With Chinese New Year over, it’s house-hunting season again; but it’s no surprise that buyers are a little bewildered. If you’ve been away from the property scene for a few years, the prices today are nothing short of stunning – from fringe region condos crossing $2 million, to warnings against “proven” prime regions. Here are a few things to take note of:

So many readers write in because they're unsure what to do next, and don't know who to trust.

If this sounds familiar, we offer structured 1-to-1 consultations where we walk through your finances, goals, and market options objectively.

No obligation. Just clarity.

Learn more here.

What are condo prices like today?

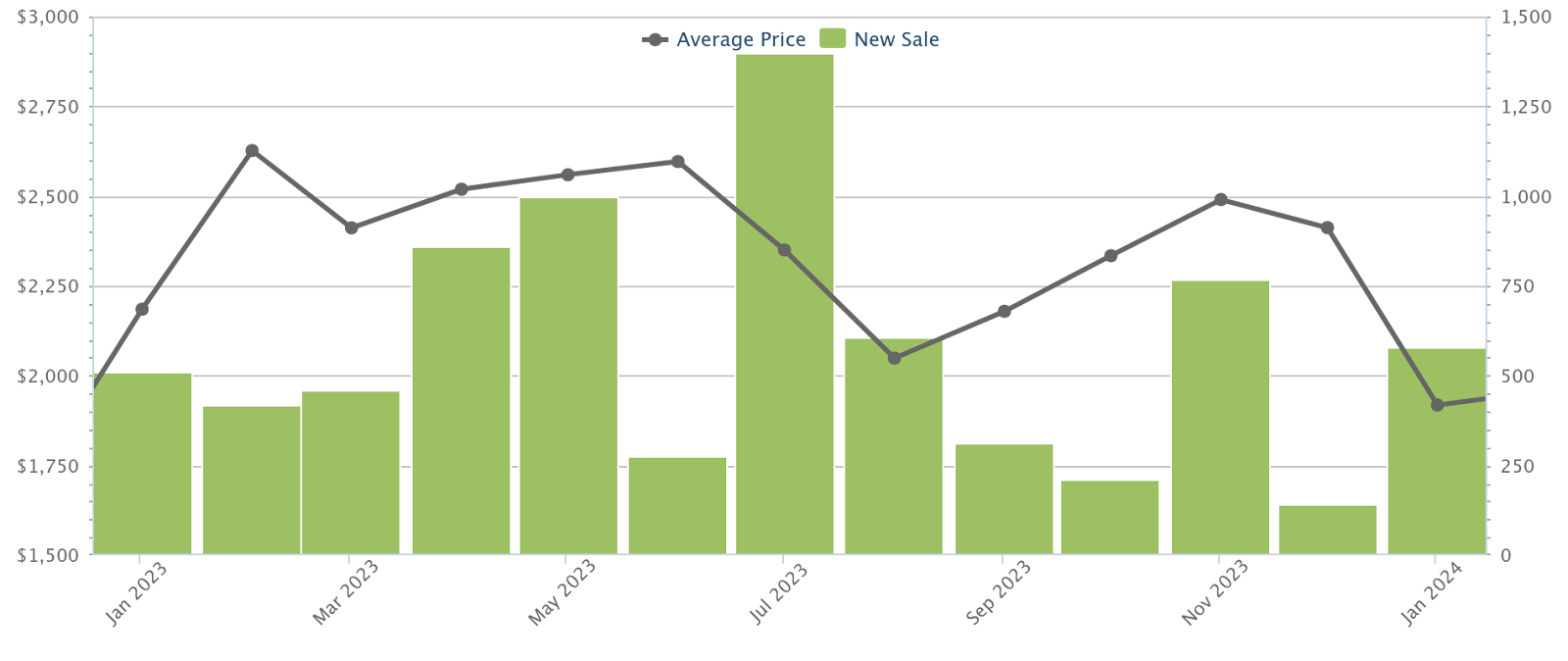

Let’s look at new launch prices first:

As of January 2024, new launch prices were at $1,918 psf islandwide, down from $2,185 psf in January 2023; but note that this is early in the year, and with some 40+ launches ahead, we would expect this to pick up in subsequent months. Note that this is just a brief overview, and looking at psf prices month on month isn’t as ideal due to the volatility in volumes. Nevertheless, this is a quick snapshot to show how new condo prices have been performing since January 2023.

