For most Singaporeans, owning multiple properties is a classic “shake leg and collect money” scenario. This week, however, we talked to Jasmine (she prefers to exclude her surname), who explains how it’s anything but.

In her 40s, Jasmine owns three condo units – a three-bedder and two compact units. These are all rented out, while she lives elsewhere with her husband and in-laws. She recently shared with us the strangest things she has faced renting out so many units; from having a tenant peeing in the sink, to balancing the books.

Acquiring the three condos

Jasmine bought her first property in 2009, at the age of just 32. It was not an easy decision, as it meant having to sell her existing business. She says:

“I was quite torn at the time, as I knew property was the way to go but I lacked the capital. When one of my cousins heard about it, he offered to buy over my existing business.

But I had started my business – mainly software for point-of-sales systems – with my husband. It was hard to get him to agree, as that business meant around 10 years of blood, sweat, and tears. And it was a scary decision, to risk between a successful business and the property market.”

Selling the business would also mean Jasmine would go back to work as a regular employee in the family business; it was not a prospect she relished as “it felt like it could be a step back, as that’s where I started my working life.”

Jasmine’s husband was not happy with the decision either. “I was on the verge of giving it up,” she says, “when there was a big dispute with a client, and my husband had a change of heart; I think he got fed up with dealing with these issues.

If it hadn’t been for that unreasonable customer, I would never have ended up buying the first condo!”

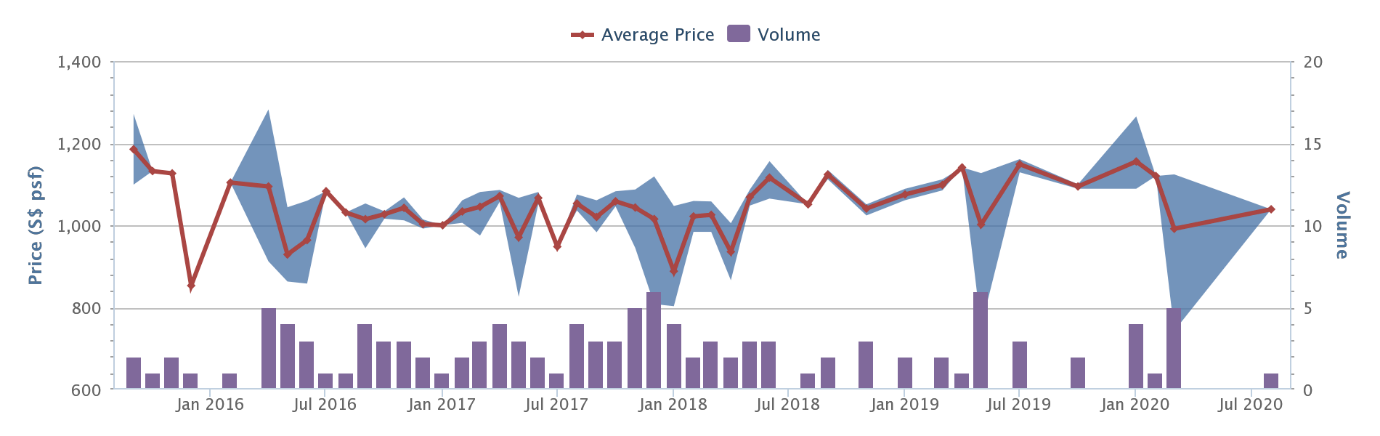

The first condo that Jasmine bought was a three-bedder in Double Bay Residences.

This is a 99-year leasehold property in Simei, in District 18.

“At the time the price was just around $620 per square foot,” Jasmine says, “Which I feel was one of the better deals around as it was within walking distance of Simei MRT. I also do not plan to hold this property for more than 10 to 15 years, so I did not want to pay the premium for freehold.”

We did a quick check on Double Bay Residences:

At present, prices at Double Bay Residences average $1,039 psf. This is roughly a 67.6 per cent increase from $620 psf, or an annualised return of about 4.8 per cent (excluding rental income) since 2009.

