Most Singaporeans will use their CPF in some form, to purchase their property. This has resulted in some debates over the years, regarding how much of our CPF we should use; or whether HDB upgraders should be using more cash instead. In the following guide, we clarify how – and how much – of your CPF can be used when purchasing various properties:

The challenge for many buyers today isn't access to information.

It's interpreting that information in a way that makes sense for their finances, goals, and stage of life.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

How is CPF used to buy a home?

Your CPF Ordinary Account (CPF OA) can be used to buy residential properties, under the CPF Housing Scheme.

Under this scheme, your CPF OA can be used to purchase both HDB residences, as well as private residential properties in Singapore. Your CPF OA can also be used for the construction of private property (e.g., building your own landed property).

Your CPF monies can be used to pay for the following:

- Part of the down payment to purchase your home

- Servicing your HDB loan or bank loan

- Servicing construction loans, as well loans taken to buy the land for your house

- Buyers Stamp Duty (BSD) and Additional Buyers Stamp Duty (ABSD)

- Premiums for Home Protection Scheme (this is a mandatory mortgage insurance policy for HDB properties)

- Legal fees, depending on the law firm used

With regard to legal fees, note that you can always use CPF if using HDB’s appointed law firm. For bank loans, some law firms can be paid through your CPF, but others may require you to pay cash – do check before appointing the firm.

Note that renovation costs, Cash Over Valuation (COV), property agents’ service fees, and residential properties outside of Singapore cannot be paid with CPF.

How much of your CPF can you use?

For downpayment of properties:

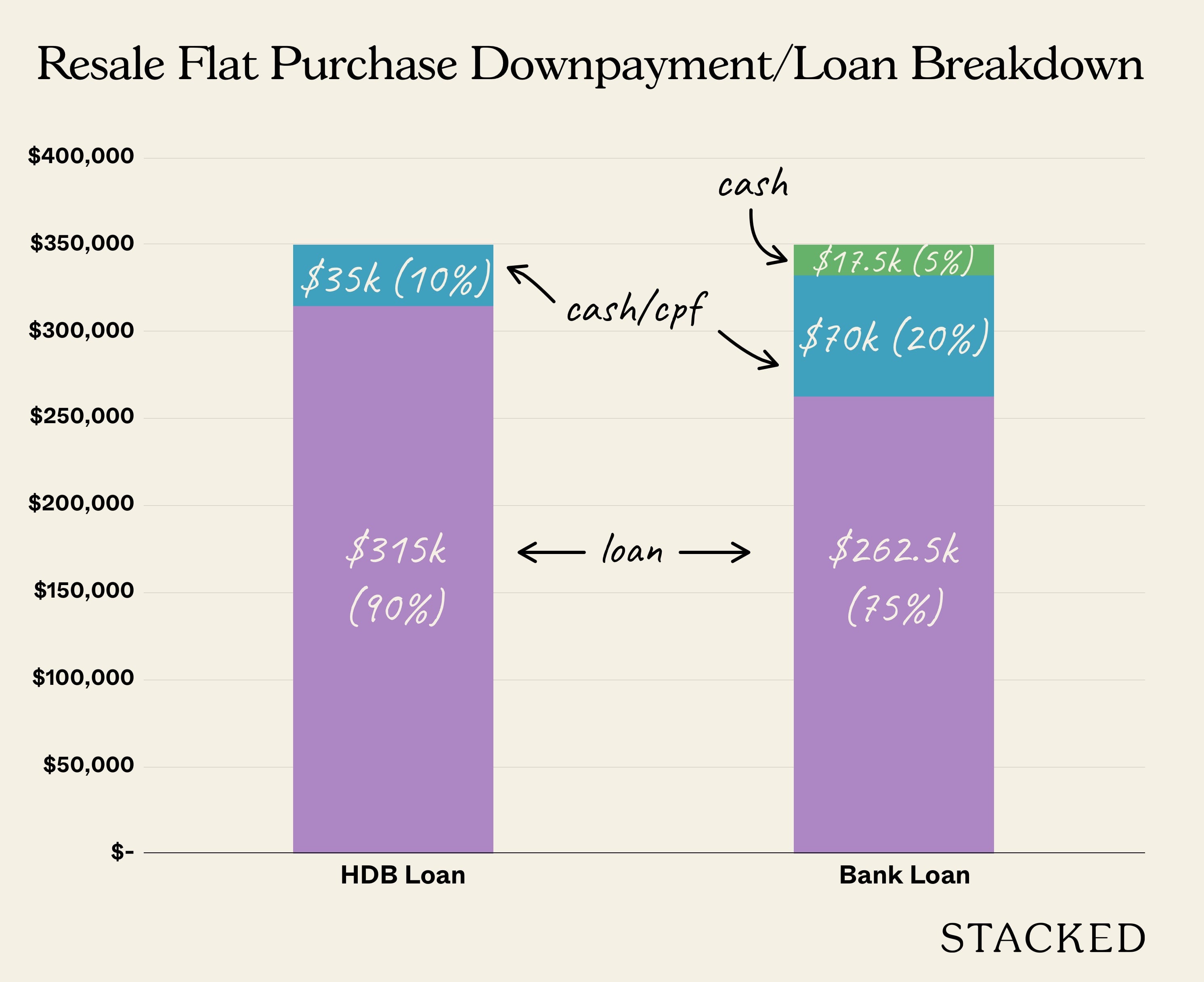

If you’re using an HDB loan, the maximum financing is usually 90 per cent of the price or value, whichever is lower (for BTO flats, the value is considered to be the same as the price).

The remaining 10 per cent down payment can be paid in any combination of cash or CPF.

For example, if your flat costs $350,000, then the minimum down payment is $35,000. This can come entirely from your CPF OA if you like. Otherwise, you can pay part of it in cash, and part of it with your OA (e.g., $20,000 from CPF, and $15,000 in cash).

Do note that the max that you can keep in your CPF OA is $20,000 if you are taking an HDB loan. In other words, anything that is in excess of the 10 per cent downpayment, you will have to use until you are left with $20,000.

For downpayment of private properties:

If you’re using a bank loan, the usual loan limit is 75 per cent of the property price or valuation, whichever is lower.

The first five per cent of the property must be paid in cash, while any combination of cash or CPF can be used for the next 20 per cent. For example:

If a property costs $1 million, the first $50,000 must be paid in cash. The next $200,000 can be paid in any combination of cash or CPF (e.g., $100,000 in cash and $100,000 from CPF, or $50,000 in cash and $150,000 from CPF).

If the property is sold above the actual valuation (both HDB and private).

For resale properties, it’s possible that the seller’s price may be higher than the actual valuation (e.g., a flat is valued at $350,000, but the seller wants $370,000). This is referred to as Cash Over Valuation (COV).

In these instances, neither the home loan nor your CPF can be used to cover the excess $20,000. You’ll have to pay the amount in cash.

Limits on CPF usage

- Limitations based on age and lease

- CPF withdrawal limit

1. Limitations based on age and lease

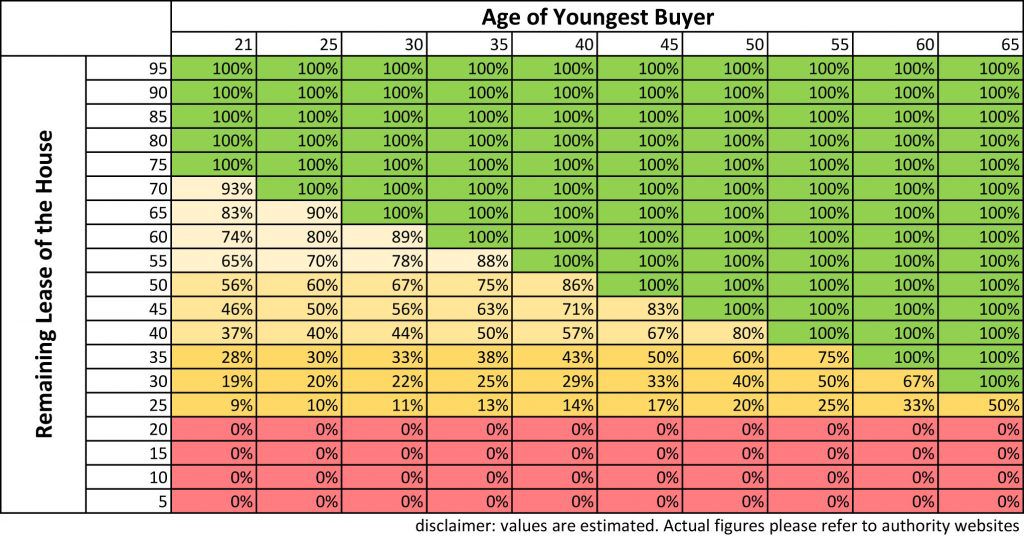

The property must have a remaining lease of more than 20 years. Otherwise, you cannot use any CPF monies to purchase the property. Besides this, your age is also a factor:

The age of the youngest owner, plus the remaining lease, should equal or exceed 95 years. If it would be less than 95 years, maximum CPF usage will be pro-rated, based on how near the lease comes to lasting till 95. To find the pro-rated amount, use the CPF website’s online calculator.

For example, say you are 35 years old, and your spouse is 28 years old. You want to buy a property with 60 years left on the lease.

60 + 28 (youngest owner only) = 88 years.

In this instance, the maximum CPF usage will be reduced, and based on the pro-rated amount.

On the other hand, if your spouse were also 35 years or older, you would be able to use the normal CPF limits below (60 + 35 = 95 years).

Assuming the remaining lease can cover the youngest owner using CPF for the flat till age 95, then the next limit would be the:

2. CPF Withdrawal Limit

You can only withdraw up to the CPF Withdrawal Limit (WL) when paying for your property. After this, you will need to pay any housing costs – such as your outstanding home loan – in cash. The WL depends on several things, namely the property type, type of loan (HDB/Bank) and whether or not you met your Basic Retirement Sum (BRS).

The normal WL is as follows, for buyers of a first property:

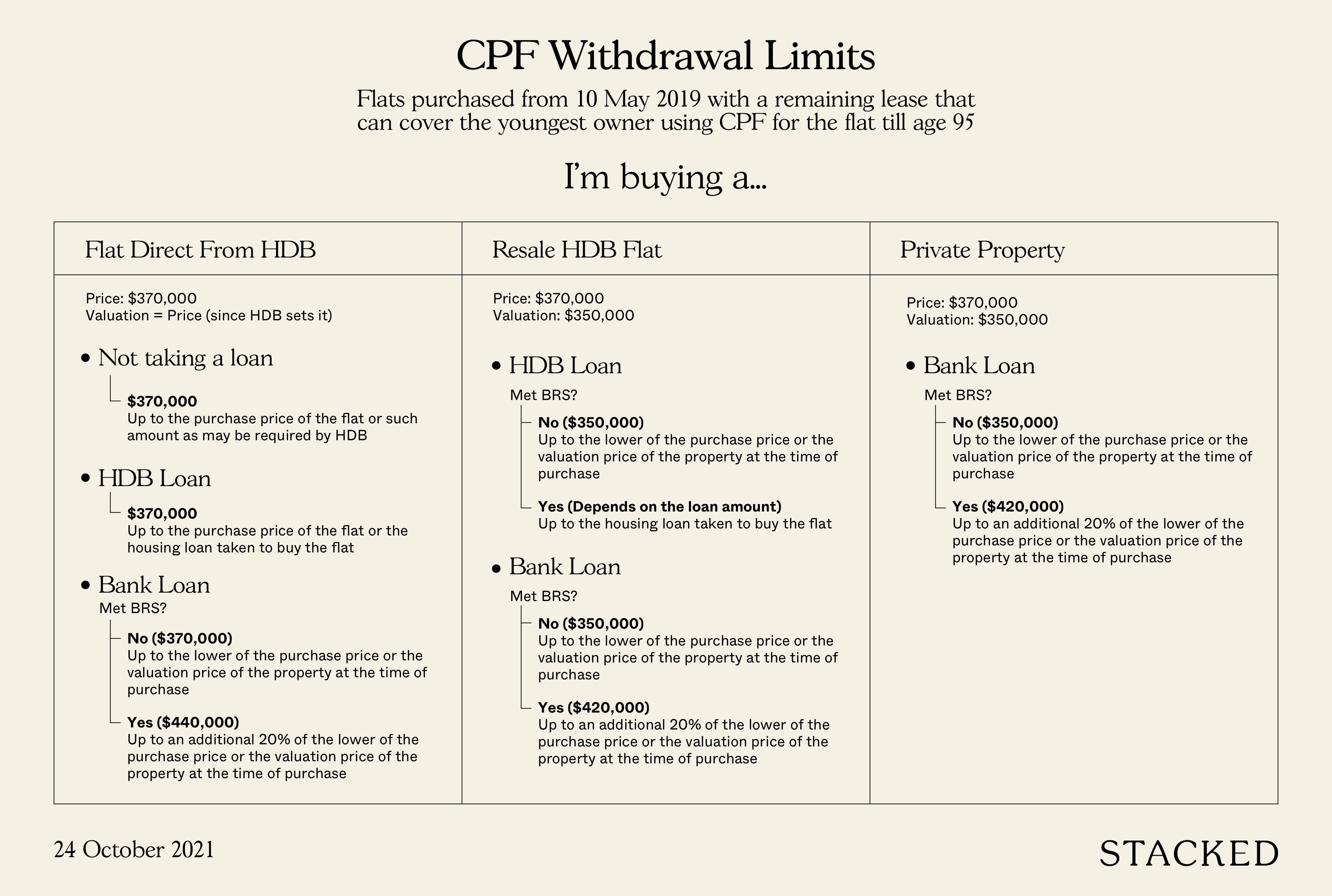

BTO flats (using HDB loan)

You can use all available CPF OA savings, until you run out or the flat is paid off.

BTO flats (using bank loan)

You can use up to the lower of the purchase price or the valuation price of the property at the time of purchase, if you cannot set aside the BRS.

For example, if the flat is $350,000, you withdraw up to $350,000 from CPF OA, before you need to start paying in cash.

You can use up to an additional 20% of the lower of the purchase price or the valuation price of the property at the time of purchase, if you can set aside the BRS.

Resale flats (using HDB loan)

The WL is the lower of the valuation or property price (at the point of purchase). For example, if the property is $350,000, and the selling price is $370,000, the WL is $350,000.

If there’s any loan amount outstanding after you’ve used this $350,000, you can only use further OA savings if you can set aside the Basic Retirement Sum (BRS). You can check your BRS amount here.

Resale flats and private properties (using bank loan)

The WL is the lower of the valuation or property price (at the point of purchase).

If there is still an outstanding loan after you reach the WL, you may withdraw another 20 per cent of the value of property price (whichever is lower) from CPF OA. However, this is provided you can set aside the BRS.