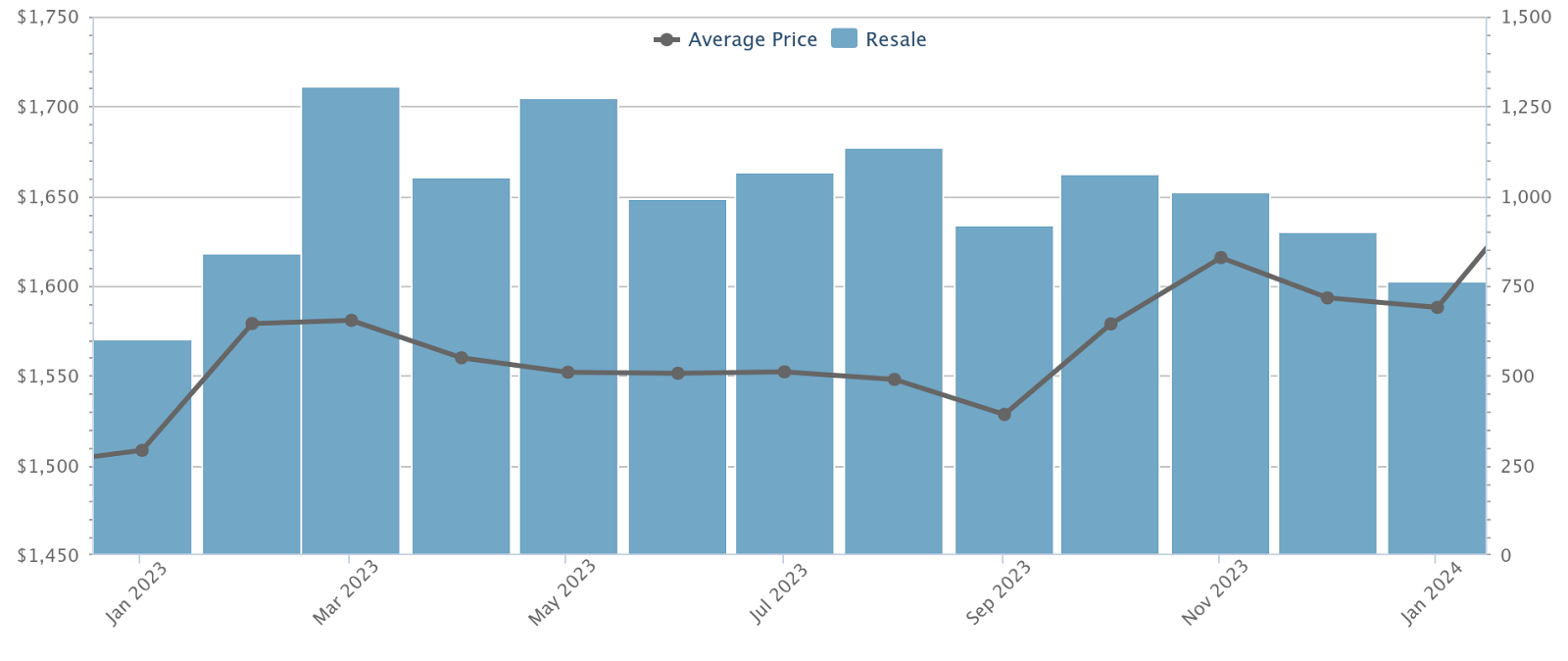

Meanwhile, resale condo prices have been rising, as buyers priced out of new launches increasingly turn to these options:

Average resale condo prices are at $1,588 psf as of January this year, up from $1,508 psf last year.

