Hi StackedHomes,

I started reading your content a year ago and really enjoyed the articles on home renovation case studies and analysis on new condos. Now that my partner and I (late 20s) are currently looking to buy our first matrimonial home, and have unfortunately (or fortunately) exceeded the income cap for HDBs and ECs, I was hoping to write in to gather your professional opinion on the available options we have

We have a combined income of 18,000/m, CPF savings of 220k, and cash savings of 120k. Both of our families reside in the west and thus had gravitated to properties there, however, we are open to anywhere except the Northeast/East.

Multiple agents have recommended us to go for New Launch condos as we do not have an immediate need to move in (and also to take advantage of the progressive payment scheme) Also we are not planning for kids at the moment, but I wouldn’t rule the possibility out in a few years’ time. Housing-wise we are looking at capital preservation and proximity to amenities like hawker centers and the MRT.

With rising interest rates and property prices, we are stuck in a dilemma between:

- New launch 2 bedder but potentially stretching ourselves (eg Lentor, Arden, Jalan Anak)

- 4 room re-sale HDB in a nearby estate (eg Trivelis, Batok Skylines)

- Resale condo

- Waiting out the interest rates

Apologies for the long email!

(This is part of an ongoing series where we answer reader questions about the property market. If you have one of your own, send it to stories@stackedhomes.com.)

Hey there,

Thanks for reaching out to us! It’s definitely more of a fortunate situation to be in than an unfortunate one but we also understand the pains of these restrictions. The last time the income ceiling was raised was in 2019, and prices have risen quite a bit since then. As such, if you’re just hovering above the ceiling it can feel a bit like you’re stuck in no man’s land. However, you’re still in a great position and you do have options to choose from so let’s run through them!

So many readers write in because they're unsure what to do next, and don't know who to trust.

If this sounds familiar, we offer structured 1-to-1 consultations where we walk through your finances, goals, and market options objectively.

No obligation. Just clarity.

Learn more here.

Affordability

Let’s work out your affordability first based on the information given.

Based on a combined income of $18,000 per month, we will assume no other outstanding loans and take both your ages to be 29 years old for this calculation. Your maximum loan quantum will be:

For an HDB purchase – $1,078,655 (25 year tenure)

For a private property purchase – $2,204,680 (30 year tenure)

As your incomes exceed the $14,000 cap for an HDB loan, you’ll only be eligible for a bank loan where the loan quantum is up to 75% of the property price or valuation whichever is lower, and the remaining 25% will have to be paid either with cash or CPF (minimally 5% has to be paid in cash, 20% can be paid with CPF). This also applies to private properties.

If we were to utilise all your CPF funds of $220,000 for the 20% downpayment and $55,000 cash for the 5% downpayment, the maximum property price you’re looking at is roughly $1,100,000 even though your loan quantum for a private property is much higher. Do note that we have not taken into consideration other payable fees like BSD, and legal fees and if you were to purchase a resale property, you’ll also have to consider renovation costs. As such, we won’t be taking the full cash available to put into the deposit for the sake of prudence.

Costs breakdown for a $1,100,000 property:

| Purchase price | $1,100,000 |

| Valuation | $1,100,000 |

| 5% downpayment (Cash) | $55,000 |

| 20% downpayment (CPF) | $220,000 |

| Loan | $825,000 |

| Monthly repayment at 3.5% interest | $4,130 |

| Buyer Stamp Duty (BSD) | $28,600 |

| Legal fees | $2,500 |

Assuming no COV in this case, the total CPF outlay will be $220,000 and the total cash outlay will be $86,100. You’ll be stretched pretty thin with little emergency funds left.

Should you buy a 2 bedroom new launch?

Since the 3 projects you listed are not launched yet, we do not know what their exact prices are. But we can take a look at their breakeven prices and a mix of online sources to just get some indication.

