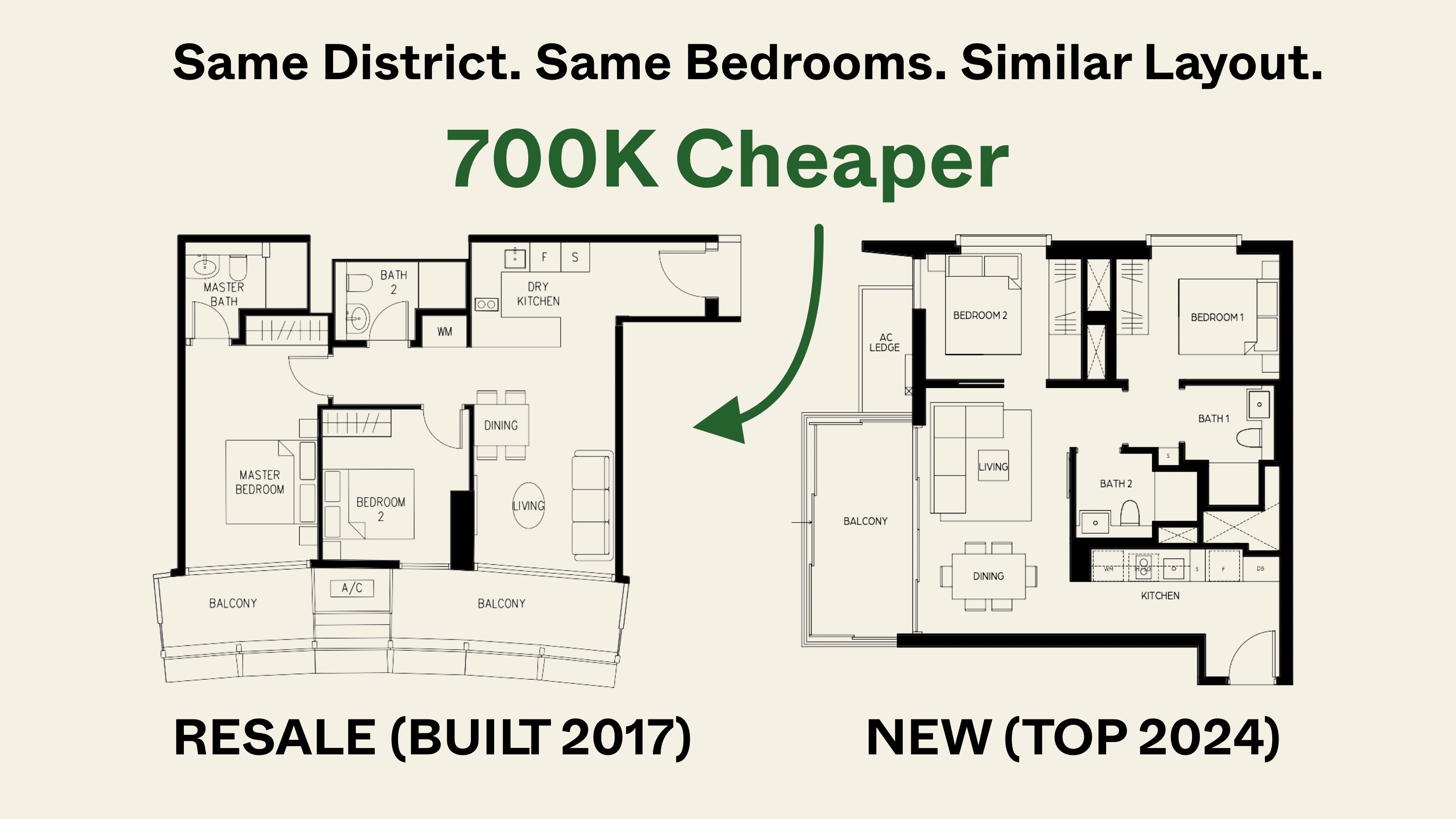

$1M HDB Or Fringe Resale Condo? These 4 Points Will Help You Decide

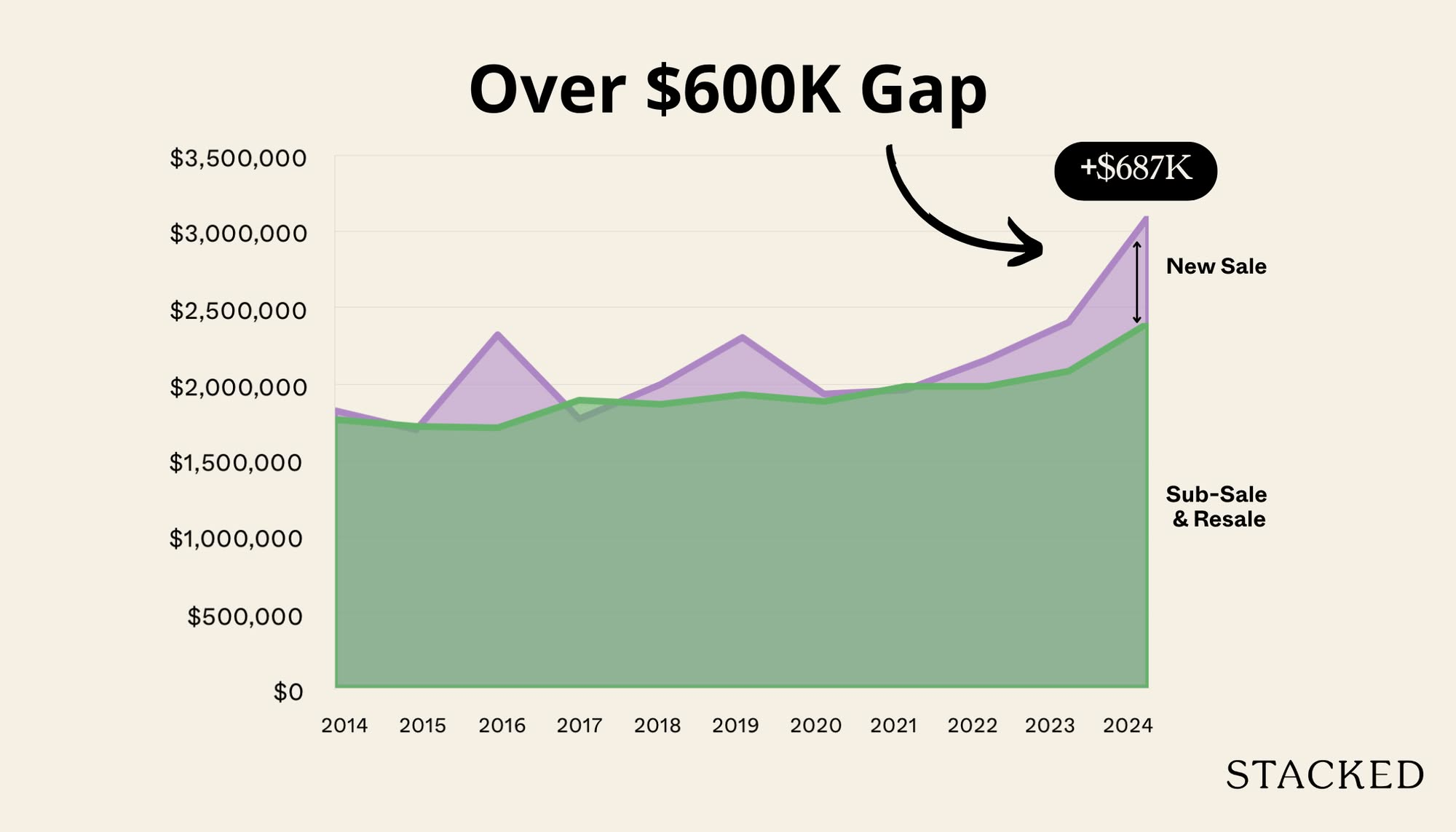

In the past few years, the gap between a fringe region resale condo and a top-end HDB flat seems to narrow. We’re headed to a point where a buyer might seriously ask the question: is it worth buying a condo for just above a million, when such a sum would get you a prime HDB property such as Pinnacle @ Duxton, an executive flat, or a DBSS project near the MRT. Some buyers might even contend we’re at that point today, and the question is already valid. Here’s what to know and consider:

The narrowing gap between million-dollar flats, and fringe, resale condos

To emphasise how difficult that decision is today, check out the prices at which you can get older or fringe region condos today. Some of the projects in the linked article have three-bedders going at $1.2 million to $1.4 million. In the meantime, the current record-holder for flats is at $1.73 million, and many of the best flats in Queenstown, Bishan, Tanjong Pagar, etc. are hovering at around $1 to $1.5 million.

Here’s a look at some of the bigger 3 bedders you can find in today’s private market:

| Condo Name | Estate | Bedrooms | Price | Floor | Size (Sqm) | Lease Remaining |

| Elias Green | Pasir Ris | 3 | $1,410,000 | 4 | 144 | 66 |

| Melville Park | Tampines | 3 | $1,415,000 | 11 | 145 | 67 |

| Sherwood Tower | Bukit Timah | 3 | $1,435,000 | 14 | 141 | 51 |

| Braddell View | Toa Payoh | 3 | $1,480,000 | 4 | 145 | 56 |

| Woodgrove Condominium | Woodlands | 3 | $1,520,000 | 3 | 141 | 72 |

| Eastwood Centre | Bedok | 3 | $1,600,000 | 2 | 140 | 70 |

| Pine Grove | Bukit Timah | 3 | $1,660,000 | 6 | 158 | 59 |

| Ivory Heights | Jurong East | 3 | $1,690,000 | 3 | 155 | 62 |

And here are some of the most expensive HDBs that transacted in 2024:

| HDB Name | Estate | Flat Type | Price | Floor | Size (Sqm) | Lease Remaining |

| Tiong Bahru View | Bukit Merah | 5 Room | $1,588,000 | 34 TO 36 | 112 | 90 |

| CityVue @ Henderson | Bukit Merah | 5 Room | $1,588,000 | 46 TO 48 | 113 | 94 |

| Kim Tian Green | Bukit Merah | 5 Room | $1,580,000 | 40 TO 42 | 113 | 87 |

| The Peak @ Toa Payoh | Toa Payoh | 5 Room | $1,568,888 | 40 TO 42 | 117 | 87 |

| Natura Loft | Bishan | 5 Room | $1,568,000 | 37 TO 39 | 120 | 86 |

| Dover Gardens | Queenstown | 5 Room | $1,550,000 | 37 TO 39 | 124 | 86 |

| Pinnacle@Duxton | Central Area | 5 Room | $1,542,880 | 43 TO 45 | 105 | 85 |

| The Peak @ Toa Payoh | Toa Payoh | 5 Room | $1,540,000 | 31 TO 33 | 117 | 87 |

You can see that the HDBs around the price range of the private condos have a longer lease, are on much higher floors (with better views), and are located in much more central areas. In many of the cases above, the amenities around are also a lot more convenient.

Assuming the trend continues, the line between the cheaper condos and the very best flats will continue to converge. So it’s no surprise that more buyers are asking if the condos are really worth it, given the kind of flats they can buy. To which we say, here are the main points to consider:

1. Investment or owner-occupancy

In terms of investment, the general preference is still toward condos. This is due to a multitude of reasons:

First, the resale prospects are wider for condos. Even though there are fewer eligibility conditions for most resale flats, there’s no getting around the fact that Singapore citizenship or permanent residency is still required. Condos can be sold to anyone, including foreigners; and PRs don’t need to wait three years to buy.

(Although we should add that, given the 60 per cent ABSD for foreigners today, and their tendency to prefer prime-region condos, this is less of an advantage today.)