Based on the above, we can estimate a quantum of around $1.91 million for a 1,000 sq. ft. three-bedder (new launch), and around $1.588 million for a resale unit of the same size.

How have HDB resale prices moved?

HDB resale prices are around $579 psf, as of January this year. This is up from $553 psf last year. We would expect prices to level off further into the year though, given the larger number of completed flats, and the ongoing implementation of Prime and Plus model housing; this could siphon demand from the resale market, drawing away buyers who have no interest in upgrading.

Let’s look more specifically at the 4-room flat, the most ubiquitous type of public housing:

Prices average $588 psf as of January 2024. The typical 4-room flat is around 960 sq. ft. (some may be a bit larger), giving us an average resale quantum of $564,480.

So looking at the probable price gaps faced by upgraders today, we have:

- A possible gap of around $1.345 million between a resale 4-room flat and a new launch three-bedder condo

- A possible gap of around $1.024 million between a resale 4-room flat, and a resale three-bedder condo

What does this mean in terms of the home loan?

Let’s assume an upgrader can qualify for the full 75 per cent Loan To Value (LTV) ratio, and that they can get a loan tenure of 25 years. Under the Total Debt Servicing Ratio (TDSR), the monthly loan repayment cannot exceed 55 per cent of their monthly income.

Also, note that the floor interest rate for TDSR calculations is four per cent per annum (but we suspect this may be raised, if real interest rates go up any further over the year).

We will also assume our upgraders sell their flat before buying their condo, thus avoiding the Additional Buyers Stamp Duty (ABSD).

For a new launch three-bedder at $1.91 million, our upgrader would need:

- $95,500 in cash (the first five per cent of the down payment)

- $382,000 in any combination of cash or CPF (the next 20 per cent of the down payment)

- Buyers Stamp Duty of $65,100

The total loan quantum after this (75% of the price) would be $1,432,500.

But can an HDB upgrader afford this? Assuming a couple purchased their BTO for $500,000 and decided to sell it after 5 years of living in it, here’s what the sales proceeds look like:

| Item | Amount |

| BTO Purchase Price | $500,000 |

| 10% Downpayment (Using CPF) | $50,000 |

| Loan Amount | $450,000 |

| Monthly Payments | $2,042 |

| CPF OA + Accrued Interest | $185,877 |

| Loan remaining after 5 years | $381,743 |

| Selling Price | $800,000 |

| After agent fees | $783,280 |

| Less loan remaining | $401,537 |

| Sales Proceeds after return of monies to CPF | $215,660 |

Assuming sale proceeds of $215,660, our upgrader would have enough cash to meet the $95,500 cash down payment. Counting in their CPF, our couple would have a total of $401,537. This is still around $76,000 short and it doesn’t even include the Buyer’s Stamp Duty, an additional $65,100.

If we assumed the couple saved up enough over the years to afford the BSD, then the monthly repayment on a $1,432,500 loan comes to $6,837 per month*, and under the TDSR framework, the upgraders would need a combined income of around $12,431.

Note that this is above the median income for two people (median income is reportedly $5,197 per individual at the time we write this).

*For new launches, you will not actually pay this full amount at the start, as there is a Progressive Payment Scheme. The monthly loan amount will increase as work is completed, and you will be paying the full amount by the time the project reaches TOP.

For a resale three-bedder at $1.588 million, the numbers look more realistic. For this, our upgrader would need:

- $79,400 in cash (the first five per cent of the down payment)

- $317,600 in any combination of cash or CPF (the next 20 per cent of the down payment)

- Buyers Stamp Duty of $49,000

The total loan quantum after this (75% of the price) would be $1,191,000.

Once again, let’s assume they get sale proceeds of $215,660 from their resale flat. Again, this is enough to meet the cash down payment of 5%. The remaining 20% is where buying a resale looks more realistic than a new launch. They would need $397,000 which the couple has. However, what’s missing is the Buyers Stamp Duty. In this case, we’ll assume that over the 5 years, the couple has saved enough to pay this down too.