So if the property’s valuation is $350,000, and the selling price is $370,000, the WL is $350,000.

If there’s an outstanding loan amount after you’ve used $350,000, you can withdraw a further $70,000 (20 per cent of $350,000) from CPF; this is provided you can set aside the BRS.

If you can’t meet the BRS, any amount after $350,000 will have to be paid in cash.

For buyers of a second property, you must set aside the BRS before you can use any remaining CPF monies. In all instances, the WL will be capped at the lower of the valuation or price.

Among new home buyers, a common question we get is how exactly they could exceed the WL.

Do remember that you pay more for your property than the actual price or value, after factoring in the interest from your home loan.

For example, say you take a loan of $315,000, for a $350,000 flat.

Your WL is $350,000.

At 2.6 per cent interest over 25 years (HDB loan), the approximate total repayment is $428,718, or about $78,718 above the WL.

For this reason, we suggest that you check your CPF usage every two or three years, to be aware of when you’re close to the WL. It’s also important to refinance your home loan when necessary, to keep the rates as low as possible.

You may find the official terms and conditions from CPF here.

Should you use cash or CPF to buy your property?

We explain the advantages of using cash, instead of CPF, in this article. But as a quick recap:

You need to refund the CPF monies you’ve used, along with the accrued 2.5 per cent interest, when you sell your property. Any excess is then given to you in cash. However, there is a risk that you need to refund more than the sale proceeds, which means you will not be left with any cash after the sale.

You do not need to top up the difference, provided you sold your home at or above market value. You can also use your CPF for the next property you buy. However, the lack of cash in hand could make it hard to cover the down payment (as you need a minimum of five per cent cash down for private properties).

Second, your CPF provides a guaranteed interest rate of 2.5 per cent per annum. Leaving more cash in your CPF could be healthier for your retirement. However, you should speak to a qualified financial planner, on whether this approach makes sense for you. It’s not always wise to be cash-strapped, while locking money in your CPF.

For more help on purchasing a home in Singapore, reach out to us at Stacked. We can guide you on details specific to your needs. You can also check out in-depth reviews of new and resale homes alike.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

0 Comments