Since the news of the cooling measures in August, we’ve written about how it has impacted the middle-class group in Singapore. However, the news comes with a silver lining for the lower-income group – the maximum Enhanced Housing Grant (EHG) subsidy was previously $80,000, but the ceiling has now been raised to $120,000.

In this piece, we take a closer look at how Singapore’s lower-income households are likely to be affected by the recent changes.

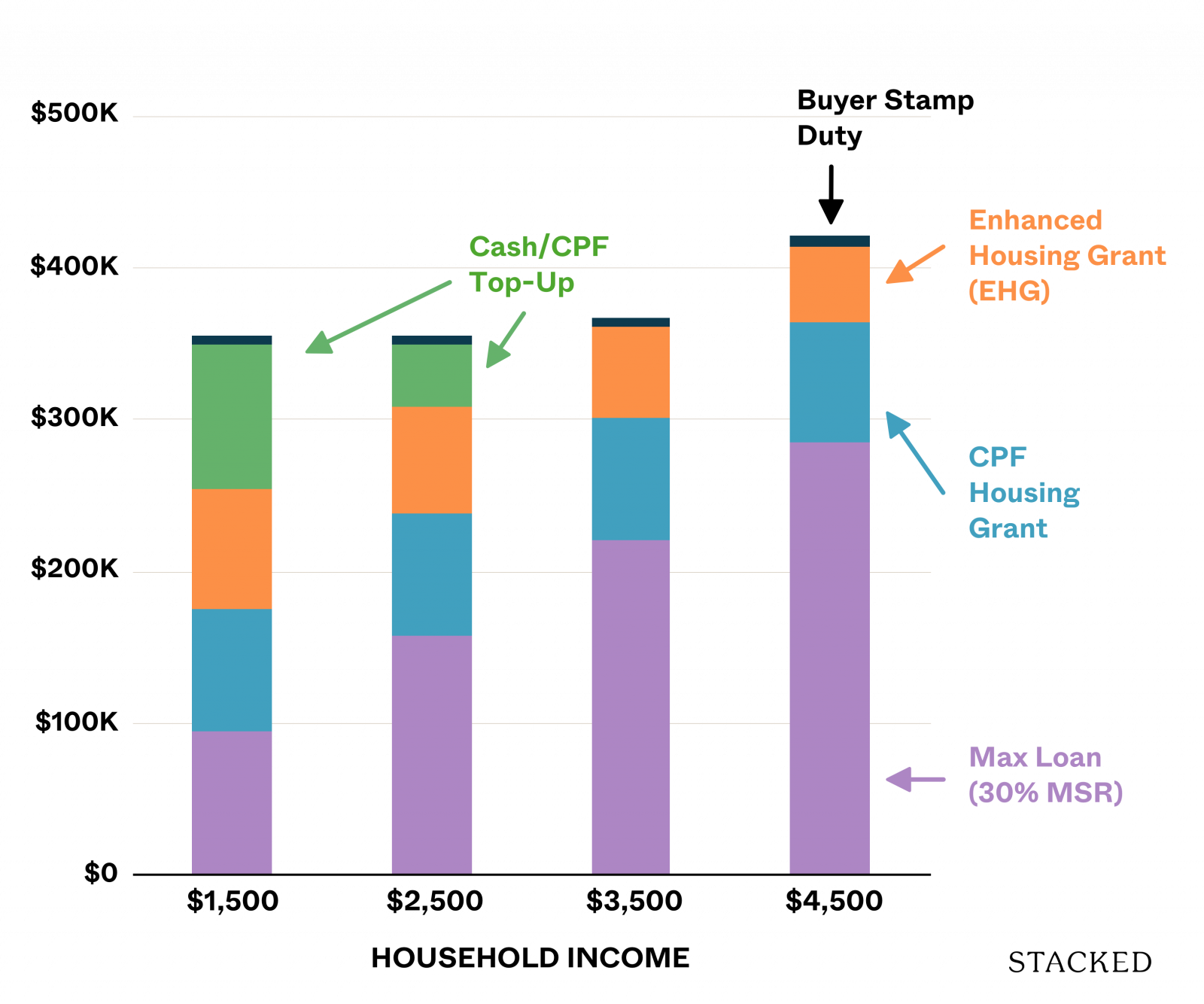

First up, here’s how the increased EHG helps:

Next, let’s see how it impacts affordability. It has to be said, answering this question puts us in a predicament as we have to make some assumptions. Unlike the middle income where using a simple formula lets us find out what they can afford based on the MSR, lower income groups have to put up a lot more cash/CPF to meet the minimum requirement for even a 3-room HDB flat.

