Hello Stacked,

I enjoyed all the videos and articles produced by Stacked. It is very enriching and informative, especially to newbies like myself when it comes to residential issues.

I hope to consult you on the best solution for my property purchase. My wife and I are unable to decide and are stuck in decisions. With the rising property price and personal circumstances, we can’t seem to agree with each other on personal preference and views.

We are in our mid 40s (wife is 42 and I am 45) with 2 kiddos at 1 years old. Currently, we are staying in an EC, 3 bedroom unit in Sengkang, bought 5 years ago and recently reached MOP. Our unit is too small for 4 of us to stay. The main reason is one bedroom is converted into a walk-in wardrobe while the other room is reserved for my parents to stay and is fully furnished. Our unit valuation is about $1,500,000. If we sell at valuation, we are able to profit a healthy amount of about $650,000. With that in mind, we are tempted to sell and purchase another bigger unit.

Property agent advise us to decouple. I will buy over her share while she used the money to purchase another new launch smaller private unit for investment or rental. Once it reached its’ TOP in 3-4 years time, we can sell 2 units and purchase a larger private unit. This would be our last chance to “flip” and get our next pot of gold by selling the newly TOP unit in 4 years time.

Alternatively, we sell our current unit and purchase a larger HDB unit (which we can have some savings for rainy days). Considering, also the current high prices of housing and interest rates which will be a heavier burden on us if we get a larger size private unit. The latter option will be comfortable for our kids with the facilities available.

Financially, we have a stable combined income of $180,000 per annum. With investments and saving bonds, we can receive about $200,000 by the age of 60. Personally, I hope to have a capital appreciation for my house just in case of any emergency, I can downgrade my unit for “cash on hand”.

We would like to move to Serangoon area (most preferred), North or North East side of Singapore. Mainly is to stay near my parents in law as they are the caretaker for our 2 kids.

Apologies on such a long email.I look forward to hear your profession advise soon so that we can make a sound decision.

(This is part of an ongoing series where we answer reader questions about the property market. If you have one of your own, send it to stories@stackedhomes.com.)

Hey there,

Thank you for the kind words, we’re really happy to hear you enjoy our content and that it has been helpful to you in your journey so far!

We do see how this can be a rather perplexing situation to be in. It is actually quite a common scenario that those in the same age group (early to mid-40s) are facing as it could possibly be the last opportunity to capitalise on a new launch property, but at the same time, you do also need a bigger space to accommodate your growing family.

As with most cases, it is a matter of what you truly prioritise the most at the end of the day. Figuring out which of these you prioritise more is crucial to making the right decision for a better peace of mind. For now, we’ll run through the options you’ve listed and share our thoughts on them!

The challenge for many buyers today isn't access to information.

It's interpreting that information in a way that makes sense for their finances, goals, and stage of life.

Over time, that's also why we decided to work with agents who shared the same data-driven and advisory-led approach behind our editorial, consultants who could help readers think through decisions more objectively, rather than simply push transactions.

Today, the team has worked with more than 2,000 clients across over $5B in property transactions.

Should you decouple and purchase a smaller new launch unit for investment?

Many people are always tempted by the decoupling option with the promise of maximising future profits, but there are its risks. However, this option is possible with the consideration of capital gains in mind since it does not change the current living situation. Here are several things you should take note of before proceeding:

- Costs involved

Since your EC has reached its Minimum Occupation Period (MOP), the Seller’s Stamp Duty (SSD) will not be payable. But for those who are looking to decouple within 3 years of purchasing a private property, an SSD of 4 – 12% will be chargeable and this has to be paid in cash.

For the individual that is buying over the shares of the property, he/she will have to pay a Buyer’s Stamp Duty (BSD) which will be calculated based on the value of the shares that are being bought over.

So for example, if both parties own 50% shares each and the valuation of the property is at $1.5M, the party buying over the shares will have to pay a BSD of $17,100 based on the valuation of the 50% share value at $750,000.

