When it comes to private property, District 9 (D9) has long been the benchmark of Singapore’s luxury market. This district encompasses some of the city’s most desirable neighbourhoods, from Orchard to River Valley, and with local buyers now reclaiming the CCR, properties here are bound to draw attention.

But in a district already packed with freehold luxury condos, buyers today face a tough question: should you go for the glossier new launches, or are the older resale options offering better value?

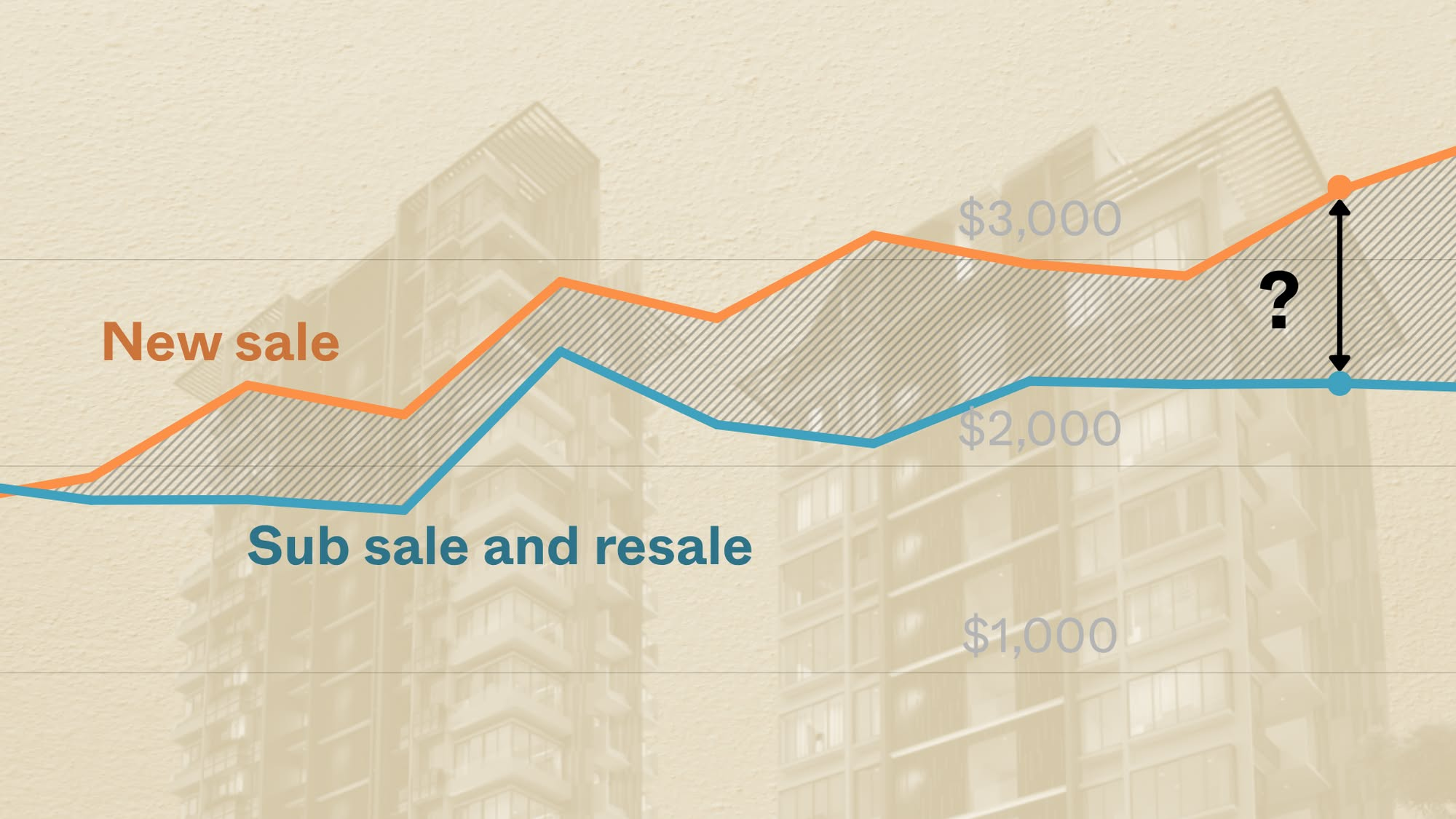

To find out, we dug into the data. After analysing District 9 transactions over the last 10 years, we break down the actual price gaps between new launch and resale condos—by unit size, from compact 1-bedders to spacious 3-bedders. The results may surprise you.

0 Comments