Let’s assume then that the couple uses the full amount of their sales proceeds $401,537 to bring the loan down to $1,186,463.

This would bring the monthly loan repayment to $5,664 per month, which requires our upgraders to have a combined income of around $10,300 per month; somewhat manageable for two borrowers on median income.

In general, this leads us to conclude that a greater number of upgraders are priced out of the new launch market, even in non-central areas. However, the resale market – as well as any Executive Condominium launches – are likely to remain viable prospects assuming the profit on the BTO is large enough or the couple somehow manages to save enough for the respective fees (conveyancing fees, Buyer’s Stamp Duty etc).

Here’s a summary of the numbers:

- For the new launch three-bedder at $1.91 million:

- Down payment: $95,500 cash + $382,000 (20% of down payment) = $477,500

- Buyer’s Stamp Duty: $65,100

- Loan quantum: $1,432,500

- Assuming sale proceeds from resale flat: $215,660

- Assuming the couple is able to top up the BSD

- Loan amount after sale proceeds: $1,432,500

- Monthly repayment: $6,837

- Required combined income: $12,431

- For the resale three-bedder at $1.588 million:

- Down payment: $79,400 cash + $317,600 (20% of down payment) = $397,000

- Buyer’s Stamp Duty: $49,000

- Loan quantum: $1,191,000

- Assuming sale proceeds from resale flat: $215,660

- Assuming the couple is able to top up the BSD

- Loan amount after sale proceeds: $1,186,463

- Monthly repayment: $5,686

- Required combined income: $10,338

Note that these examples are generalised: there can be significant differences once it comes down to specific projects, so do reach out if you need help with your individual situation.

What’s the difference between 2024 and previous years?

The most glaring difference would probably be the amounts involved; 2024 is at the tail end of price spikes in 2022 and 2023. But that aside, there are a few factors that go beyond the numbers:

First, the interest rate is much higher compared to previous years. If the last time you bought a home was 10 years ago, for example, you may be used to an interest rate of two per cent or below. The most significant factor here is that your home loan interest rate is no longer outpaced by your CPF interest rate (2.5 per cent).

You can check out the full details here.

The second difference is only relevant to higher-budget upgraders, who can look to the Core Central Region (CRR), or other prime areas. We have more details on this here, but to summarise, the latest round of cooling measures disproportionately impacted the CCR. Foreigners face 60 per cent ABSD, and these buyers tend to prefer prime regions – so locals looking to these areas may see less competition.

This is all happening against a backdrop of growing geopolitical issues, from the war in Europe to the upcoming US elections, so 2024 may be a year to play it safe. In light of all this, we do think that – for the average Singaporean upgrader – it’s best to keep upgrading goals modest: look toward upgrading to an EC or resale condo, or perhaps even just to a bigger flat, if you’re not in the higher income brackets.

It’s generally less painful to wait and upgrade later, than it is to make a mistake and have to downsize back to a flat (especially now that, if you just sold a private property, you may need to wait 15 months to buy a resale flat.)

At Stacked, we like to look beyond the headlines and surface-level numbers, and focus on how things play out in the real world.

If you’d like to discuss how this applies to your own circumstances, you can reach out for a one-to-one consultation here.

And if you simply have a question or want to share a thought, feel free to write to us at stories@stackedhomes.com — we read every message.

6 Comments

Hello, i believe the downpayment for HDB BTO should be 20% which is 200k instead of 10% as written in the table.

Sorry i meant 100k**

So far, all news outlets keep reporting where & which HDB resales broke new pricing records but short of the buyers perspectives….!!

Wonder who are these HDB resale buyers who can afford to folk out >$1m to buy?

Are they mainly from private downgraded dwellers? If yes, I thought there is 15months embargo period after they sold their private properties…

Or are these cash rich PRs or locals???

Hope someone or MND can look into these $m HDB Resale buyers’ demographics in order to understand their buying perspectives.

three-bedder at $1.91 million – this is not realistic. It should be around at least 2.5 million.