As decoupling involves 2 transactions, i.e buying, and selling, the legal fees can amount to upwards of $5,000.

2. CPF refund

As with a normal selling transaction, when a property is sold, your CPF used plus incurred interest will have to be refunded into your CPF OA. For the party buying over the shares, a considerable amount of CPF funds could have already been utilised in the initial purchase of the property, so he/she may need to pay for the CPF refund of the selling party in cash.

Put simply, if the CPF refund for the selling party is $300,000 and the buying party currently has a balance of $100,000 in his/her CPF OA, he/she will have to top up the remaining $200,000 in cash into the selling party’s CPF OA.

3. Loan amount

The individual buying over the shares of the property will have to ensure that his/her income is able to support the new loan given that the current Total Debt Servicing Ratio (TDSR) threshold is at 55% of a borrower’s monthly income. Just as with any property purchase, we always want to practice prudence and not over-stretch ourselves, especially for a family with young kids like yourself.

As we do not have your exact figures, we cannot advise whether or not you guys will be able to decouple the property prudently. But since this is something your real estate agent has advised you to do, we’ll assume they have done the calculations and that this is a feasible pathway.

We suppose this investment will be a short-term plan seeing that you will most likely need to move in the next few years as your kids are growing up. If you’re looking at a new launch property and planning to sell once it obtains its Temporary Occupation Permit (TOP), then rental will not come into play. If you’re open to looking at resale properties, you should take into account their rental yield and possible capital appreciation in the near future. We have previously written an article on comparing new launches and resale condos which could be helpful for you!

One upside of buying a new launch would be its progressive payment plan which will lighten the financial burden during the initial years while the development is still under construction. After paying the 25% downpayment and stamp fees, this is what the typical progressive payment plan will look like:

| Stage of construction | % of purchase price disbursed |

| Foundation work | 10 |

| Reinforced concrete work | 10 |

| Partition walls | 5 |

| Roofing | 5 |

| Door sub-frames / door frames, window frames, electrical wiring (without fittings), internal plastering, and plumbing | 5 |

| Car parks, roads, and drains serving the housing project | 5 |

| Notice of vacant possession – TOP obtained | 25 |

| Completion date – Certificate of Statutory Completion is issued | 15 |

As for a resale unit, the loan repayment will kick in once the transaction is complete which could be as soon as 2.5-3 months time, but buying a resale unit has its perks too.

You’ll be able to physically see the unit, facing, who your neighbours are (although this can change of course), and start renting it out for income once you get your keys. Some costs that you may incur should you wish to rent out the unit would be the condo’s monthly maintenance fee, agent fees, and cost to clean and touch up the place if needed. As we have said earlier, you should definitely check out the average rental yield before purchasing if your intention is to earn some passive income from the rental.

We get that the prospect of buying a new launch and making a tidy profit upon TOP is a huge draw for investors but that isn’t always the case. Just as buying a resale property doesn’t necessarily mean you’ll lose money. You can read more on that here! It is more important that you have identified the right investment property, rather than decoupling for the sake of buying one – only to be saddled with a poor investment as well as a less than agreeable living situation.

For your perusal, these are some of the most affordable new launch and resale units available on the market at the moment. They may or may not be suitable for you depending on your own needs, you should consult your agent for further analysis.

| New launch / Resale | Development | District | Unit type | Size (sqft) | Level | PSF | Price |

| New launch | The Florence Residences | 19 | 1 bedroom | 603 | #18 | $1,736.32 | $1,047,000 |

| New launch | Atlassia | 15 | 1 bedroom | 506 | #02 | $2,205.59 | $1,116,031 |

| New launch | The Gazania | 19 | 1 bedroom | 463 | #02 | $2,457.88 | $1,138,000 |

| Resale | The Hillford | 21 | 1 bedroom | 398 | #mid | $1,381.91 | $550,000 |

| Resale | Kovan Grandeur | 19 | 1 bedroom | 388 | #01 | $1,443.30 | $560,000 |

| Resale | Le Regal | 14 | 1 bedroom | 366 | #mid | $1,571.04 | $575,000 |

Pointers to mull over should you decide to go ahead with this option:

- Is living in the current house for the next 3 – 4 years workable?

