The October 2024 BTO launch is just around the corner as we write this, and it’s one of the most significant in recent years. This will be the first launch using the new classification system, where flats are divided into Standard, Plus, and Prime categories. The launch will involve 15 HDB projects, of which seven are under the Plus category, and one is Prime. Here’s what you can expect:

The upcoming BTO sites

A quick note: we’ve already covered the sites in a previous article; but at the time we didn’t have a confirmed statement of which sites were Standard, Plus, or Prime. This is the current breakdown of flat numbers in each category. Note that the numbers are BTO launch estimates, so the exact numbers may differ slightly during the actual launch:

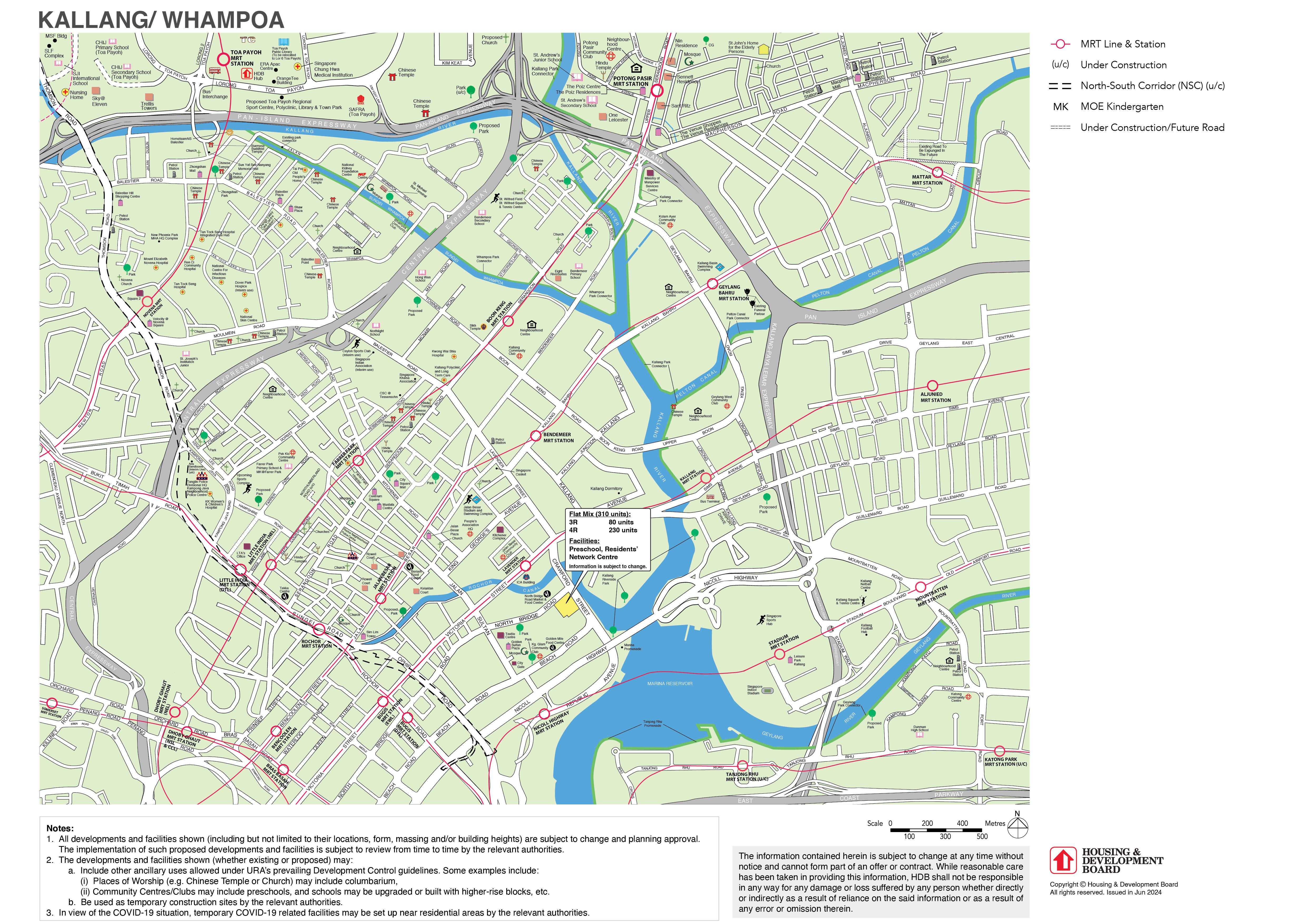

Crawford Heights (Prime, Kallang/Whampoa)

| 3-room | 4-room |

| 80 | 230 |

Kallang View (Plus, Kallang/Whampoa)

| 3-room | 4-room |

| 70 | 200 |

Tower Breeze (Plus, Kallang/Whampoa)

| 2-room | 4-room |

| 140 | 220 |

Central Trio @ AMK (Plus, Ang Mo Kio)

| 2-room | 4-room |

| 160 | 270 |

Bayshore Vista (Plus, Bedok)

| 2-room | 3-room | 4-room |

| 200 | 80 | 450 |

Bayshore Palms (Plus, Bedok)

| 2-room | 4-room |

| 160 | 550 |

Kembangan Wave (Plus, Bedok)