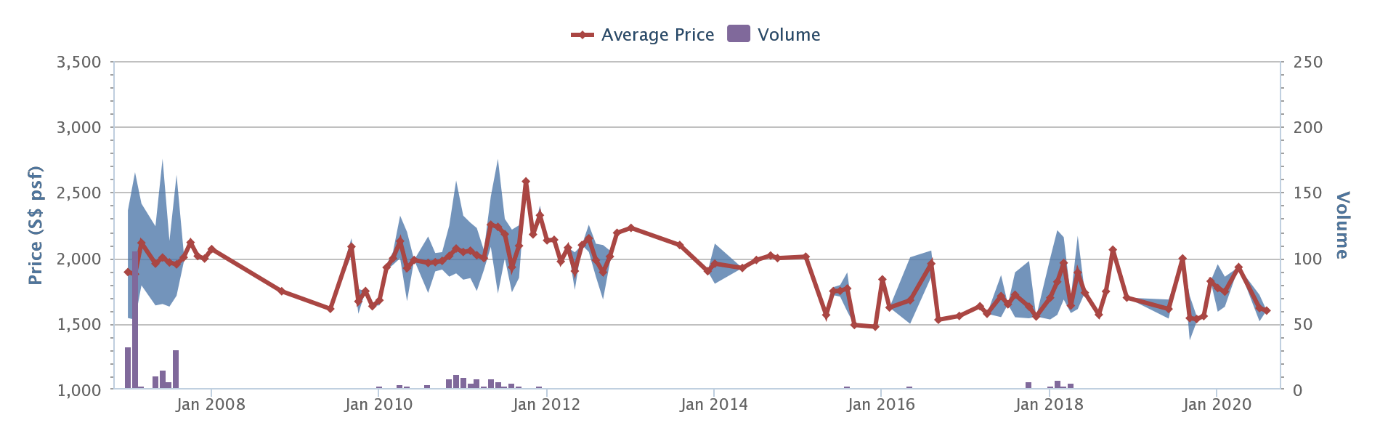

Jasmine’s initial intent was to live in Double Bay Residences, and then purchase a second, smaller unit to rent out. So shortly after in 2010, she bought a resale unit at One Shenton. This was around $1,800 psf at the time.

(Note: there was no Additional Buyers Stamp Duty in 2010).

Prices at One Shenton only average $1,601 at present however, so it would have been an annualised return of about – 1.16 per cent since she bought it (excluding rental income).

“I let urgency get the better of me,” Jasmine said, “As the owner was eager to offload it and I was worried someone else would beat me to it. But maybe it’s lucky since the ABSD was instituted shortly after.”

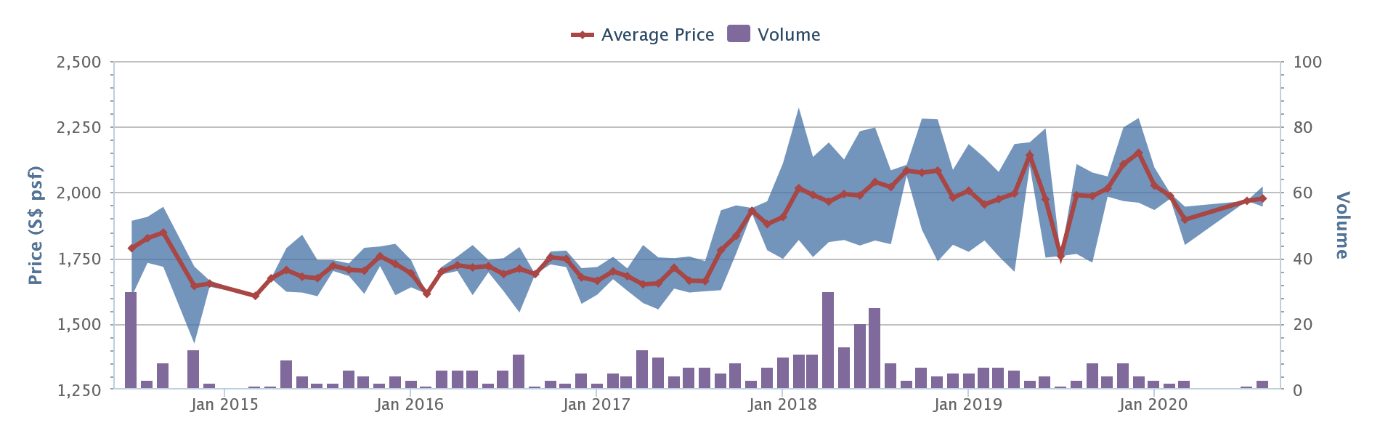

The third property was purchased after ABSD, in 2014. This was at The Crest, but it was purchased entirely under her husband (this meant there was no ABSD payable).

“At that point we actually moved in with our in-laws, and made the decision to rent out all the properties. The Crest was tempting to us because it was relaunched with lower prices.”

(A lot of the old news has been lost with time, but we understand the Crest was initially launched in June 2014, then relaunched at adjusted prices in October 2014).

The one-bedder at the Crest was bought at $1,680 psf. The current average is $1,941 psf. This is an increase of about 15.5 per cent, or an annualised return of 2.4 per cent over six years (excluding rental).

Why always leasehold?

Jasmine shared that her philosophy, from the beginning, is to stick to leasehold properties:

“My objective is to get the best yield, and then resell in maybe in 10 to 15 years. So I just focus on the location and rentability, and I try to make sure the condo is not too old. Freehold incurs a premium that doesn’t really benefit me, as I’m not going to wait for en-bloc sales or hold all the way.”

(Jasmine is referring to the premium of about 10 to 15 per cent on freehold units, compared to leasehold counterparts).

What is it like to maintain the books on three condos?

Jasmine says the largest of the three condos takes more work:

“There are three separate tenants, all working expatriates, and I need to track rent separately. There’s also some mediation needed, because the tenants spilt the utility bills – so when it’s too high, sometimes there will be private complaints that one tenant uses up the lion’s share of water and light. In future I would like to just have one family living there, it makes everything much simpler.”