- Is decoupling a feasible option and will you be over-leveraging?

- What if the investment property you’re purchasing is not profitable after 3 -4 years? Will you continue living in your current house or bite the bullet and sell at breakeven/loss?

Let’s take a closer look at the decoupling option.

Buy an own stay property under one name and buy another investment property under your spouse’s name or vice versa, whichever works better. Do note that by limiting your budget to $1.5m and below, you will likely be looking at a 3 bedroom unit (in Serangoon) instead of something bigger. Unlike the HDB option below, you won’t have to wait 5 years to purchase the investment property. It can even be done concurrently if you like.

This option will check all your boxes of having a comfortably sized home with facilities, as well as an investment property that you can cash out on for emergencies. However, this goes back to the question of whether you’ll be over-stretching yourselves.

This is a simple breakdown of the costs involved assuming both your incomes are equal:

| Own Stay | Investment | |

| Price | $1,500,000 | $800,000 |

| 5% Cash | $75,000 | $40,000 |

| 20% Cash/CPF | $300,000 | $160,000 |

| Loan shortfall (Cash/CPF) | $343,800 | $0 |

| BSD | $59,600 | $18,600 |

| Legal fees | $2,500 | $2,500 |

| Outlay | $780,900 | $221,100 |

| Total outlay | $1,002,000 |

| Age | 42 (Buy own stay property) | 45 (Buy investment property) |

| Annual income | $90,000 | $90,000 |

| Monthly income | $7,500 | $7,500 |

| 55% TDSR | $4,125 | $4,125 |

| Monthly installment | $4,125 | $3,480 |

| Interest (included in installment) | $2,278 | $1,750 |

These are the most affordable new launch units that have transacted in the last 8 months:

Pointers to mull over should you decide to go ahead with this option:

- Will you be ok putting yourself in a situation where you’ll have to sell your house in the event of an emergency in order to cash out?

- Are you willing to compromise on space in order to have the best of both worlds (i.e living in a condo and owning another investment property)?

- Will you be over-leveraging?

Should you sell and purchase a larger HDB/private unit?

Either one of these options would solve your issue of space constraint, but let’s take a look at their respective pros and cons.

Buying an HDB

With an annual combined income of $180,000 and taking into consideration a healthy profit of $650,000 after selling your EC, purchasing a 5-room or Executive HDB unit in Serangoon/North/North East region is most certainly achievable.

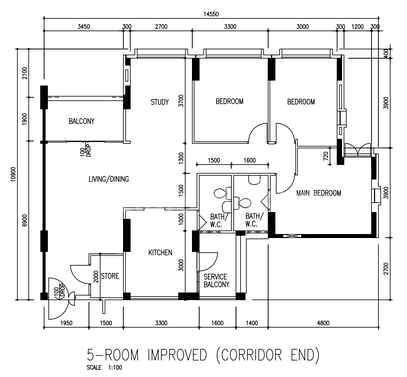

Some 5-room units come with a study area that is sizeable enough to be converted into a bedroom if needed. The layout looks something like this:

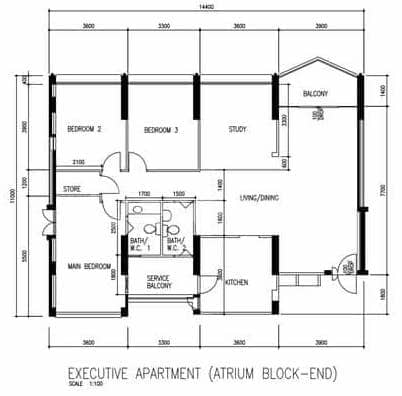

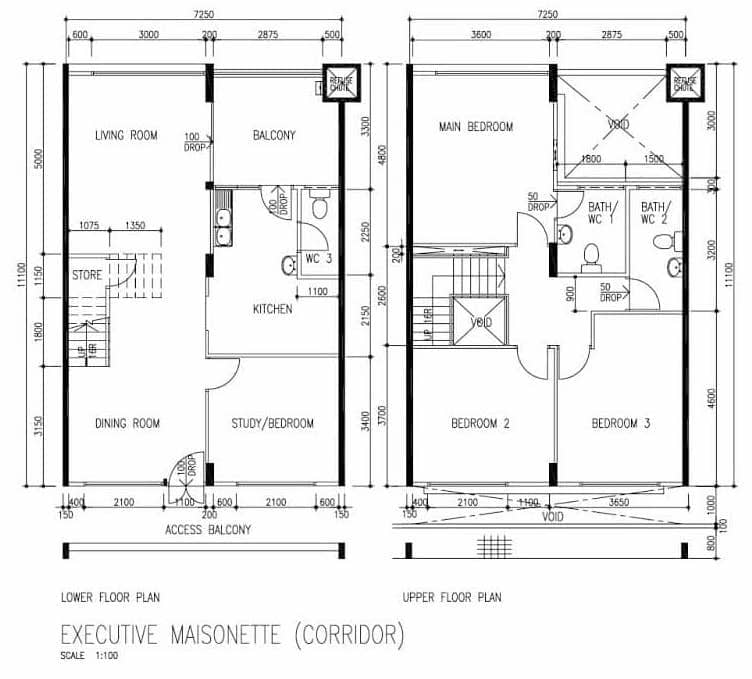

Most Executive Apartments (EA) or Executive Maisonettes (EM) come with either four bedrooms or three bedrooms and a study that is usually also big enough to double as a bedroom. These are examples of their layouts:

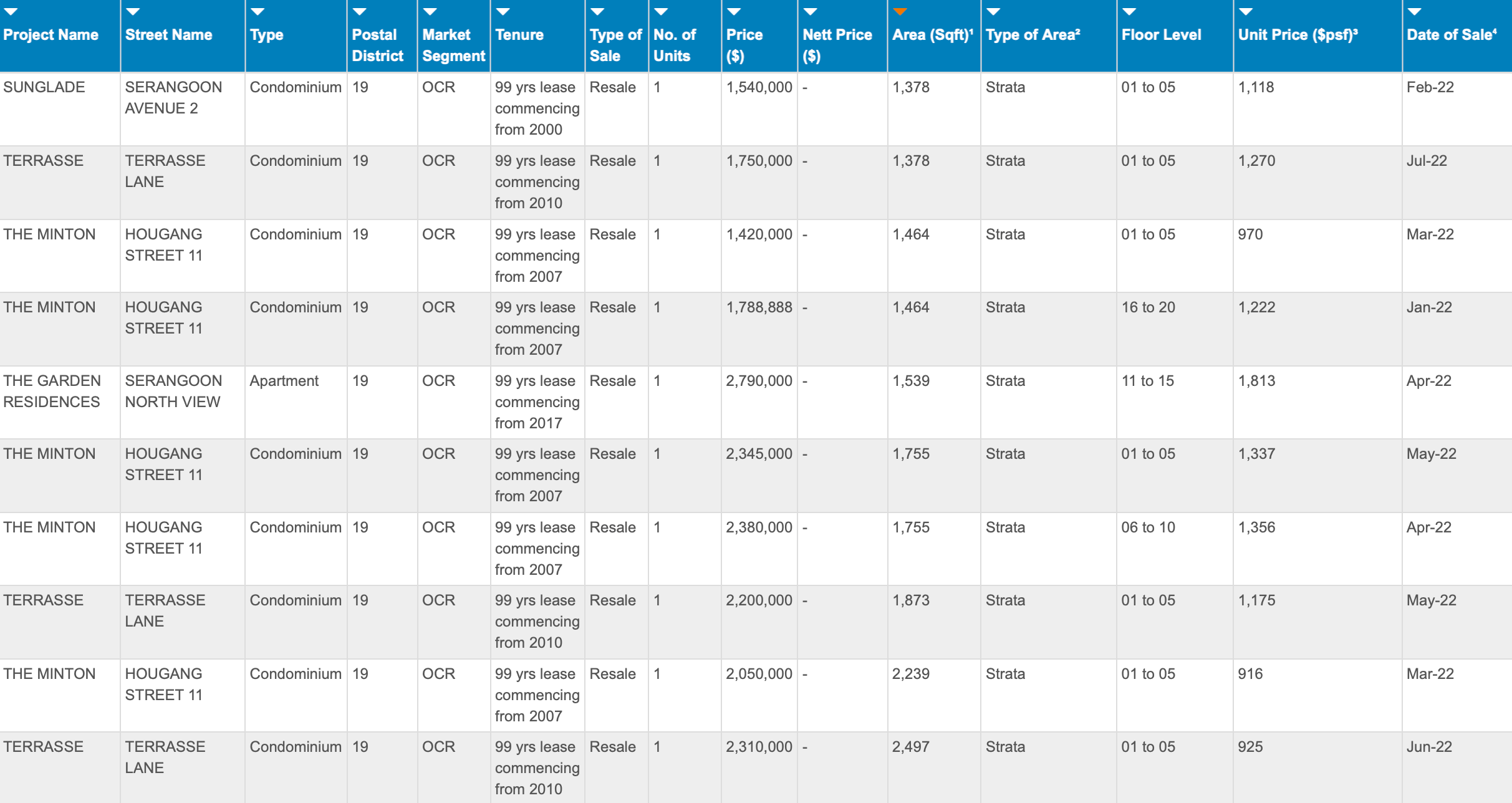

The following are some of the recent transactions in Serangoon (your most preferred estate):

5-room HDB flats

Executive HDB

As you have rightly mentioned, buying an HDB will no doubt allow you to have a greater amount of savings for rainy days. It would also be the option that may give you the biggest peace of mind, as you will not be under any stress should either of you (in the worst-case scenario) lose your jobs. And even if you do decide to retire early, this would be ideal as well. Instead of investing solely in property, you could free up some cash to do alternative investments too.

Do note though that if you’re looking for these bigger 5-room layouts or an executive unit, these blocks will minimally be 20 years and older as HDB has phased out the construction of executive units in the early 2000s. If you prefer something newer, the 5-room units tend to be built smaller so they may not be a good fit.