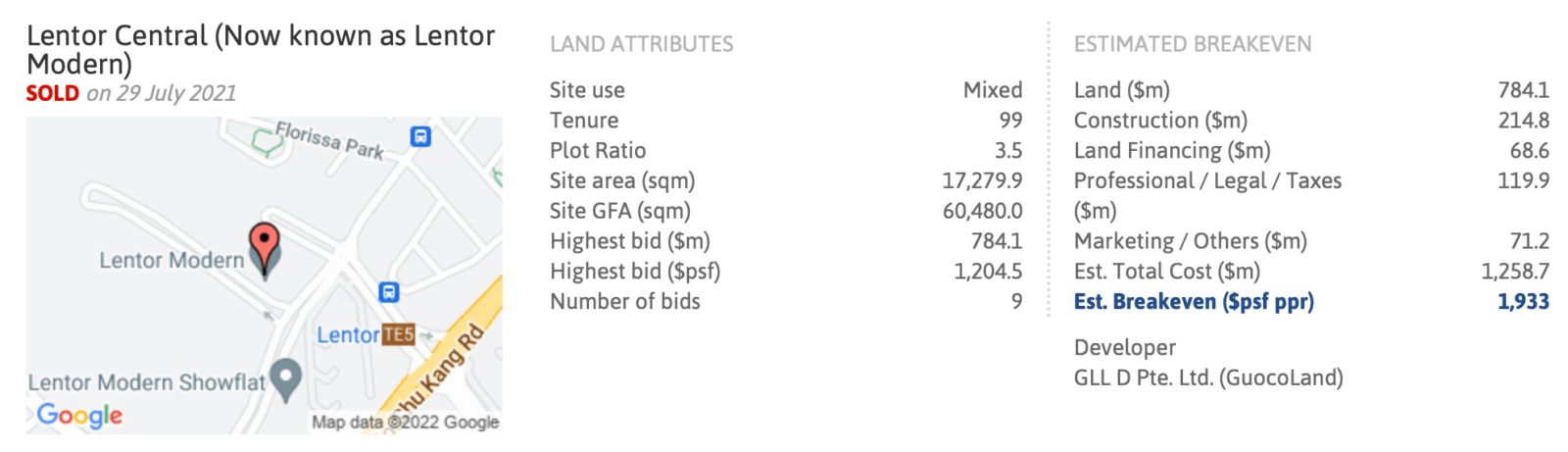

Lentor Modern

Estimated breakeven price – $1,933 psf

Predictive launch price – $2,337 psf

For a 700 sq ft 2 bedder, you’d probably be looking at a ballpark of $1,635,900.

