.

Performance of Sunhaven

| Year | Sunhaven avg PSF (resale) | YoY | Property Price Index (PPI) of Residential Properties | YoY |

| 2012 | $910 | – | 151.5 | – |

| 2013 | $987 | 8.46% | 153.2 | 1.12% |

| 2014 | $903 | -8.51% | 147.0 | -4.05% |

| 2015 | $842 | -6.76% | 141.6 | -3.67% |

| 2016 | $812 | -3.56% | 137.2 | -3.11% |

| 2017 | $866 | 6.65% | 138.7 | 1.09% |

| 2018 | $974 | 12.47% | 149.6 | 7.86% |

| 2019 | $895 | -8.11% | 153.6 | 2.67% |

| 2020 | $983 | 9.83% | 157.0 | 2.21% |

| 2021 | $1,020 | 3.76% | 173.6 | 10.57% |

| 2022 | $1,115 | 9.31% | 188.6 | 8.64% |

| Annualised | – | 2.05% | – | 2.21% |

It’s clear from the above table that prices at Sunhaven are moving in line with the overall private property market over the last 10 years. Looking at the graph, we can also see that there is a healthy number of transactions annually which is an important contributing factor to the appreciation of a project.

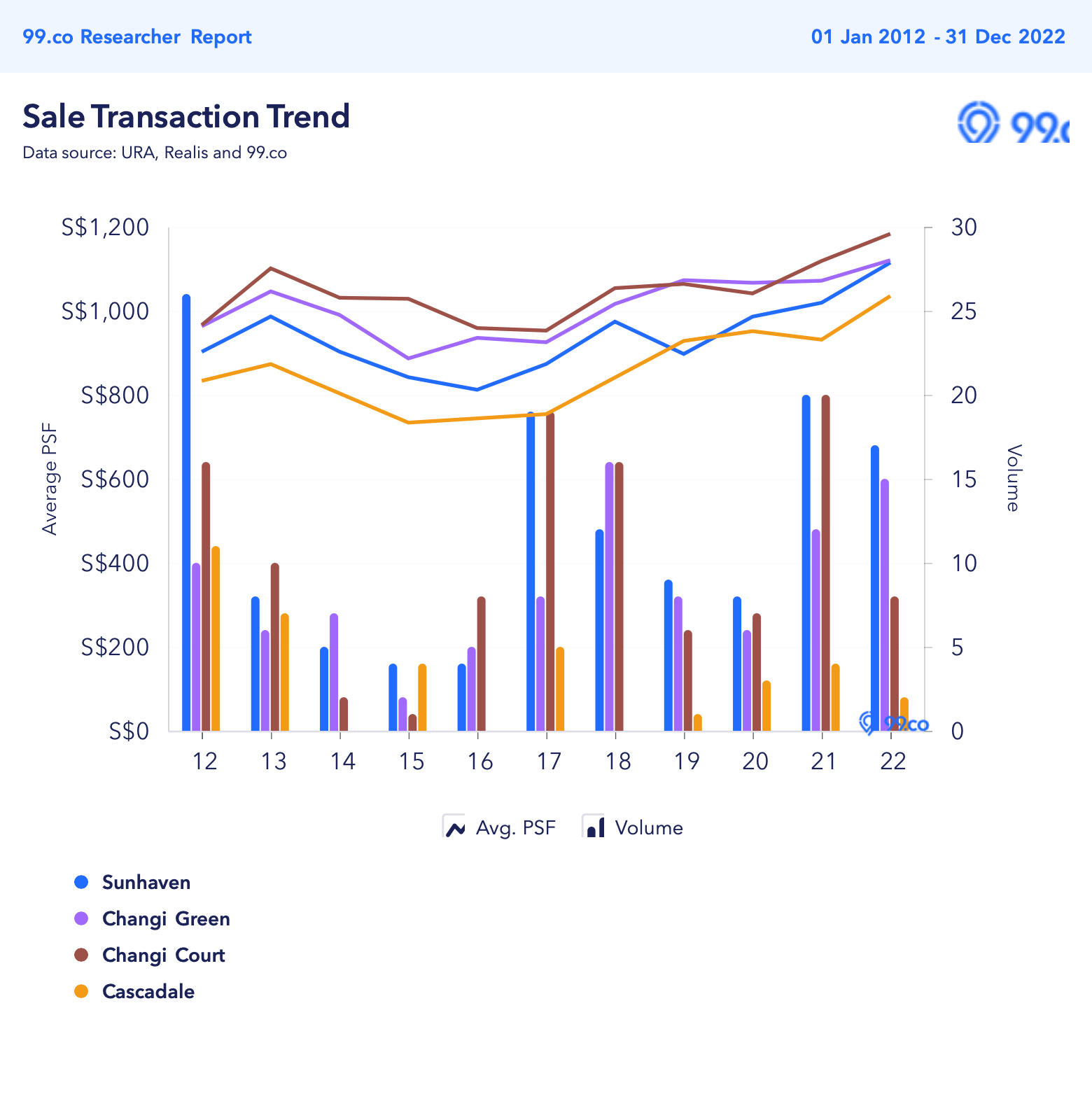

Let’s now take a look at some of Sunhaven’s competitors.

Freehold developments in the vicinity

| Project | Tenure | TOP | No. of units | Avg PSF |

| Sunhaven | Freehold | 2003 | 295 | $1,115 |

| Changi Green | Freehold | 2001 | 256 | $1,120 |

| Changi Court | Freehold | 1997 | 297 | $1,183 |

| Cascadale | Freehold | 1994 | 134 | $1.35 |

Among the neighbouring freehold developments, Sunhaven stands as the most recent project. In spite of this, its average price PSF is among the lowest. Comparatively, in terms of project size, it is similar to Changi Green and Changi Court, both of which boast higher average price PSF.

One potential rationale for this discrepancy could be attributed to its distance from the MRT station, as Sunhaven is the farthest among the four projects. Nevertheless, it is still a mere 15-minute walk from the Upper Changi MRT station, which some people would still consider to be within reasonable walking distance.

Notably, Sunhaven demonstrates consistent transaction volumes in comparison to the other developments, indicating a healthy level of demand.

So from the surface numbers, it’s reasonable to anticipate that prices at Sunhaven are likely to remain stable.

Alternative option