And this is difficult even with the higher Enhanced Housing Grant.

The middle income can simply choose an older flat or a cheaper estate. The lower income has fewer options.

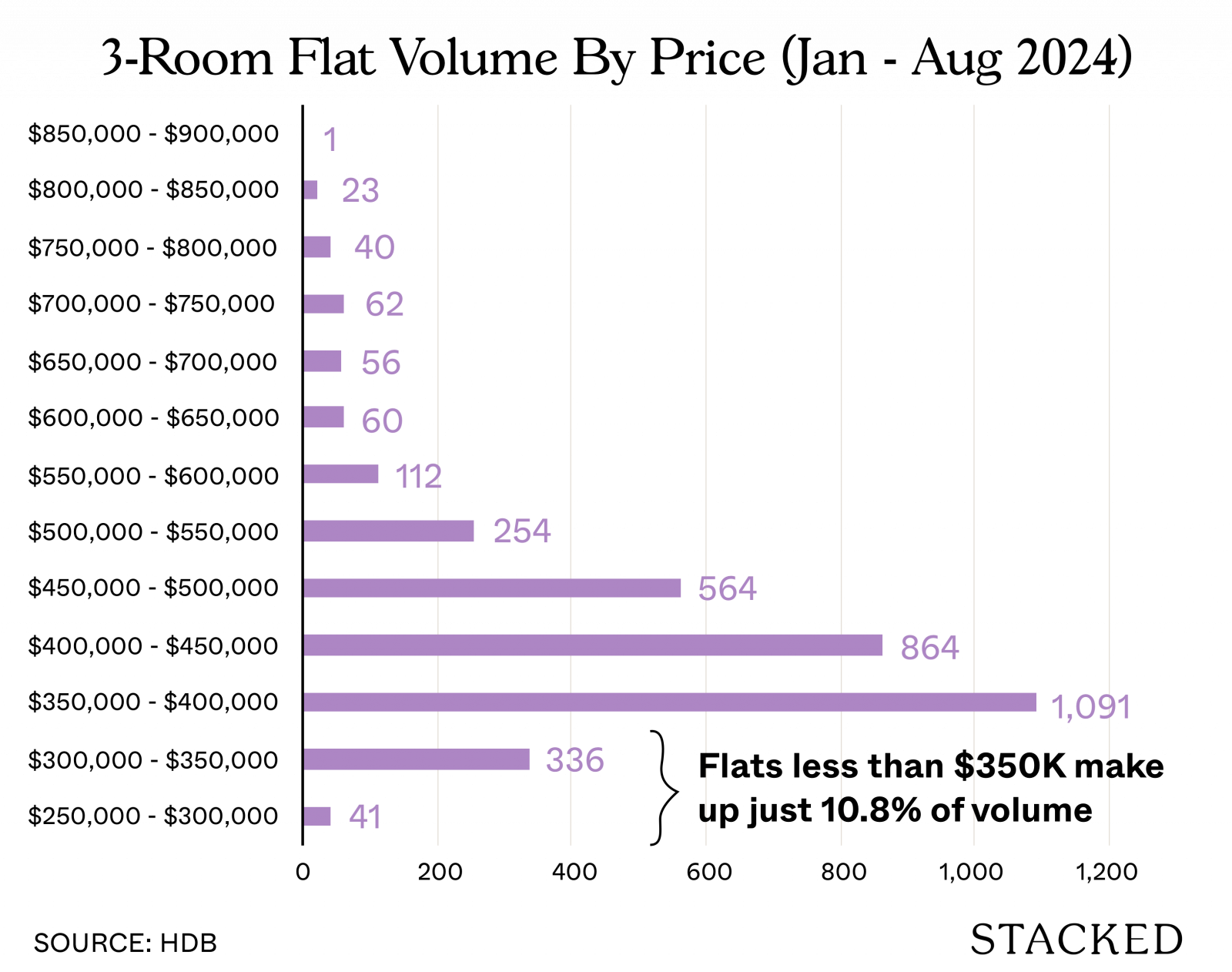

To illustrate, here’s a look at the volume of 3-room flats transacted by price bands, starting with $250K:

Only around 11% of all 3-room flat transactions (excluding Terrace homes for obvious reasons) transacted for $350K and below. If you’re stuck within this price range, you don’t have a lot of choices at all. These would be the oldest 3-room flats you can buy in Singapore.

Since calculating a purchase price using an MSR formula alone isn’t sufficient, we’ll need to consider a scenario. For example, a lower-income family looking to start their journey towards homeownership might aim to purchase a 3-room flat, typically priced around $350K. We will base our analysis on this assumption.

With that in mind, let’s now look at how the regulation plays out for them.

| Before 20th August 2024 | Household Income | |||

| Type | $1,500 | $2,500 | $3,500 | $4,500 |

| Enhanced CPF Housing Grant | $80,000 | $70,000 | $60,000 | $50,000 |

| CPF Housing Grant (Families) | $80,000 | $80,000 | $80,000 | $80,000 |

| Max Loan (Based on 30% MSR) | $94,894 | $158,157 | $221,420 | $284,683 |

| Max Loan + Grants | $254,894 | $308,157 | $361,420 | $414,683 |

| HDB Flat Price (Loan + 20%) | $350,000 | $350,000 | $361,420 | $414,683 |

| LTV Ratio | 27% | 45% | 61% | 69% |

| Top-Up Required | $95,106 | $41,843 | $0 | $0 |