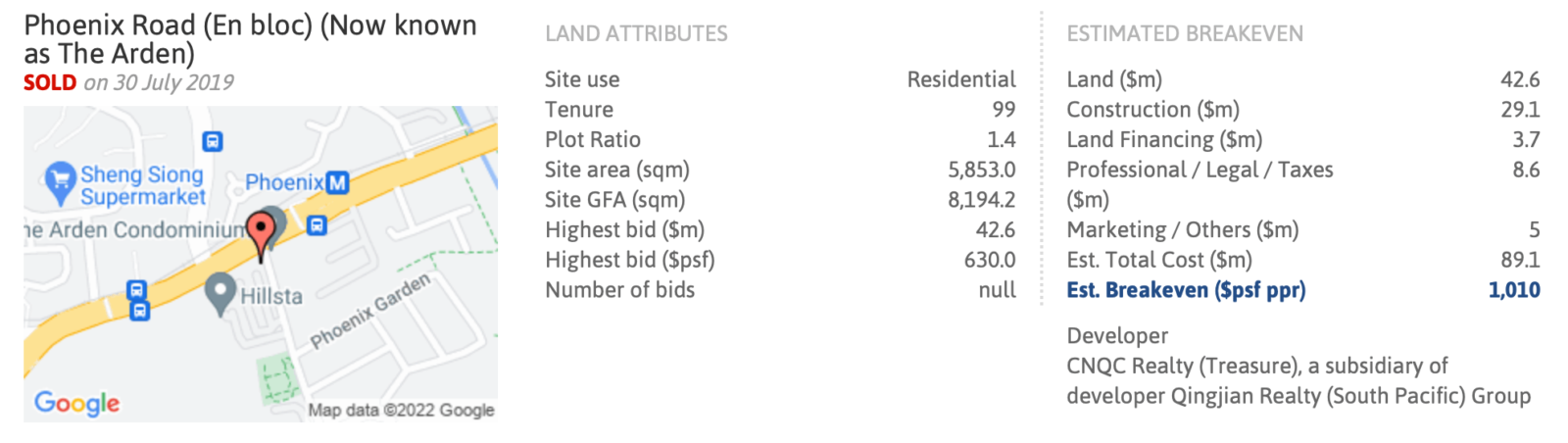

The Arden

Estimated breakeven price – $1,010 psf

Predictive launch price – $1,221.09 psf

For a 700 sq ft 2 bedder, you may be looking at a price of $854,763

That said, from what we see most sources are estimating this to be launched at $1,5xx, which seems more in line with current market prices today. At that price, you’d be potentially looking at a price point of $1.05 million instead.

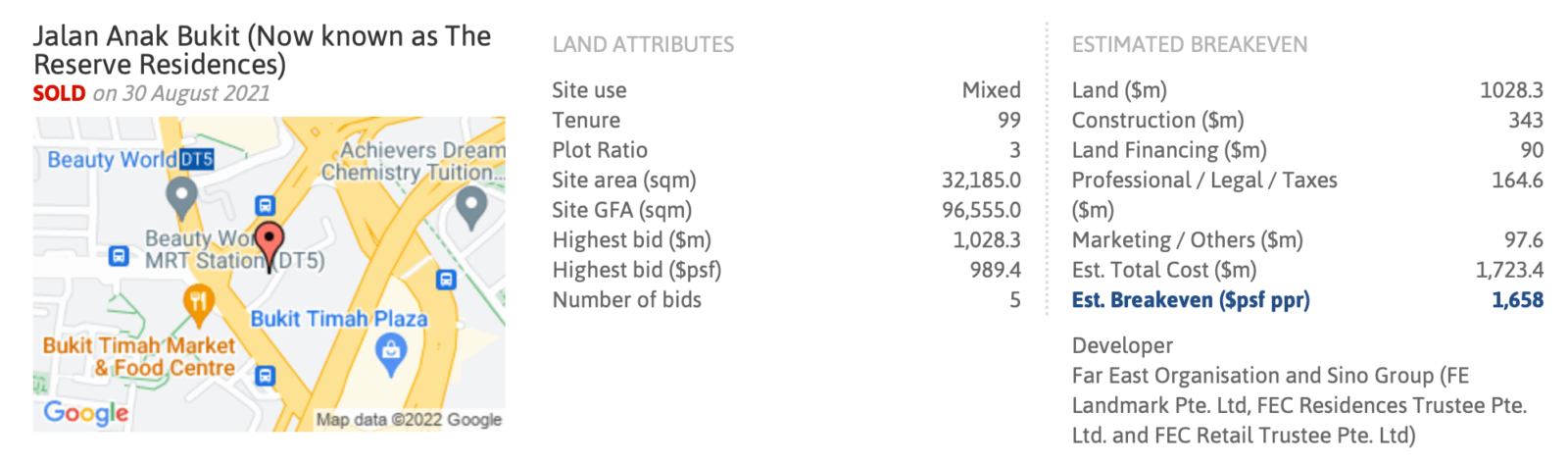

The Reserve Residences

Estimated breakeven price – $1,658 psf

Predictive launch price – $2,004.52 psf

For a 700 sq ft 2 bedder, you’d be looking at a price of $1,403,164.

To get a better overview, we can also look at the average new launch prices in the different regions over the past few months:

Outside Central Region (OCR)

For the past 8 months, the total number of new launches sold in the OCR is 1,512 units with an average of $1,808 psf.

Estimated price for a 700 sq ft 2 bedder – $1,265,600

Rest of Central Region (RCR)

For the past 8 months, the total number of new launches sold in the RCR is 2,324 units with an average of $2,282 psf.

Estimated price for a 700 sq ft 2 bedder – $1,597,400

Core Central Region (CCR)

For the past 8 months, the total number of new launches sold in the CCR is 1,214 units with an average of $2,799 psf.

Estimated price for a 700 sq ft 2 bedder – $1,959,300

Judging from the above, you guys may be priced out of the market with a $1,100,000 budget for a 2 bedroom unit. Unless you’re open to purchasing a 1 bedder which may not be the most suitable option should you decide to start a family a few years down the road.

