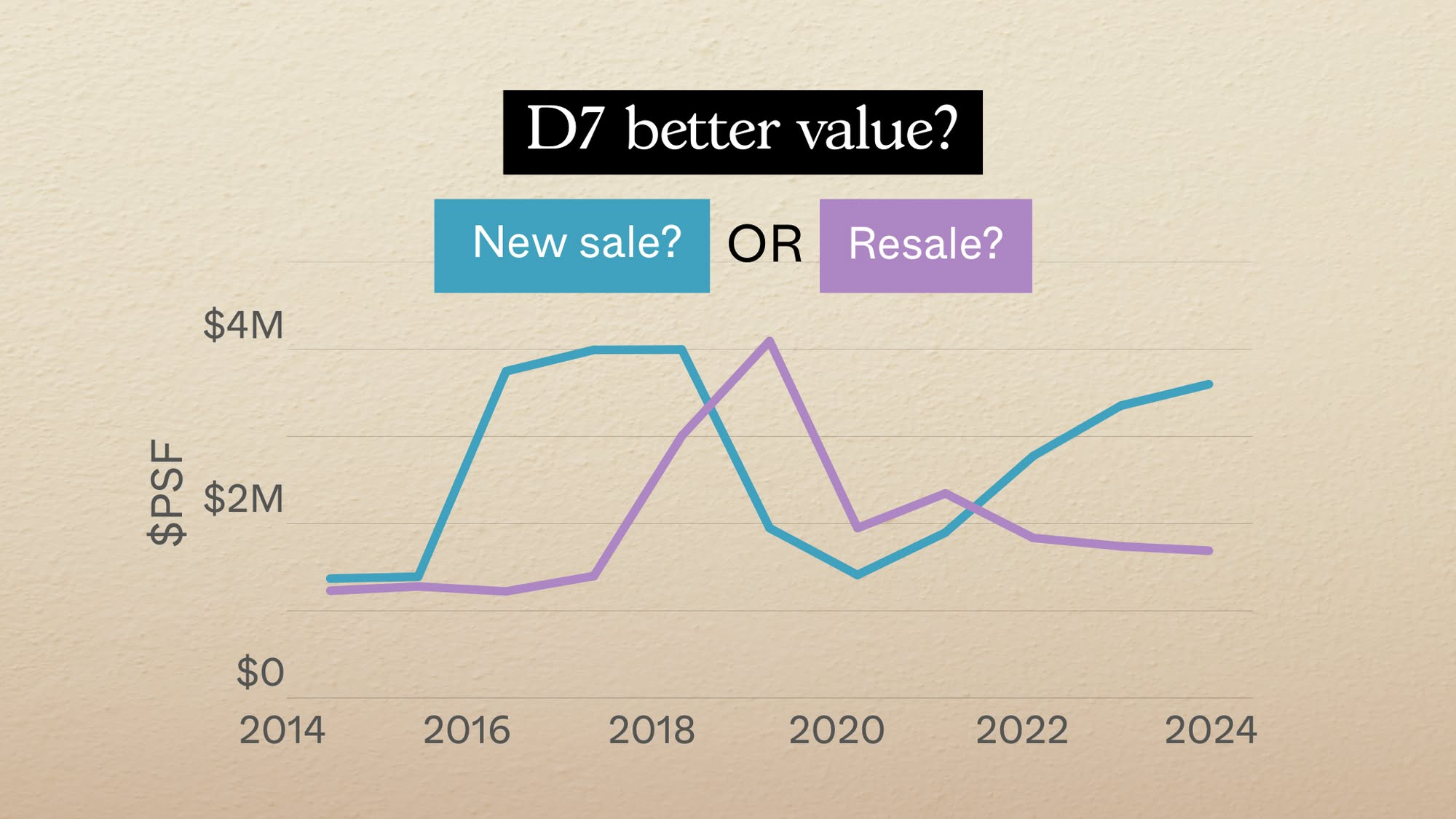

District 7 is one of the few areas where the official zoning and market reality don’t quite align. Although URA classifies it as part of the Rest of Central Region (RCR), parts of it are in the Core Central Region (CCR). As such, the transaction data tells a different story: several new launches in Bugis and Rochor have crossed $3,000 psf, a level more commonly associated with District 9. In fact, some projects here have transacted at premiums above nearby CCR counterparts.

This raises a practical question for investors: if D7 is already pricing like a CCR district, is there still a case to buy in, and should you be looking at new launches or resale projects for better value?

So many readers write in because they're unsure what to do next, and don't know who to trust.

0 Comments