The MSR of 30% severely restricts the affordability of a household earning $1,500 (they can loan $94,894). Plus the grants, this comes up to $254,894. At this price, the household will have few options that topping up is necessary. If we assume they have saved up to purchase a $350,000 flat, then the cash/CPF top-up they have to top up $100,306 (including the BSD):

Here’s what their affordability looks like after the recent changes:

| From 20th August 2024 | Household Income | |||

| Type | $1,500 | $2,500 | $3,500 | $4,500 |

| HDB Flat Price (From Previous Example) | $350,000 | $350,000 | $361,420 | $414,683 |

| Enhanced CPF Housing Grant | $120,000 | $105,000 | $90,000 | $70,000 |

| CPF Housing Grant (Families) | $80,000 | $80,000 | $80,000 | $80,000 |

| Max Allowable Loan Based On 75% Of Purchase Price | $262,500 | $262,500 | $271,065 | $311,012 |

| Max Loan Based On MSR | $94,894 | $158,157 | $221,420 | $284,683 |

| Max Loan + Grants | $294,894 | $343,157 | $391,420 | $434,683 |

| Buyer Stamp Duty | $5,200 | $5,200 | $5,443 | $7,040 |

| Top-Up Required | $55,106 | $6,843 | $0 | $0 |

| Difference in top-up | $40,000 | $35,000 | $0 | $0 |

You can clearly see the difference in the change in the Enhanced Housing Grants. Now the low-income group who wants to afford the $350K is closer to being able to afford a $350k flat.

You’ll also see that now, households earning $3,500 and $4,500 saw their affordability go up by $30,000 and $20,000 which is equivalent to the EHG increase. In this case, their affordability is now $391,420 and $434,683 respectively.