These are some of the most affordable 2 bedroom new launches on the market at the moment:

| Project | District | Type | Size (sqft) | Level | PSF | Price |

| Zyanya | 14 | 2 BR | 614 | #04 | $2,015.14 | $1,237,296 |

| Mori | 14 | 2 + S | 721 | #02 | $1,930.65 | $1,392,000 |

| Bartley Vue | 19 | 2 BR | 657 | #11 | $2,162.86 | $1,421,000 |

| Pasir Ris 8 | 18 | 2 BR | 710 | #04 | $2,025.35 | $1,438,000 |

| The Gazania | 19 | 2 BR | 635 | #04 | $2,318.11 | $1,472,000 |

With rising land and construction costs, it is unlikely that prices will go back to pre-pandemic times. We have previously written an article on this, which you can read more on that here.

Should you buy a 4-room resale HDB in the neighbouring estates?

We have done up reviews for both Trivelis and Skyline I and II Bukit Batok if you would like to read more on the characteristics of these clusters!

Recent transactions for 4-room HDB units at Trivelis:

Recent transactions for 4-room HDB units at Skyline I @ Bukit Batok:

Recent transactions for 4-room HDB units at Skyline II @ Bukit Batok:

Based on your affordability of $1.1m, a 4-room flat in these clusters is definitely viable. One thing to note is that the HDB website does not reveal how much COV is paid for these units, if any.

For instance, the unit at Trivelis that changed hands in May 2022 for $790k, the valuation was actually at $760k and the buyer paid a COV of $30,000. It’s hard to define how much COV you should or should not pay for a property as this is subjective and every buyer may perceive the value of the house differently based on their own circumstances whether financially or emotionally.

One bonus is that despite your salaries exceeding the income limit for the CPF Housing Grants, you’re still eligible for the Proximity Housing Grant (PHG) of $20,000 if you were to purchase an HDB that is within 4 km of your parent’s place. (There’s no income ceiling for this).