Second, there are fewer rental restrictions on condos. You can rent out the full unit the moment you acquire and renovate it. For HDB flats, there is still the Minimum Occupancy Period (MOP), during which you can only rent out rooms. For those seeking immediate rental income, a condo is almost always the preference.

Third, condos can go en-bloc, whereas HDB flats only rarely see SERS (less than five per cent of HDB estates), and VERS is something we’ve yet to see happen. That said, we would never advise counting on an en-bloc sale; it’s just a potential condos have that HDB flats lack.

For pure owner-occupancy, all of this may not matter.

In such cases, you might prefer the HDB flat even if the resale / rental prospects are diminished. For pure homeowners, being in a location near the CBD (e.g., Tanjong Pagar), or living in a super-convenient location (e.g., Queenstown or Bishan) might be the priority; doubly so if you’re right-sizing, and the flat is the last stop on your property journey. In these instances, a well-located flat often trumps a fringe-region condo.

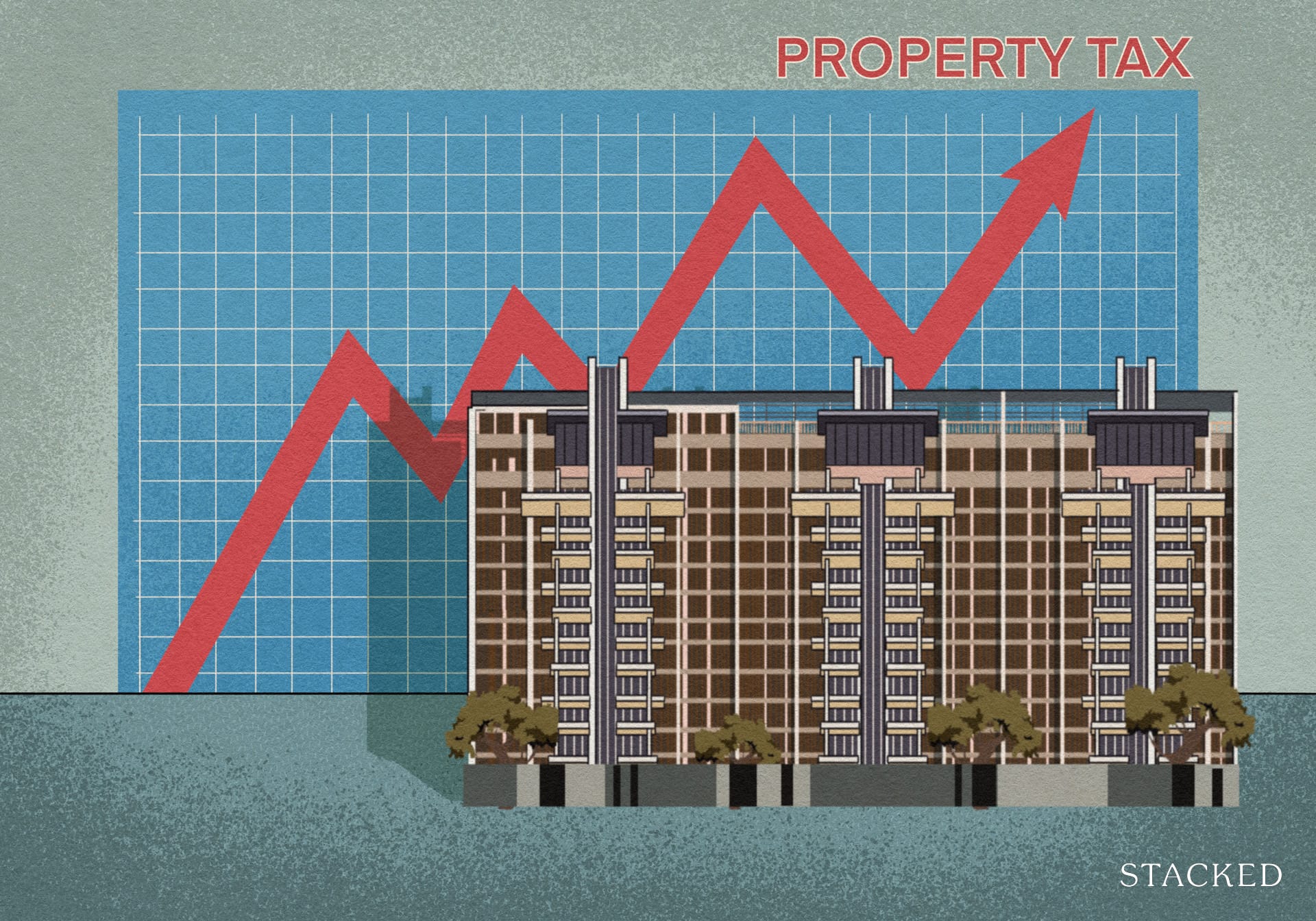

2. Maintenance fees and taxes (especially post-retirement)

Whether or not you use the condo facilities, you have to pay the maintenance fees. Even the biggest flats seldom have conservancy charges above $101, whereas even mass-market condos can rack up maintenance fees of $300 to $400 per month depending on your unit type.

Also note that HDB tends to be more lenient: if you can’t pay your conservancy charges, especially if you’re a retiree, there tends to be a longer grace period; and HDB does its best to avoid evicting people. Condos, on the other hand, often slap on interest rates (we’ve seen rates of 15 per cent per annum). And if you can’t pay the maintenance, the MCST is obliged to take action, including eviction – this is a responsibility to the other owners.

From an owner-occupancy perspective, consider who uses the facilities. It’s not always true that older owners don’t have use for condo facilities: you may want them around for your children, grandchildren, or friends to use.

Retirees, or those nearing retirement, need to keep in mind the maintenance fees never end. They’ll be there even after you’ve paid off your mortgage, so you need to factor them into your post-retirement cash flow needs. Note that these may not always stay the same, and could even go up depending on how much upkeep a property needs as it gets older.