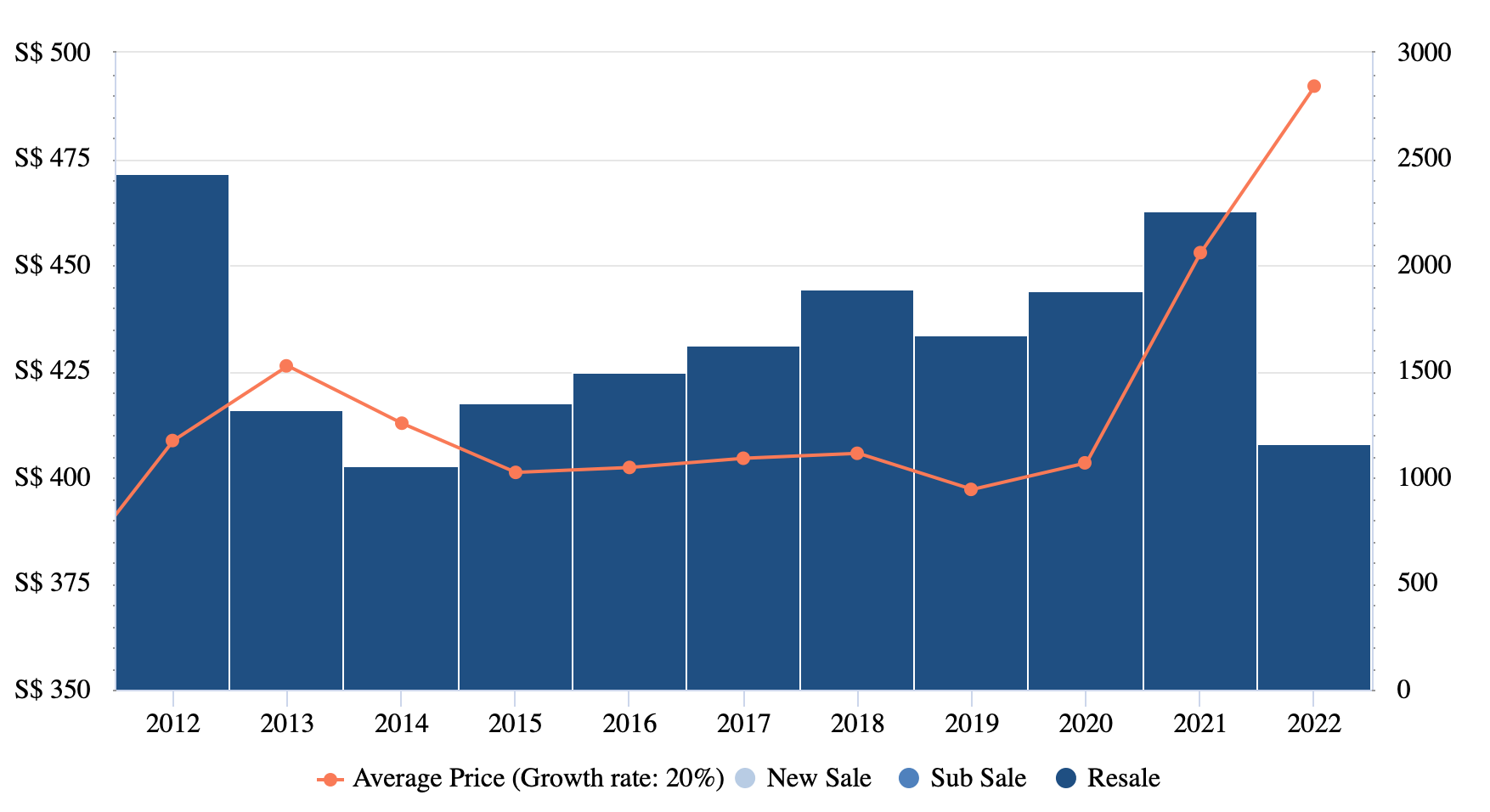

Average price trend and volume of Executive units transacted in the last 10 years:

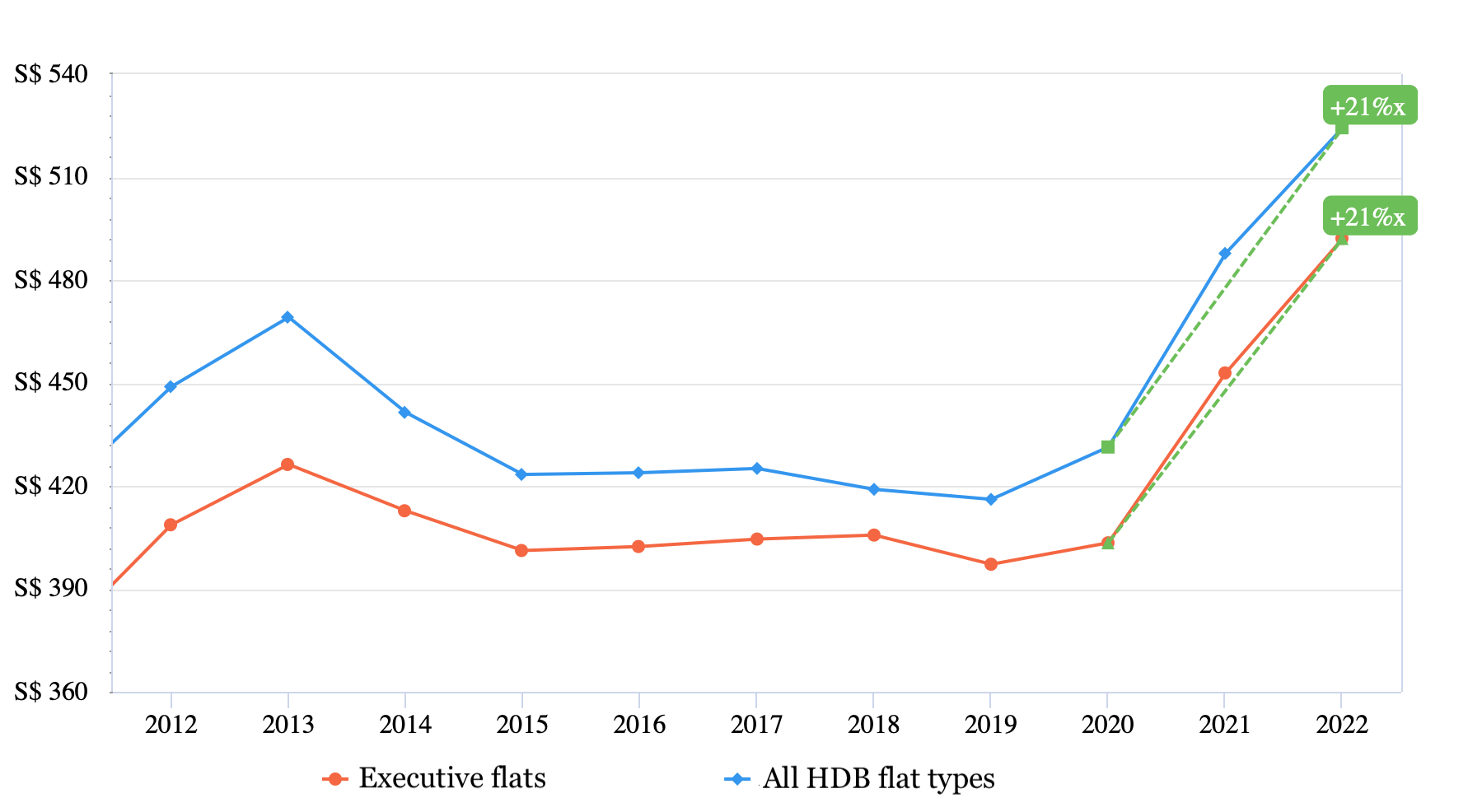

The average price of Executive units in comparison with the average price of all HDB unit types in the last 10 years:

Of course, some may argue that given the limited supply of these flats, and with enough demand, prices may yet go up in the future. We have seen this with the recent 25 year old Hougang EA that changed hands at $1,072,888 in July. Looking at these price trends above, the prices of executive units are on the rise but it is still moving in tandem with overall HDB prices.

Nonetheless, the lease decay is still a factor we should take into consideration especially if you plan to stay for the long term, since the majority of these units were built in the 1980s to 1990s.

A possible option you can take is to purchase the HDB under one name, either yourself or your wife, with the other party listed as an essential occupier. The essential occupier can then go on to purchase another property for investment purposes after the HDB has reached its MOP.

This will check most of your boxes seeing that you will have a spacious home for your family, as well as an avenue that will allow you to cash out in case of an emergency without affecting your living situation. The drawback of this option is that you will have to wait 5 years before being able to purchase your investment property (which may not necessarily be a bad thing as you can use this time to save up).

Pointers to mull over should you decide to go ahead with this option:

- Are you comfortable living in an HDB flat with no facilities?

- Does waiting 5 years to purchase the investment property fit in your timeline?