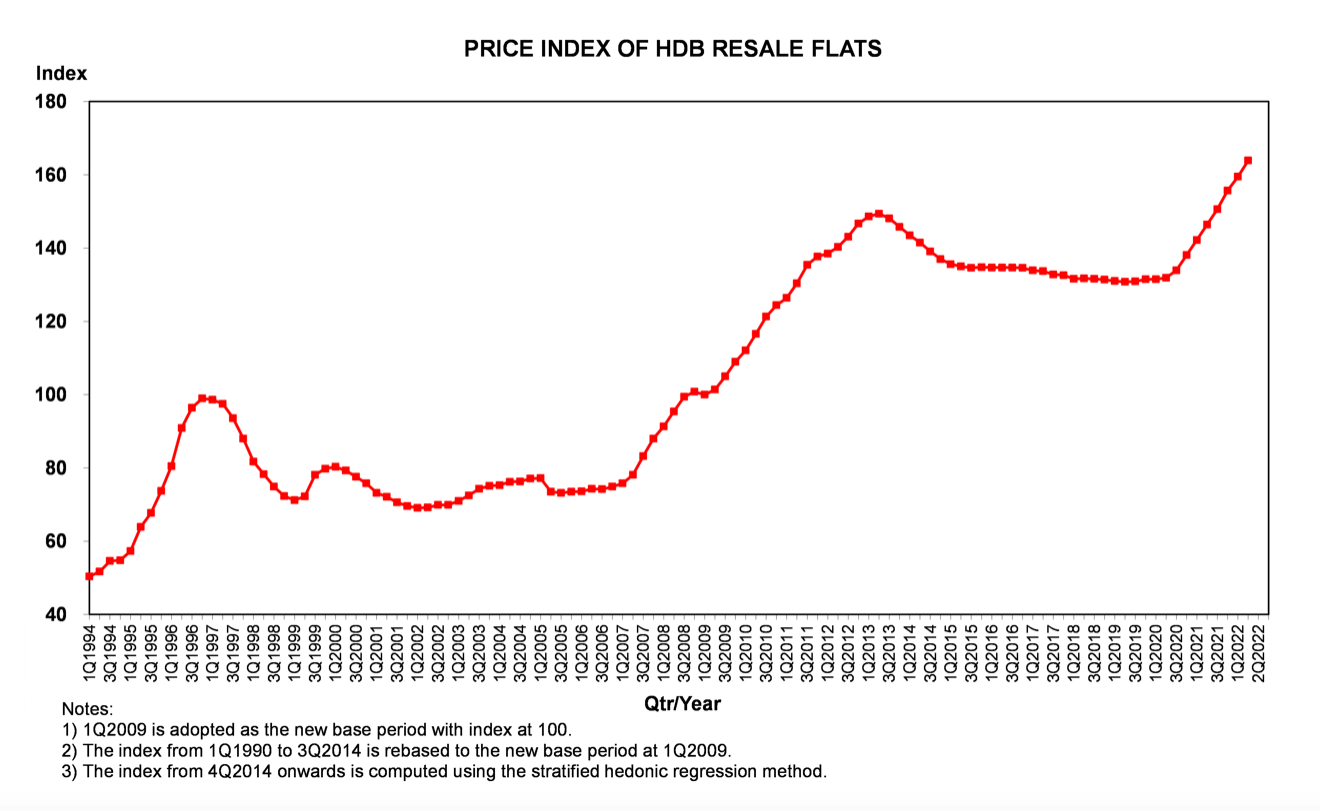

Generally, for most HDBs, their pricing will hit its peak upon meeting the MOP (or if you manage to get an early approval to sell before MOP, we have seen these units transacting at as high as $100k above valuation!). As these will be the youngest resale flats you can purchase on the secondary market and units are probably still in good condition, buyers may be able to save on reno costs, which is why there is always a demand for these flats.

However, if you’re thinking of buying a HDB that has just reached its MOP, holding period is a factor you should think about. If you’re planning to stay for a short term, say 5 years, and the supply of new HDB flats coming up in the area is low, prices are likely to hold up. But if your plan is to stay long term, say 10-15 years, it’s unlikely you’ll be able to sell the unit at the same price you got it for, especially if there is a constant influx of newer flats being built in the vicinity.

Of course, this varies from area to area depending on the demographics, demand, and supply. For example in Clementi, demand is more often than not, high, given its proximity to renowned schools. So prices of 20 year old flats are still almost on par with those that just recently hit their MOP.

On the other hand, if we were to compare a 20 year old flat in Bukit Batok versus one that just reached its MOP, you will see there is a price disparity which is a normal occurrence in most estates as prices do gradually decrease as their lease decays.

Cost breakdown of purchasing an HDB at $750,000:

| Purchase price | $750,000 |

| Valuation | $750,000 |

| 5% downpayment (Cash) | $37,500 |

| 20% downpayment (CPF) | $150,000 |

| Loan | $562,500 |

| Monthly repayment at 3.5% interest | $2,816 |

| Buyer Stamp Duty (BSD) (CPF) | $17,100 |

| Legal fees (CPF) | $2,500 |

| Proximity Housing Grant | $20,000 |

Assuming no COV in this case, the total CPF outlay will be $149,600 after deducting the $20,000 PHG and total cash outlay will be $37,500. You will still have some CPF funds left in your account which you can use for your monthly repayments and also cash on hand in case of emergencies or if investment opportunities arise.

Should you buy a resale condo?

When buying a resale private property, there are several things you should do your due diligence checks on to see if the development meets your needs and requirements, you can read more on that here!

There are certain advantages when it comes to buying a resale condo such as:

- Having the option to rent it out immediately if you don’t need to move in anytime soon

- Since the rental market is doing well at the moment, the rent could partially or even fully cover the monthly repayments. In a way, someone is paying your mortgage for you, and your funds are hedged against inflation.

- Shorter holding period

- You’ll be able to sell the place in 3 years time (without having to pay SSD) in the event you need a bigger space for your family or want a change of environment.