One of the things that helps though, is the simplified tax deductions for Singapore landlords:

“For rental expenses, you can claim 15 per cent of gross rent as tax deductions. This is super convenient I feel, as you don’t need to collect all the separate bills and invoices when you make repairs.”

(Note: At Stacked, our suggestion is that landlords track the different rental expenses anyway; just in case the costs end up being more than the flat 15 per cent you can claim. But this is not always possible for landlords like Jasmine, who are time-strapped).

The biggest thing to watch for, however, are unexpected maintenance fees. This can even include accommodation.

“There was a situation where the circuit board actually caught fire and the power went out,” Jasmine said, “It cost me about $4,200 to repair. Even worse, it took two days to fix. I had to compensate the tenant for temporary accommodation during those two days – she was a student and it was exactly before her exams, so how can she study without electricity? There’s no choice.”

For these reasons, Jasmine has saved up and maintains a reserve of about $10,000, for any such situations. It’s protected her cash flow in multiple situations over the years.

Keeping the costs low

Jasmine says her approach is to “renovate with an eye for functionality, not aesthetics.” A key thing to remember is that the longer your inventory list, the more items you need to monitor.

She also says that:

“Expect damage to happen. If you use wallpaper or tiles where the design is no longer produced, what happens if one part gets damaged? You either have to live with the mismatch, or you need to replace the whole thing. So it’s best to keep everything as generic as possible.”

In terms of the mortgage, Jasmine tries to keep yields consistent by using a semi-fixed approach; something she has only changed recently due to lower rates.

“I like to refinance from one fixed package into another. So when a five year fixed-rate ends, I prefer to refinance into another five-year fixed rate, just to make things as consistent as possible.

I am not doing that now though, as interest rates are so low. You have to be adaptable. Sometimes you can’t have just one strategy and be stubborn, you need to adapt.”

Property investment isn’t always passive

Jasmine disagrees with property being a labelled a passive investment:

“Property is not like a unit trust or something, where you can just buy it and forget about it. There are always things to fix and tenant issues to address; and the more properties you take on, these problems will grow exponentially.

Even with just three units, I have to deal with a tenant problem at least once every two weeks or so. I think if I own more it will become my full-time job.”

Consider something as trivial as a tenant losing their keys:

“We were in the US at the time, and the tenant called and said he lost the key and couldn’t get in. The spare key was still in the house.

I had to coordinate with a relative to get a locksmith there to handle it. And then the locksmith we called didn’t turn up, and my relative had to leave, so I had to call another locksmith myself, explain everything, and so on. And I was doing this at midnight through to 2 am where I was.”

There were also bizarre situations that happened “maybe once every year without fail”, according to Jasmine.

“One time the other tenants called to complain, that one of them was always peeing in the sink in the common bathroom. When I called to check, he accused the other tenants of peeping; but it’s also his fault as he didn’t close the door, and one person recorded him on his phone. Sometimes it’s like dealing with children.”

Just last year, Jasmine had to deal with another situation where a student tenant got into a fight and was expelled; she had to break her lease. Jasmine wouldn’t go into the specifics of the solution, but she said it was “complicated by the fact that her parents had already paid 12 months rent upfront.”

The main takeaway from Jasmine’s experience is that:

“Property is a passive investment if you’re just buying a home you hope you’ll appreciate, or you have just one unit that you rent out. But you’ll be surprised how time consuming it can become once you have more than one property asset to manage. One plus two small units already take so much effort.”

Any advice for our budding landlords?

“Things are always changing”, Jasmine says, “investment styles that worked in 2000 or 2010 may not work in 2020. This is true for any kind of investment, and property is not special that way. Things like the ABSD happen overnight.

Don’t try to exactly copy how someone else did it 10 or 20 years ago. If they made a lot of money doing it back then, there’s high chance the government has done something to stop it, to prevent the market from overheating.”

One of the examples Jasmine points out is opening a company, and then buying properties through it. This method would be counter-productive today, as it would incur 25 per cent ABSD.

“But despite the difficulties, I do feel it’s worth it. There’s a sense of security in knowing that you own tangible properties.”

If you would like to keep up to date, follow us on Stacked as we track the latest news and changes. And if you’re an aspiring landlord with questions, do drop us a message on Facebook.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

2 Comments

Oh, Jasmine has these Landlord’s ordeals with three Spore properties! Imagine owning five properties in four different countries! If you think owning compact properties of less than 500sf is small, then think of 25 to 30 sq metres studios in many oversea countries such as Thailand and Philippines.

Today, many Sporeans are compelled to invest overseas due to ABSD, high cost of properties itself, and strong SGD. Besides, the returns from Spore properties (based on 1-bedroom units of >500sf) at 3% is not lucrative as similar oversea units fetch higher returns as much as 6-8%. Moreover, most of the oversea properties are freehold.