| 2-room | 4-room |

| 110 | 230 |

Merpati Alcove (Plus, Geylang)

| 2-room | 4-room |

| 260 | 160 |

West BrickVille (Standard, Bukit Batok)

| 2-room | 3-room | 4-room | 5-room | 3Gen |

| 130 | 90 | 260 | 170 | 40 |

Taman Jurong Skyline (Standard, Jurong West)

| 2-room | 3-room | 4-room | 5-room | 3Gen |

| 550 | 120 | 590 | 500 | 80 |

Costa Riviera I (Standard, Pasir Ris)

| 3-room | 4-room |

| 90 | 190 |

Costa Riviera II (Standard, Pasir Ris)

| 2-room | 4-room | 5-room | 3Gen |

| 140 | 200 | 110 | 30 |

Fernvale Oasis (Standard, Sengkang)

| 2-room | 4-room | 5-room |

| 180 | 340 | 320 |

Fernvale Sails (Standard, Sengkang)

| 2-room | 3-room | 4-room | 5-room |

| 130 | 90 | 220 | 110 |

Marsiling Ridge (Standard, Woodlands)

| 4-room | 5-room |

| 160 | 130 |

You’ll notice that this is a very high number of flats and locations for a single BTO launch (around 3,270 units). Indeed, the flats offered during the October launch will constitute around 40 per cent of the entire BTO supply for 2024, and it’s one of the biggest single launches we’re likely to see in some time.

Some interesting details about the Plus and Prime sites:

- 1. It’s possible to have Plus and Prime flats in the same town, in the same launch

- 2. In future, “Prime” may not just be based on proximity to the city centre

- 3. For now, there’s little difference besides the SR, between Plus and Prime

- 4. A cap on price growth due to the income ceiling and MSR

- 5. No fixed numbers on Plus or Prime offerings each year

1. It’s possible to have Plus and Prime flats in the same town, in the same launch

Crawford Heights, Tower Breeze, and Kallang View are all within Kallang/Whampoa, but they have different classifications. This is based on access to different levels of amenities: as we mentioned in our previous article, Crawford Heights – being close to North Bridge Road, Haji Lane, etc. – snags a Prime classification, while Kallang View and Tower Breeze are “only” Plus category flats.

This could, however, prompt arguments about how the lines are drawn. Deciding where the amenities are “superior” is not always obvious (especially in more mature towns, where almost everywhere is convenient in its own way). So when Plus and Prime offerings appear in the same town, we think buyers are going to ponder whether the premium for Prime flats is justified.

2. In future, “Prime” may not just be based on proximity to the city centre

To date, we’ve made the assumption that the main difference between Plus and Prime is that Plus flats might be the hub of fringe neighbourhoods, whereas Prime refers to the city centre; it’s an assumption shared by many of the realtors or analysts we’ve spoken to as well.

But it turns out this isn’t a rule per se. For now, the Prime projects are the ones which are closer to the city centre. In the future, however, there’s a possibility that we’ll see Prime housing even in non-central areas. This reflects quite a lot of confidence in decentralisation; and it’ll be interesting to see how we justify the differences between Plus and Prime in an area like, say, Punggol in the distant future.

(Our guess: it will mainly come down to market rates of surrounding flats, more so than a qualitative assessment of amenities; although the two are interrelated).

3. For now there’s little difference besides the SR, between Plus and Prime

The various restrictions, such as an income ceiling on resale buyers, 10-year MOP, inability to rent out the whole flat, etc. apply to both Plus and Prime. The main difference boils down to price, and the Subsidy Recovery (SR).

(The SR is a clawback, implemented at the point of sale to compensate for the higher subsidies needed to make these flats affordable. The SR only applies to the first batch of owners).

Existing Prime projects have had an SR of nine per cent, and this will be the first time we see the SR of Plus flats. If it’s not too far below nine per cent, some buyers will likely shrug it off as irrelevant and go for the Prime option instead. From word on the ground, we’ve heard the SR for Plus flats may be around six per cent.

In any case, this was a smart move that keeps things simple for buyers. We hope it stays the same, as changing other conditions (e.g., eligibility requirements) between Plus and Prime would make an already complex system even tougher to comprehend.

Speaking of eligibility requirements…

4. A cap on price growth due to the income ceiling and MSR

Plus flats, like their Prime counterparts, impose a $14,000 a month income ceiling even on resale buyers. This is different from standard resale flats, where there’s no income ceiling at all.

The combination of the income ceiling, along with loan curbs like the Mortgage Servicing Ratio (MSR), is aimed at preventing enclaves of the rich from forming in HDB towns. This is intended to restrict the price growth of Plus as well as Prime flats, and create a balanced socioeconomic mix. It’s too early, however, to tell if this will work. On a psychological level, simply grouping the flats into Standard, Plus, and Prime is already a way to stratify the town.

5. No fixed numbers on Plus or Prime offerings each year

We’ve been told there’s no particular rule on the number of Plus or Prime offerings each year. It may even be possible for a year to go by with no such offerings, depending on the viability of the situation.

This is probably good for all of us, as it gives HDB more flexibility to build as needed. However, it also means you shouldn’t assume you’ll have another pick of Plus or Prime properties next year, next launch, etc.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

0 Comments