If you were to search on PropertyGuru for 2 bedrooms units under $1.1m, there are over 1,200 listings available. We picked out some of the younger 2 bed 2 bath units in the west for your reference but it’s best you consult an agent for further analysis on their suitability.

| Project | District | Tenure | TOP | Size (sqft) | Price |

| Parc Riviera | 5 | 99-years | 2020 | 710 | $1,080,000 |

| Waterfront @ Faber | 5 | 99-years | 2018 | 752 | $1,068,000 |

| Westwood Residences (EC) | 22 | 99-years | 2018 | 689 | $880,000 |

| Eco Sanctuary | 23 | 99-years | 2016 | 732 | $1,100,000 |

| Foresque Residences | 23 | 99-years | 2015 | 743 | $1,090,000 |

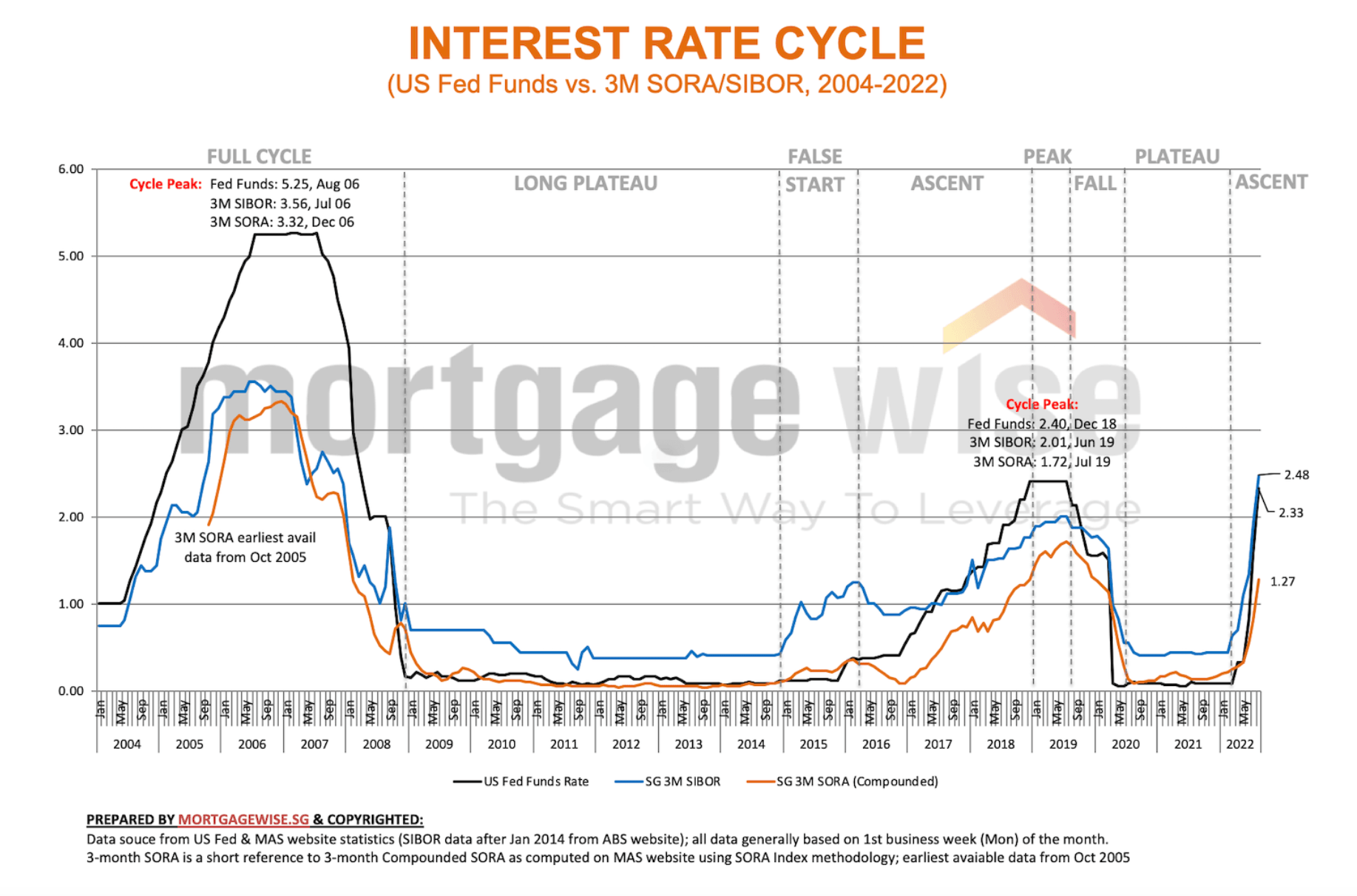

Should you wait out the interest rates?