As for property taxes, these are based on the estimated rental income your property could generate per year; the Annual Value or AV. Even the largest flats tend to get assigned an AV of just $13,000 to $14,000, whereas mass-market condos tend to see an AV of around $25,000 to $30,000. So you will be paying more taxes for the condo as well.

3. Importance of unit size

A million dollars could buy you a flat with 1,300 to 1,560 sq. ft., whereas a resale condo might only be about 900 sq. ft. for the price. This is barring some exceptions, such as leasehold condos from the 1970s or ‘80s, which tend to be bigger, and sometimes cheaper due to the age and lease.

The value of this boils down to how much room you need. If it’s just you and your spouse, for example, it might be very comfortable to live in even a two-bedder condo unit, with all the facilities. Conversely, if you have a large family, expect to live with children, etc. the flat might give you more room, for the same budget.

4. Importance of freehold options

Most cheaper or fringe region condos tend to be leasehold; but there are still freehold or 999-year projects that are in the $1.3 million to $1.5 million range. Here’s a recent list of them.

HDB flats are always on a 99-year lease. Million-dollar flats – particularly scarce ones such as maisonettes or jumbo flats – tend to be quite far into this lease. This also ties into the resale issue in point 1 (see above): with limited lease remaining, banks tend to give out smaller loans, and CPF usage is restricted.

A key concern here is legacy planning. If you intend to leave your dependents a property, then a million-dollar flat built in the ‘80s or earlier is probably not a good idea. There won’t be much value left by the time they get the flat.

Conversely, if your children have a home of their own, then you don’t really need to worry about the remaining lease on your flat; they won’t need it anyway (they may not even be able to inherit it, depending on the kind of home they already have).

The right choice comes down to your specific intentions

It’s not a clear-cut choice, as the gap continues to narrow. The decision will be based on your mid to long-term plans, as well as your specific lifestyle needs. If you’re uncertain which to pick, reach out to us on Stacked, so we can help you with a guided walkthrough.

If you’d like to get in touch for a more in-depth consultation, you can do so here.