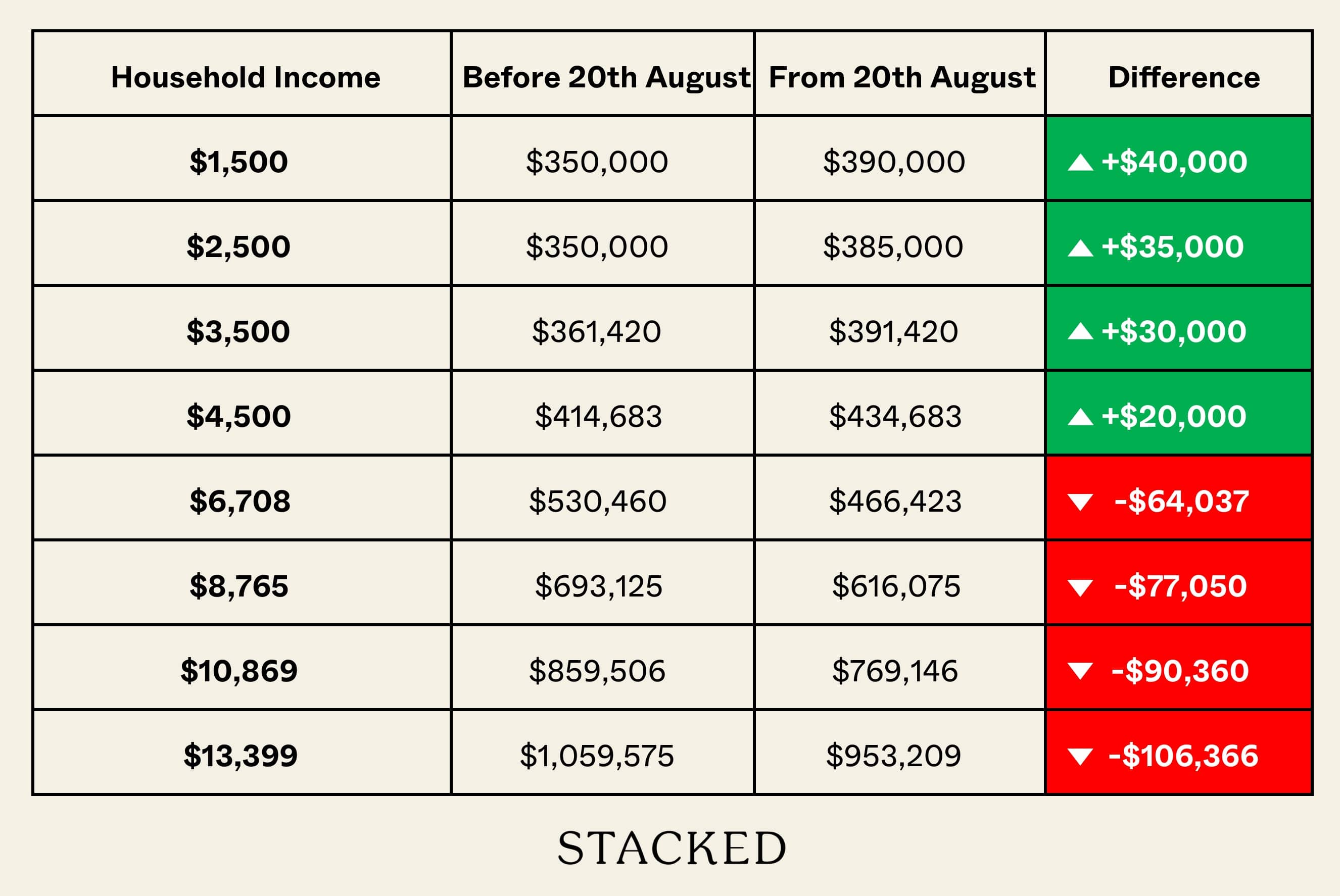

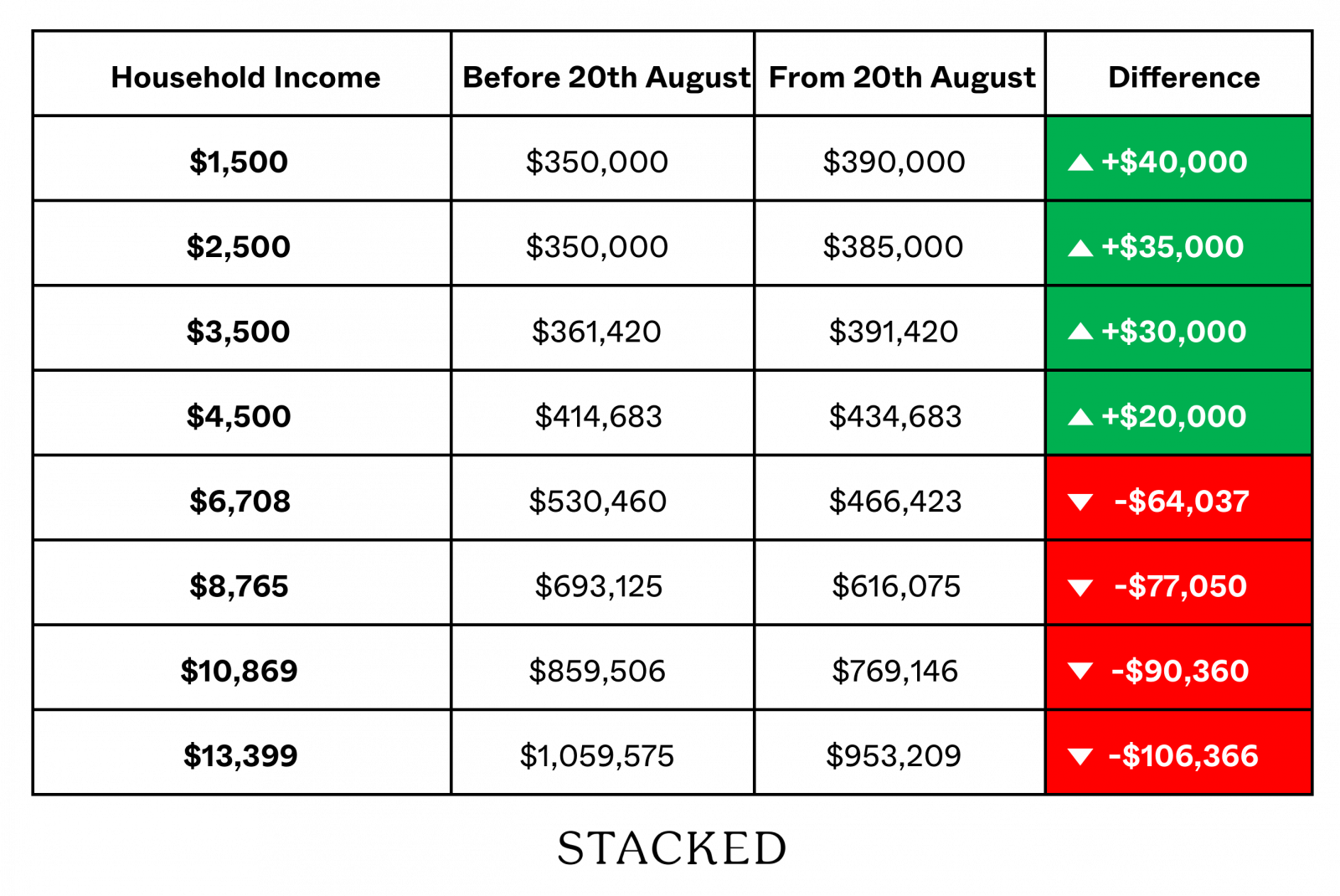

Now that we have all the figures, we can put every income group looked at together (based on our previous article here) and see the before-after effects assuming the top-up amount remains the same:

What’s interesting here is how the income groups between $4,500 and $6,708 converge. While the increased grant amount of $20,000 doesn’t look like much, the drop in affordability for middle-income earners who aren’t able to meet the top up puts them in almost the same category as those earning $4,500.

Another way to look at it is – now, lower-income groups, who were hardest hit by inflation and the increased interest rates, have received the greatest benefit. So for those in the lower income, while affordability remains a challenge, the playing field has evened out slightly.

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

0 Comments