“UOB analysts echoed that market expectations remain firm for the Fed to continue hiking rates and expect three more interest rate increases – ranging from 25 to 50 basis points – over the rest of 2022. The Fed could also extend the rate-hike cycle to early next year, they added in a report.” – Business Times, 28 July 2022

“And the central bankers said even when the rates hit a “sufficiently restrictive level”, they may keep them there for some time to ensure that inflation falls.” – Business Times, 18 August 2022

From the looks of it, interest rates are not likely to come down anytime soon. In spite of this, the local property market is still resilient and on an upward trend albeit with a slight slow down as compared to last year. For more consequences of rising interest rates, you can read more here.

The good news is that what goes up must come down, and looking at past interest rate hikes in 2004 and 2017, these did not last for more than three years.

As the saying goes, time in the market beats timing the market. There are still opportunities to enter at the moment but more importantly, you’ll need to ensure your funds are in check should the interest rates continue to go up.

Conclusion

Frankly, a new launch may not be feasible at this point unless you look at the smaller 1 bedroom units. But that might not meet your needs should you decide to start a family, and selling a home sometimes may take a lot longer than you think. Unless you take this purely as an investment and sell it upon TOP or rent it out until the time comes that you need a place to move into.

Especially if you are going to consider a 1 bedroom, we would also caution first-time home buyers to really take a look at the actual size of the unit to see if it can fit their lifestyle. We’ve met many such people who’ve purchased a unit at the show flat, only to be surprised at how small the unit is once it is completed.

Also, even for the bigger 2 bedroom units, it may not be the most ideal even with 1 kid in terms of space. You’d be surprised at just how many additional things you need to buy when you have children (thereby requiring more storage), and also if both of you are going to continue working, the possibility of a helper – which many new 2 bedroom units do not have a utility room for you to use.

For own stay purposes, a resale HDB is definitely a more suitable option and you will not be stretching yourselves too thin financially. The size is flexible enough for any future changes, and we’ve seen many creative options in our Living In series on YouTube, where a couple really makes full use of the additional space. Be it an awesome study area, additional space for an indoor garden, or a room to string a hammock across, these are lifestyle options that you won’t be able to enjoy without the flexibility of more space.

As for resale condos, you do have a wider range of choices as compared to new launches and it also gives you more flexibility with the option to immediately rent it out and a shorter “MOP” but it boils down to choosing the right development with potential capital gains in the future should you decide to sell.

To conclude, we’d really think hard about the future plans before putting a commitment into any housing purchase. As long as kids are not off the table completely, planning to have kids can be quite an uncertain thing. We know of people who’ve had to wait for a couple of years, and also of people who had them earlier than they planned. And when that happens, the scramble to sell the home, and look for a suitable option can be stressful (along with all the other changes!).

Your needs and priorities can change quite drastically, even from your late 20s to early 30s. Given that a suitable new launch condo seems quite out of the question at the moment, the choice boils down to a resale HDB or condo option for you.

We are leaning towards a resale condo option, with the main reason being that you are able to sell at the 3 year mark. That does give you more flexibility to change things up in the future as your situation changes, as the 5 year HDB MOP can be quite a stickler in your plans.

You do have to be patient with resale properties, as the right unit may not always be available when you want it. The problem is you’d never know when a “better” or more suitable unit might come on the market, or even at all. But given you don’t seem to have a time constraint, that may be a plus point in your favour right now.

Have a question to ask? Shoot us an email at stories@stackedhomes.com – and don’t worry, we will keep your details anonymous.

For more news and information on the Singapore private property market or an in-depth look at new and resale properties, follow us on Stacked.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

2 Comments

I think in order not to overstretch yourself, you should consider a resale HDB instead of condo.

My advice is to either (i) buy a resale hdb or (ii) stay with parents/ parents-in-law for a few more years. Continue saving along the way. Down the road, you can revisit this to see if a bigger condo is what you really want. Don’t be too stressed out paying a high mortgage from such a young age. Enjoy life (while still young) 🙂