Buy a private property

Here are some recent transactions of projects in Serangoon:

If we’re looking at units >1,300 sq ft in the Serangoon area, they are going from $1.4m – $2.8m depending on their size.

Let’s say we were to purchase a unit that is priced in between at $2m (contingent on how much cash and CPF you want to put into the house) and you take the full loan of $1.4M (this is your estimated maximum loan for a private property based on $180,000 combined annual fixed income, ages of 42 & 45 and no other outstanding loan) which is still $100,000 short of the 75% LTV.

This means you’ll need to pay a total of $600,000 in cash/CPF for the 25% downpayment and loan shortfall. Not to mention, we haven’t taken into account the BSD as well as legal and other miscellaneous fees. This could eat into the profits that you’ve made from the sale of your EC if you do not have sufficient CPF funds and cash on hand. Based on an interest rate of 3.5% with a loan quantum of $1.4m and a tenure of 21 years, your monthly repayment will be $7,853.

In this scenario, it is likely that you will have to purchase the property under both your names in order to be eligible for this loan quantum and utilise both your CPF funds. This option will check the boxes of having a larger home with facilities, but in the event of an emergency, cashing out on the property may be a sticky position to be in as it will affect your housing situation.

Conclusion

As we have mentioned at the beginning, it is important to figure out what your priorities are before moving forward. Every option has its tradeoffs, it depends on what matters more to you and what you are willing to forgo.

Ultimately, perhaps you should ask yourself the amount of risk that you are willing to take. Owning 2 private properties while on the surface can seemingly provide for the “ideal” Singaporean dream, but actually can be a form of undue stress that can lower your own quality of life.

Again, it’s hard to really give an accurate account given we don’t have full access to your financial situation, but on this brief front – the amount of money left for an investment property should you decouple is limiting on what you can actually purchase given how prices have moved.

So, the question is – how much can you really make from an $800k investment property that would be attractive to you? Given the limited options you have, you have to bear in mind that you might not necessarily be investing in a property because it has good potential, but making a decision to purchase something just because it falls within your budget. And if by doing that, it also affects your family lifestyle because you have to limit the size of the home on that front too? Judging from that viewpoint, we’d say that it may not quite be worth it.

Remember, because of the various cooling measures, property prices in Singapore will not move quite like what they used to before. It’s less of a risk today because prices don’t wildly swing up, so neither would they just drop drastically. Because of that, don’t assume that your investment property will always be a huge pot of gold for you as it’s better to tamper your expectations on that front.

Also, all this talk is with the assumption that everything goes well, and that the investment property that you pick does well. What if it doesn’t? Beyond a stagnant property, you have holding costs to think about too (even if you can rent it out).

We’d suggest that you also consult an agent to assist with this process, especially if you’re planning to decouple or purchase 2 properties as these could get complicated if your financials are not done right.

Have a question to ask? Shoot us an email at stories@stackedhomes.com – and don’t worry, we will keep your details anonymous.

For more news and information on the Singapore private property market or an in-depth look at new and resale properties, follow us on Stacked.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

4 Comments

I love this article. There are so much that you’ve unpacked for the readers. Thank you so much. I would love to see this same article and subject for locations near to the city… city fringes. Kudos to the writer and team that contributed.

So after writing one whole NUS economics thesis, whats the answer? No conclusion right? LOLs. The sad fact is 1.5m with 650k profit doesn’t mean anything as you can’t even move closer to town ie serangoon side, without coughing up 1.8m up for a larger unit, even for an old (>15 year old condo). OK lah, let me give a workable suggestion. Sell out, move to Sunglade. Choose a unit not facing the flyover, please.

One other bit of advice. Settle the family own stay unit first. The rest will fall in place, later, down the road. Meaning, don’t worry too much about whether the unit will appreciate or not. As long as it’s a safe bet, it’s fine. For the query, I advise Sunglade as the price decent, next to NEX, location quite central, can get a larger unit. They can thank me 5 years later.