Given your emphasis on capital appreciation, an alternate route worth considering is to first procure an HDB under the owner-occupier scheme. Subsequently, the occupier can proceed to acquire a private property for investment after fulfilling the MOP for the HDB. This approach facilitates the separation of your primary residence and investment property, offering more flexibility should the investment property become profitable.

Regrettably, despite purchasing under the owner-occupier scheme, HDB evaluates your combined household income for eligibility for an HDB loan and CPF Housing Grants. As such, these benefits remain inaccessible to you.

With a budget of $514,000, your choices for a 4 or 5-room flat in the Central and Eastern regions might be constrained to older properties. In this scenario, we’ve allocated just $50,000 in cash for the purchase. However, considering you have time to accumulate savings for the investment property, you might opt to allocate more cash toward the HDB purchase to expand your budget and options. Nonetheless, for the sake of calculation, let’s assume a purchase price of $514,000.

| Description | Amount |

| Purchase price | $514,000 |

| BSD | $10,020 |

| CPF + cash | $220,000 |

| Loan required | $304,020 |

Cost incurred

| Description | Amount |

| BSD | $10,020 |

| Interest expenses (Assuming interest rate of 4%) | $105,494 |

| Property tax | $2,970 |

| Town council service & conservancy fees (Assuming $90/month) | $10,800 |

| Total costs | $129,284 |

Potential gains

We will do a simple projection based on the growth rate of HDBs over the past decade at 1.42%.

| Time period | Price | Gains |

| Starting point | $514,000 | $0 |

| Year 1 | $521,299 | $7,299 |

| Year 2 | $528,701 | $14,701 |

| Year 3 | $536,209 | $22,209 |

| Year 4 | $543,823 | $29,823 |

| Year 5 | $551,545 | $37,545 |

| Year 6 | $559,377 | $45,377 |

| Year 7 | $567,320 | $53,320 |

| Year 8 | $575,376 | $61,376 |

| Year 9 | $583,547 | $69,547 |

| Year 10 | $591,833 | $77,833 |

Total gains for the HDB: $77,833 – $129,284 = -$51,451

Regarding the investment property, let’s assume that Partner 2 purchases a private property at the maximum budget of $1.29M in five years. As current market options may not be relevant in the future, we won’t delve into present choices. For calculation purposes, a rental yield of 3% will be employed. As we are looking at a 10-year timeframe, we will use a 5-year holding period for the investment property.

| Description | Amount |

| Purchase price | $1,290,000 |

| BSD | $36,200 |

| CPF + cash | $350,000 |

| Loan required | $976,200 |

Cost incurred

| Description | Amount |

| BSD | $36,200 |

| Interest expenses (Assuming interest rate of 4%) | $183,280 |

| Rental income | $193,500 |

| Agency fees (Payable once every 2 years) | $10,449 |

| Property tax | $26,700 |

| Maintenance fees (Assuming $250/month) | $15,000 |

| Total costs | $78,129 |

Potential gains

We will do a simple projection based on the growth rate of private properties over the past decade at 2.21%.

| Time period | Price | Gains |

| Starting point | $1,290,000 | $0 |

| Year 1 | $1,318,509 | $28,509 |

| Year 2 | $1,347,648 | $57,648 |

| Year 3 | $1,377,431 | $87,431 |

| Year 4 | $1,407,872 | $117,872 |

| Year 5 | $1,438,986 | $148,986 |

Total gains for the private property: $148,986 – $78,129 = $70,857

Total gains if you were to take this pathway: $70,857 – $51,451 = $19,406

What should you do?

Let’s do a quick summary of all the 4 options:

| Option 1. Buy a resale HDB | Option 2. Appeal for a BTO or SBF | Option 3. Buy a resale condo | Alternative option. Buy an HDB under the owner-occupier scheme and buy an investment property 5 years later | |

| Costs incurred in 10 years | $138,776 | $26,560 | $530,567 | $207,413 |

| Potential gains | $1,899 | $263,440 | -$120,101 | $19,406 |

The table clearly indicates that Option 2, which involves buying a BTO or SBF, potentially offers the highest returns. However, the approval for such an appeal is uncertain. Additionally, there’s a considerable waiting period involved – a 30-month wait out and 3 – 4 years of construction time. In our calculations, we assumed that alternative accommodation is available, but if that’s not the case, the incurred costs will notably diminish the potential gains.

The subsequent favourable choice is procuring an HDB under the owner-occupier scheme and investing in another property five years later. This approach allows you to own two properties, dividing between your personal residence and investment, thereby diversifying risks. Rental income from the investment property can offset some outgoings, reducing overall costs.

Opting for a resale HDB might not be ideal if capital appreciation is a prime concern, given the tighter regulations in the HDB market. Comparatively, private properties generally display better performance than HDBs.

It’s important to note that the above three options involve a wait-out period of 15 – 30 months, incurring substantial costs if alternative accommodation is unavailable.

Choosing a resale condo eliminates any waiting time, but in our calculations, it appears to result in negative gains due to increased loans and prevailing elevated interest rates (and if it remains high over 10 years although it’s not likely). However, considering capital appreciation, private properties typically hold better potential if chosen wisely. So this is naturally very much dependent on choosing the right property.

Considering the prolonged wait and MOP restrictions associated with BTOs, selling the property might take almost a decade or longer. Therefore, this pathway seems less favourable.

In contrast, the alternative option of initially purchasing an HDB under the owner-occupier scheme and acquiring an investment property five years later appears promising. It provides the opportunity to eventually own two properties and offers more time to accumulate savings for a broader selection of investment options.

Additionally, you could use this time to wait out the property market and high interest rates. Of course, this is timing the market, so there’s no guarantee that you would benefit from the wait here. However, we think that if you are fine with owning an HDB first for your own stay reasons, then this option seems to be a more suitable one at this point.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

4 Comments

Wow, this is completely useless advice and such a bad way of comparing the different options.

There are so many things wrong with the analysis but just to highlight a few – each option has a completely different risk profile to be a meaningful comparison, there are too many general assumptions about capital appreciation growth rates, overly simplistic analysis about potential gains vs cost…

And the conclusion about freehold being better than leasehold just because freehold appreciates at a higher rate (duh) is wrong – you are forgetting that a leasehold property will be significantly cheaper (15-20% cheaper) than a freehold property with identical attributes. The initial outlay saved from purchasing a leasehold property can similarly be invested and the gains from that will need to be taken into account when comparing the leasehold vs freehold option. Hence the conclusion is not as black and white as portrayed in the response above.

Hope that stackedhomes can improve the quality of its responses. I can guarantee you that the asker will be more confused after reading your response.

Hi, we need some advice too. Please may i know whuch email address to send to. Thank you so much.

To my knowledge, this couple, with their combined income of > 14k, would not be eligible for BTO or SBF at all. As you correctly pointed out, they can still get resale HDB with bank loan. So the BTO discussion seems like a moot point altogether!